Small Cap Myth Busting

– David Wanis, December 2022

As we look back on 2022, we remind investors not all beliefs they hold are true. We have highlighted some of the most common and strongly held small cap beliefs we encountered in our conversations with investors this year and why we think they may be wrong.

More Concentration = Higher Returns

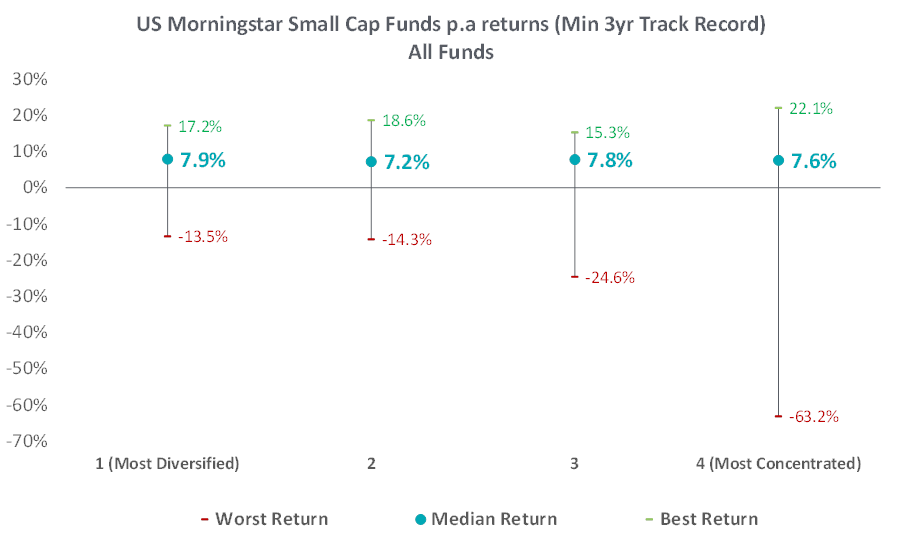

Beyond around 30 stocks the benefit to volatility of adding more stocks is limited. But the belief that this extends to a) risks beyond volatility – itself a poor measure of true risk and b) returns within the small cap universe is assumed, and in our view false. The belief in volatility reduction from more stocks translating to other outcomes is the closest thing we have seen to a Mandela Effect in equity markets.

We highlighted this empirically in 20 years of small cap fund returns analysis published in September this year.

Why broader portfolios can perform as well as more concentrated portfolios is driven by the positive skew in individual stock returns – which is even more pronounced in small caps than large. This means the median stock return is lower (sometimes much lower) than the average stock return. Index returns look more like the average due to their breadth. Concentrated portfolios, if they happen to miss the small number of big winners (or in small caps catch too many of the big losers), will fall short.

Source: Morningstar. U.S Database. Dec 1999 to July 2022. 632 total funds. Concentration measured by % of portfolio in 10 largest positions.

Investors can test this for themselves mathematically with a simple toy model, empirically observe it in fund returns (as above) or think about the way success and failure works in the real world. There are also many studies over more than 25 years confirming this effect.

High Conviction = Low Stock Numbers

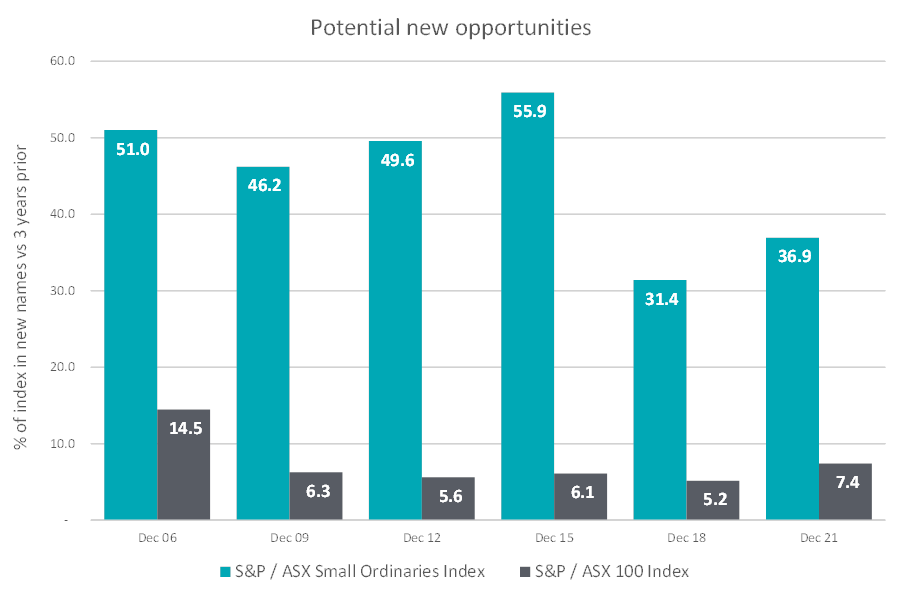

As small cap investors we have a very large potential investment universe to choose from – more than 1,000 stocks in most years and over 1,200 stocks today. This universe is far more dynamic (names entering and exiting) than the almost static large cap opportunity set (ASX100). We also work within a far more skewed universe – bigger winners and bigger losers. Finally, it is well known that broker stock coverage in small caps is much lower than large caps. This also extends to professional investors – where the ratio of investment analysts to individual stocks in large caps is 10-50x greater.

