The Small Cap company lifecycle sweet spot

Small caps are different to other parts of the market partly because of where most small cap companies are in their company lifecycle. Many founders describe their businesses as ‘their children’ or ‘another child in the family’ and this is no accident. Businesses are literally ‘birthed’ from an idea on a sheet of paper. They evolve (sometimes fast, sometimes slowly) through early life-stages and into established businesses. Like children, they follow a common pattern of life-stages; they often learn by doing but learn different things at different stages of life.

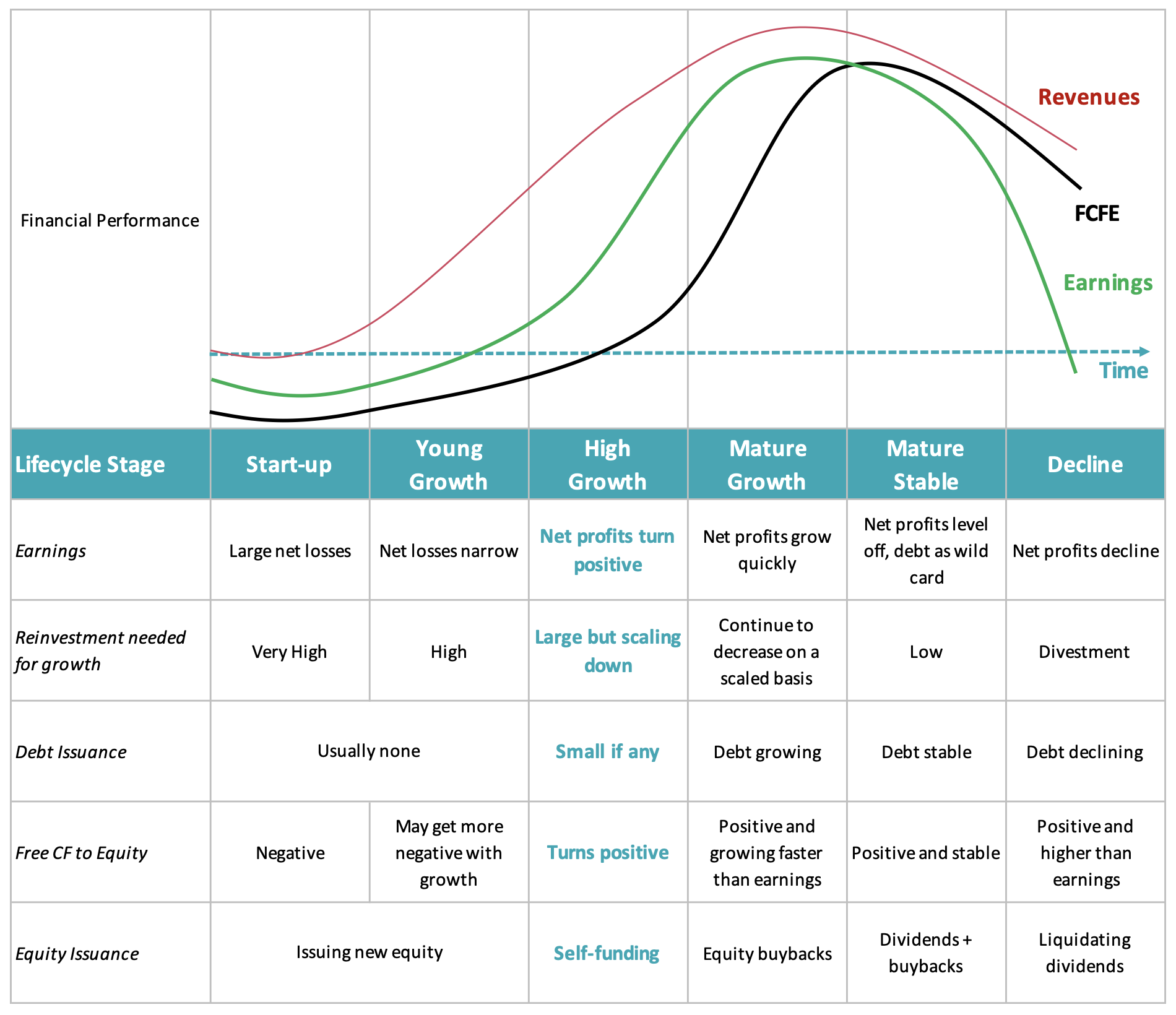

We think Damodaran’s framework of the six stages to a business’s life cycle is a helpful lens through which to look at small cap businesses. Very early in its evolution (Start-up phase) a business will be not much more than an idea that appears to meet an unmet customer need. The business reaches its “Young Growth” stage as it moves into a more defined business model and is starting to show real potential for future revenue and earnings. During the High Growth stage, the business is really hitting its stride and is firmly recognisable as a growth business. Stages 4 to 6 (Mature Growth, Mature stable and Decline) are characteristic of bigger corporations.

