Simple but not easy

Investing is simple but not easy. We largely know what to do, what to ignore, the right time horizon to focus on for superior long-term results, but we seem to not be able to get out of our own way. And by we, I mean pretty much all human decision makers, investors, allocators and stock pickers.

In simple terms, actively managed Australian small caps out-perform large caps (active or passive) over the long term. This outperformance is not linear nor consistent every year, which means the path to superior long run performance is marked with periods of underperformance. This underperformance has been the story of 2023 (and 2022!) but the long term remains intact.

In 2023 we covered much of what investors need to know about the whys and hows of long-term small cap outperformance:

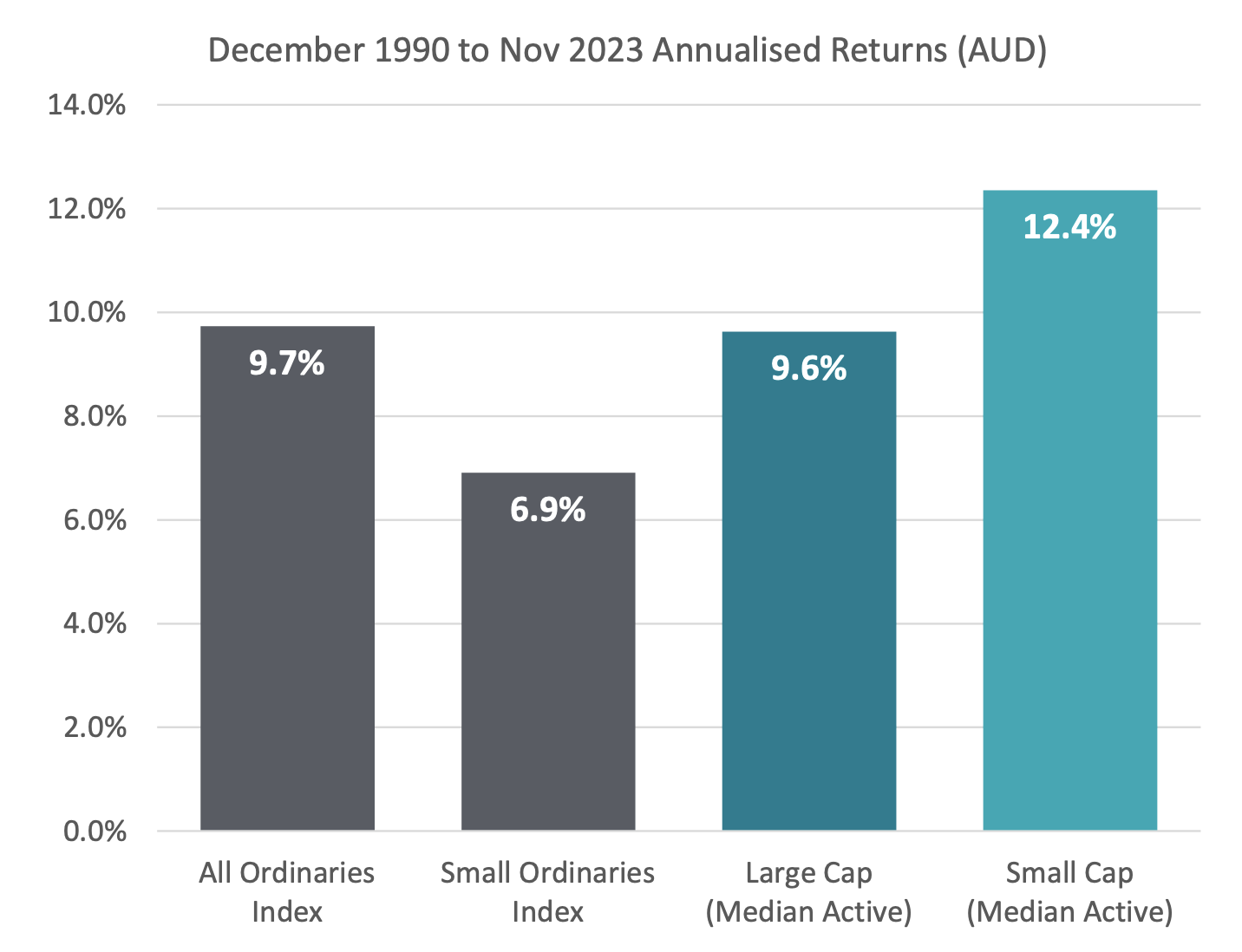

- Long term Australian small cap outperformance: Active Australian Small Caps have been one of the best performing places to invest over the past three decades.