Source: Longwave Capital, S&P / ASX Indices

Small caps are different to large caps in many ways.

To us conviction is less about an arbitrary number of stocks in a portfolio, rather it reflects unwavering commitment to our quality investment philosophy. We have the conviction to pass on more than 90% of stocks in our universe failing our quality hurdles. This can be painful at times (like mid 2020 to late 2021) when low quality, speculative investing was wildly popular. Conviction requires discipline to say no.

In order to capture long term returns, conviction also requires a willingness to hold companies as they compound over many years (patience) and be willing to sell holdings when the investment thesis breaks and we are wrong (humility).

In our view, a 100 quality stock portfolio, deliberately selected and actively managed from 1,200 opportunities can be higher conviction than 30 stocks selected from the ASX 100. Given more concentrated small cap portfolios have other downsides and no higher returns, we wonder what we are really missing by not holding fewer names?

Small Cap Alpha only comes from Informational Edge

Investment edge comes in many forms, as we discussed in October using the Behavioural, Analytical, Informational and Technical (BAIT) framework.

All small cap investing edge is informational remains a persistent myth. More company meetings = more alpha. More broker meetings = more alpha. More conferences = more alpha. We believe alpha should be sought from all sources of edge, and often those overlooked – such as behavioural edges – can be more durable.

2022 highlighted ignored behavioural or analytical considerations had built up in many investor portfolios during 2020 and 2021 and the adjustment this year was painful.

Value or Growth is the driver of long-term investment performance

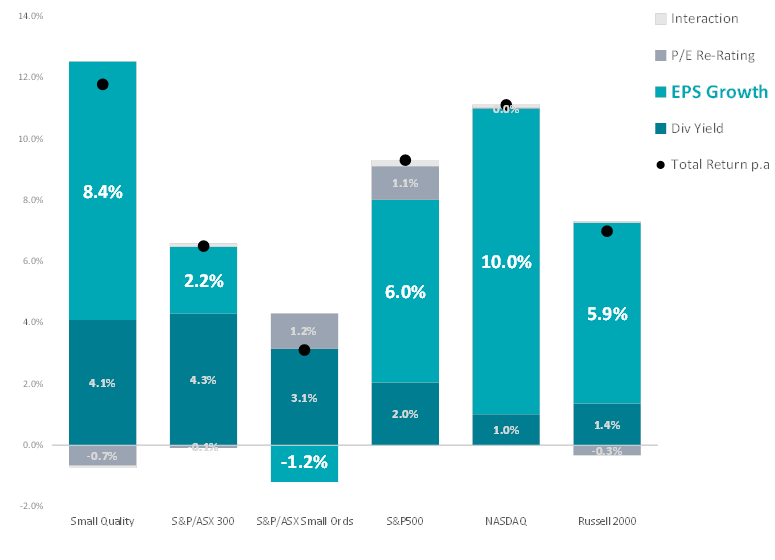

Value and growth are labels used to cluster the temporary character of stocks and the styles of fund managers who hold them. A whole industry forever tries to figure out which is better – or which is better right now. In reality, long term returns are driven by the fundamental performance delivered by businesses – EPS growth and dividend yield. Changes in valuation or P/E multiples – which is most of what value vs growth is about – is a total sideshow. Investors in equities should be investing for at least five years, by which time the noise from value or growth has likely cancelled out and only fundamental return drivers remain.

Rather than value or growth, quality is our laser focus and conviction in small cap investing. It is quality that delivers demonstrably superior long term EPS growth and over the past 15-20 years higher dividend yields as well.

Source: Mar 2006 to Nov 2022. Longwave Capital, Bloomberg

There are short cuts to big alpha

Every year there is a new fad – SaaS, crypto, green metals, SPACs, etc. Boring, proven approaches that work slowly but with high probability over time are overlooked. Real, profitable high-quality business. Cash flow. Strong balance sheet. No funny accounting. Shareholder friendly behaviour by management and directors. Reasonable valuation. Long holding periods. Low portfolio turnover. Humility. Low costs and fees. Humans are hard wired for stories which creates behavioural blind spots for investors due to the narrative fallacy. The seduction of narratives and themes is persistent.

Myths are widely held but false beliefs. We believe these five myths are either objectively false or have a high probability of being false. Beliefs are often so strongly held they are resistant to disconfirming evidence or facts. The beauty of strongly held but untrue ideas is they become a source of durable behavioural alpha for those that side with reality. Over the long run, the market prices reality – even if short run prices reflect narratives. Resistance means that most people who read our commentary as contrary to their existing beliefs will sooner dismiss our views than change. This is good news for us as long-term investors as our investment edge will likely remain intact.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.