We can map Revenue, Earnings, Free cashflow, debt and equity issuance profiles onto the different life stages. ‘Startup” and Young Growth phases are characterised by none to minimal revenue and negative free cashflow. Businesses in this part of their lifecycle rely on the equity or debt markets for continued funding of their operations. Because the unit economics of their business aren’t yet proven, they’re more fragile on multiple different fronts. During the High Growth stage, unit economics are proven, revenue growth hits its stride and the free cashflow in the business is positive, allowing companies to reinvest in their growth. The Mature Growth phase sees slowing revenue growth, but a continuation in fast profit growth. At stability (Mature stable), a company will see a stabilisation of revenue and profit growth and due to lower re-investment requirements in the business, this stage is sometimes referred to as “cash cow”.

Source: Longwave and Aswath Damodaran

Source: Longwave and Aswath Damodaran

Numbers not narrative

Stocks in the small cap universe range from barely out of start-up phase to Decline stage. What makes small cap stocks fundamentally different, however, is the prevalence of businesses that are in the early and growth stages of their lifecycle. From an equity investors’ perspective, the very early stages (start-up and young growth) are characterised by high risk of failure or excessive dilution. Failure can come in many forms: unit economics can turn out to be entirely different to what was originally targeted, customer adoption may take a different path to what was forecast, equity or debt markets can suddenly close, requiring a complete strategic pivot.

There are other aspects of these early life-cycle stages that make small cap businesses fundamentally different to large-caps. Their underlying businesses tend to be less diversified. They may have weaker governance structures in the business, and they may still have founder owners who effectively control the company.

The unfortunate aspect of these earlier and more fragile life-cycle stages is that they are also the most exciting. Company founders in the very early lifecycle stages are compelling story tellers, and it’s easy to get carried away in the sophisticated and compelling narrative. Narrative investing is made all the more easy given the limited amount of observable information (profits) to verify the narrative against.

This fragility means investors in small-caps need to be particularly careful about controlling for risk of failure. What we’ve learnt over 25 years of investing in small caps is that despite the wonderful stories of early investments that pay off 10-times for their investors, as investors we get paid to wait until a business is in what we think of as the sweet spot of its lifecycle. This is when a business has already come through the very early stages of startup and young growth and has hit the point where they have the highest probability of survival along with the highest growth period in their business. This sweet spot corresponds to Damodaran’s High Growth life-cycle stage. Looking for characteristics in the financial statements of small cap companies that correspond to this life-cycle sweet spot, we think, helps control for some of the narrative investing bias that can easily creep into investment processes.

The time dilation effect in company lifecycle is real

Time dilation is the phenomenon where two objects moving through gravitational fields of different intensities experience different rates of time-flow. The concept is used to great effect in the movie Interstellar (we are fans). Just like the crew from Endurance, some companies move through their life stages very quickly and others move quite slowly. Just because a business was founded more than 20 years ago, doesn’t necessarily mean its automatically in its mature or decline lifecycle stage.

For instance, Austal Ships is a small cap stock founded 30 years ago that has slowly achieved a firm place in the US Navy continuous shipbuilding program. It has a low level of base profitability and a sizeable future growth profile from its forward order book with the US Navy.

Nothing wrong with cash cows at attractive prices

There are exceptions to the rule and our investment process allows the Longwave portfolio to hold more mature businesses. In a more diversified portfolio seeking to achieve more consistent alpha, there is a place for mature stable businesses with defendable strategic moats at attractive prices. For example, the opportunity to buy an asset like Auckland Airport at a price 25-30% below pre-pandemic levels, with the lowest leverage in 20 years (and while Sydney Airport was being taken private at very close to a record price) was a compelling opportunity we took in 2022.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.