Source: Morningstar, Longwave Capital. Index returns are gross of fees, fund returns are net of fees.

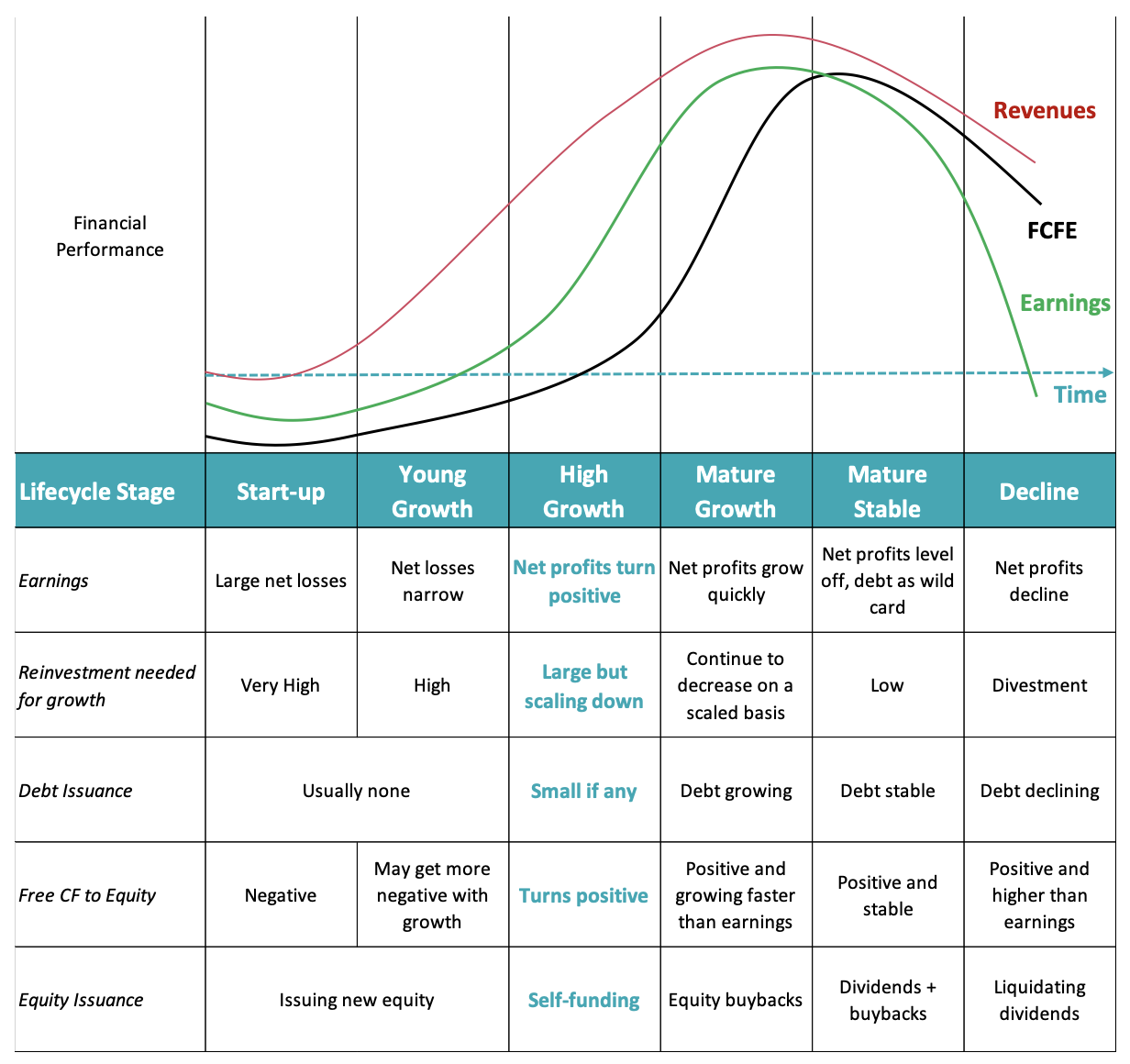

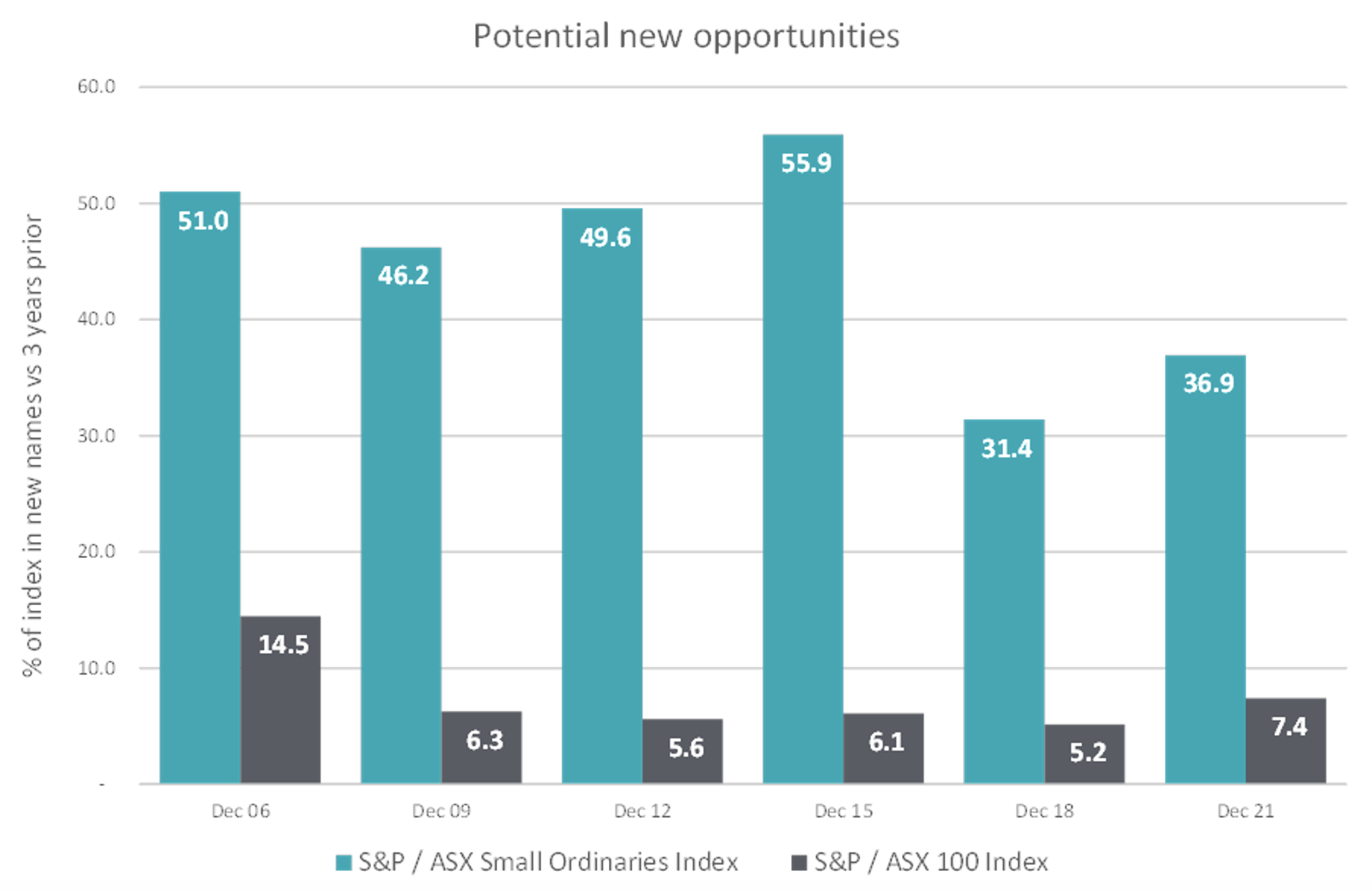

- Why Small Caps are different: Investors often forget that small caps are younger and more fragile than their large cap brethren. They are also less well covered and more dynamic businesses.

