The first five years at longwave

As we mark the five-year performance anniversary of the Longwave Australian Small Companies Fund, we review what we set out to achieve for our investors and how markets have evolved. Specifically:

Small caps are a valuable source of alpha in client portfolios; however, the index has been a poor way to capture this. We aim to deliver an outcome that allows investors to capture the long-term benefits of active small cap investing. Our goal was (and remains) to outperform the S&P / ASX Small Ordinaries Index and also outperform the median active manager (so second quartile of peers or better) through a 5 to 7 year investment cycle.

Although active small cap funds on average have delivered good results for investors (better than the small cap index, large cap index and large cap active managers), they almost universally build highly concentrated portfolios – either by stock numbers or by concentration to a theme, sector, or style. This results in a more volatile path of returns, delivering a wild ride for investors. Our goal was (and remains) to build more diversified and more robust portfolios which could deliver our performance goal in a wider range of market environments and reduce performance volatility.

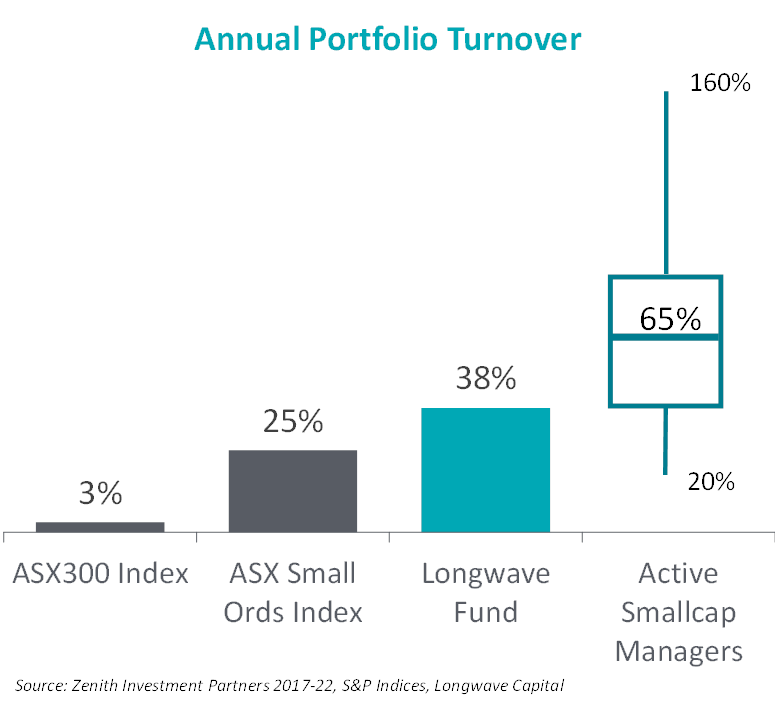

We also believe that what matters to investors in the long run are the net returns they realise. Net of fees. Net of taxes. Net of trading costs and commissions. Our goal here is to focus on long-term investing and the compounding of value from the companies we own, rather than furious trading activity trying to capture every wriggle in the market and timing the prices of individual stocks. This has meant our portfolio turnover of around 40% p.a is at the lower end of active small cap funds (that range between 20% and 160% with the average around 65% since 2017 – Source: Zenith Investment Partners). As we flagged last month, portfolio turnover is normally elevated in small cap funds due to the highly dynamic nature of the universe (new opportunities emerging) and the need to exit companies once they grow to a certain size in order to preserve the small cap focus and not drift up in the market cap spectrum. In Longwave’s case, that means selling our investments in companies within a reasonable time (six months) after they are promoted into the ASX100 and re-deploying those funds back into the small cap universe in search of the next generation of winners.

We believe our approach is helping to democratise the benefits of active small cap investing to a wider range of potential investors. Investors who have told us they haven’t invested in small caps due to the wild ride of performance. Or the excessive turnover. Or the high fees – which are increasingly in focus.

It is interesting to look back at the Longwave seed portfolio from 1 Feb 2019 and see how things have changed over that time. At inception:

- We held a diversified portfolio of 94 stocks,

- Our largest sector over weights were Consumer Discretionary and Materials, and our largest under weights were Real Estate (which we tend to be underweight in most market environments) and Industrials,

- Our portfolio had a higher ROE and lower leverage than the small cap index, but traded on a similar P/E ratio with a lower EV/EBITDA,

- Around 10% of the original portfolio was exited through takeovers,

- Of those companies still listed, 31% of the original portfolio has since been promoted to the ASX100 and as such is no longer part of our investment universe or portfolio,

- Many of the big winners from 2019 are still part of our portfolio today – companies such as Super Retail Group (+200% total return from 1 Feb 2019 to 31 Jan 2024), CSR (+220%), PWR Holdings (+240%), Nick Scali (+240%), Lovisa (+290%) and Pro Medicus (+720%) – although we suspect Pro Medicus will head into the ASX100 in 2024,

- Of course, it wasn’t all plain sailing, and a number of stocks didn’t do so well, although of the disastrous performers (such as Appen, Platinum Asset Mgt, St Barbara, Bravura, Cooper Energy) we exited most along the way.

Investors get conflicting messages on how to handle winners and losers in a portfolio. On the one hand, we are counselled to be price sensitive as if there is an absolute law of price reversion which leads to advice like ‘buy-low and sell high’ and ‘If you liked it at $1 you must love it at $0.50’. On the other hand, we are told ‘losers average losers’ and to ‘let your winners run’. The reality is that it depends. Not a very satisfying answer – but a lot of investing is like that.

Peter Lynch said it best “Some people automatically sell the “winners”—stocks that go up—and hold on to their “losers”—stocks that go down—which is about as sensible as pulling out the flowers and watering the weeds. Others automatically sell their losers and hold on to their winners, which doesn’t work out much better. Both strategies fail because they’re tied to the current movement of the stock price as an indicator of the company’s fundamental value.”

Action bias

We have written many times about behavioural biases that underpin a lot of alpha available in markets, and Action Bias is yet another. Investors feel like they are exerting control and reducing uncertainty by ‘doing something’ in their portfolio. It could be in response to their internal research, or it could be in reaction to a company event. It could originate internally from the investment team, or from other stakeholders.

A common interaction we have in communicating an unfortunate near term development in a portfolio company to clients, researchers and consultants is the question “what are you DOING about it?” Even long-term compounders, that ultimately win for their investors over time, face near term setbacks. Excluding COVID, every one of the six winning stocks we highlighted above had business issues and share price drawdowns of at least 40% over our holding period. Of course, buying more on these drawdowns is obvious in hindsight, and in some cases, we were smart enough to do that at the time as well, however sometimes the desire to DO SOMETHING can lead to selling on a short-term setback and missing the ultimate long-term gains.

There are lots of myths in investing and the need to be seen to DO SOMETHING – which is how portfolios end up with 150% per annum turnover – is one that doesn’t always benefit the performance of investors over the long run.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.