Source: Aswath Damodaran, Longwave Capital Partners

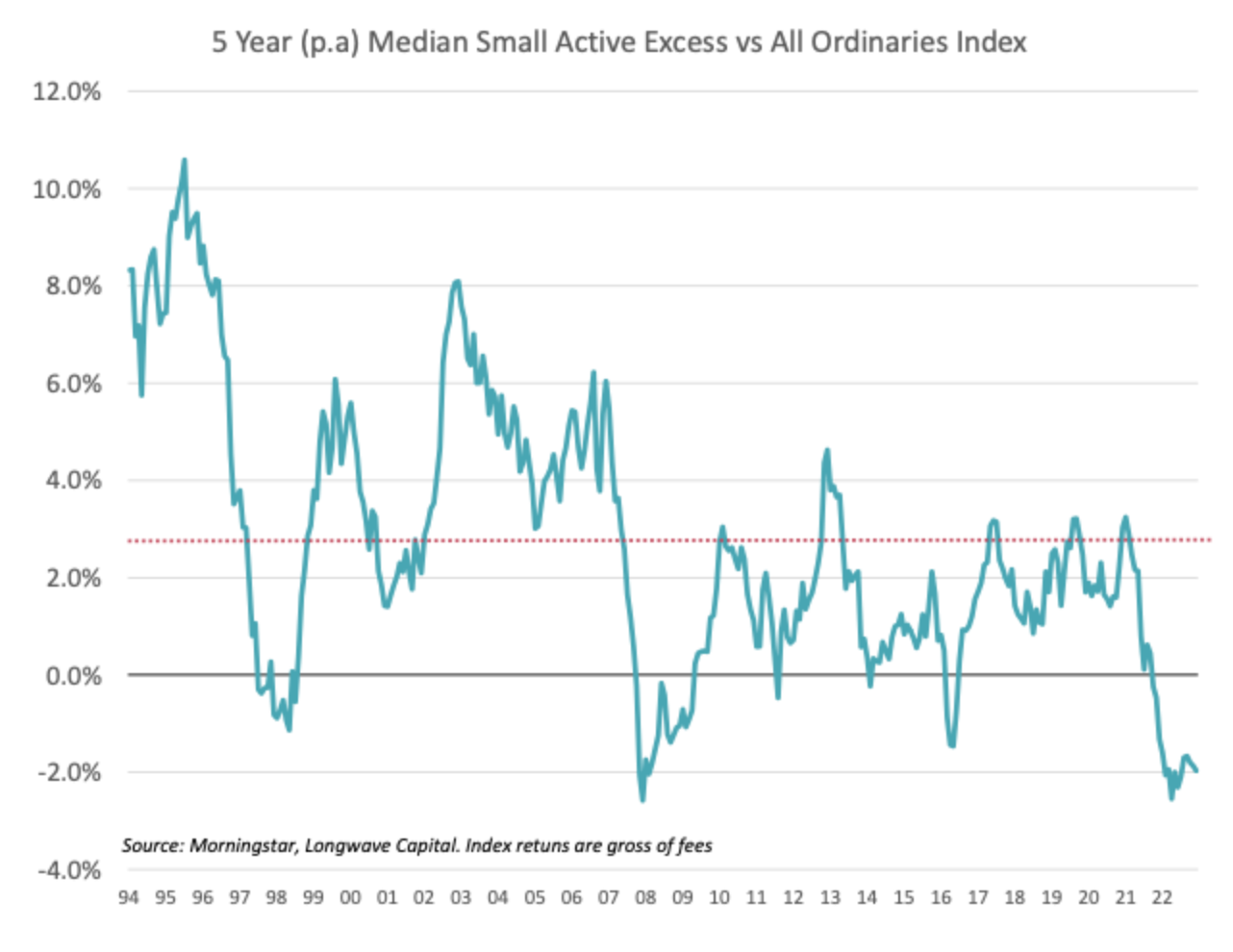

- Why active management works in small caps: Active management is under pressure in many parts of the market – and for good reason as the delivered performance hasn’t justified the fees. Small caps continue to be a part of the market where it really does pay to be active, and there are structural reasons why this will continue.

Source: Morningstar, Longwave Capital. Index returns are gross of fees.

- The importance of quality: Quality is a common term with a multitude of ways to be defined. This is a feature, not a bug.

- Human Behaviour and decision making: Artificial Intelligence (AI) captured the imagination of the world in 2023. Experience in the Chess world gives some clues how investors may best respond and integrate technology into fundamental investing.

- Mythbusting our way to higher long term returns with lower risk: The myths we specifically highlighted were:

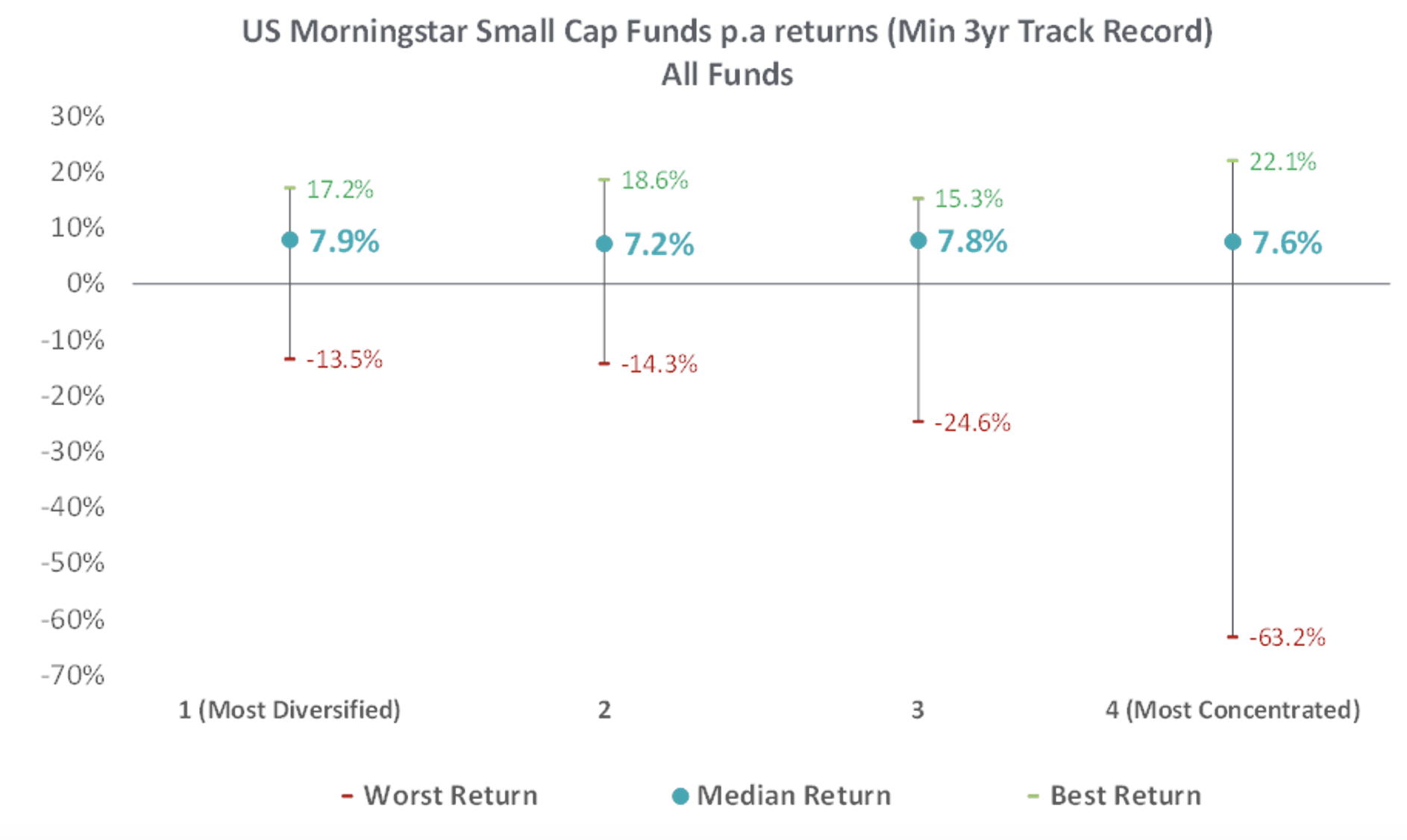

- More concentrated portfolios deliver better returns. This is one of the most persistent myths in funds management and it is just not true,

Source: Morningstar. U.S Database. Dec 1999 to July 2022. 632 total funds. Concentration measured by % of portfolio in 10 largest positions.

-

- High conviction is about low stock numbers,

Source: ASX Indices, Longwave Capital Partners

-

- Small Cap alpha only comes from Information Edge,

- Value, or Growth, is the factor that works best in Small Caps,

- Thematic investing is a short cut to high alpha in Small Caps.

Not easy but worthwhile

The worthwhile goal of active investment in Australian Small Caps is the superior long-term compounding of wealth that can be achieved. Activity for the sake of looking busy is one thing that feels like it should help but does not improve investment returns.

As a quality investor, looking to buy and hold companies that can compound value over the long term, our portfolio turnover is relatively low. Given we have not previously discussed this, we thought some numbers may illustrate what this looks like.

Our portfolio turnover in 2023 was 38% and while this was low by the standards of active small cap managers (average around 60%, with many above 80% per annum), it is also inflated by some factors outside our control. Every year we sell companies due to external factors that ordinarily (based upon the performance of the business) we would continue to hold. In 2023, 8.5% of our turnover was due to index changes (we are not allowed to own ASX100 stocks) and the delisting of the Janus Henderson CDI (forcing us to sell). 1.6% of our portfolio turned over from companies we own that were the subject of takeovers. We also have some portfolio turnover driven by changes in weight between companies in the portfolio due to changes in relative valuation appeal.

It is also worth noting that the underlying small cap index turnover is around 25% per annum, far higher than the 1-2% p.a turnover seen in an ASX300 ETF.

Name turnover – how many companies enter and exit the portfolio in a given year – was 26% in 2023, which was slightly higher than prior years, when it had averaged closer to 15-20%.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.