What the Apple iPhone tells us about small cap funds

In less than 20 years, the Apple iPhone has generated almost US$2 trillion in sales and over US$500 billion in operating profits. It is still selling at the rate of around US$300bn in sales per year.

If we go back to when the iPhone was introduced, the compelling feature of the iPhone, compared to all their competitors who were trying to crack the smartphone market, was the seamless integration of three key features into one device.

A widescreen iPod with touch controls, a revolutionary mobile phone and a breakthrough internet communications device. Three products in one, allowing users to get all these features in a single device. 17 years on, this seems obvious – but it was a revolution at the time when Blackberry and Nokia dominated the market.

What does this have to do with investing in small caps and small cap funds?

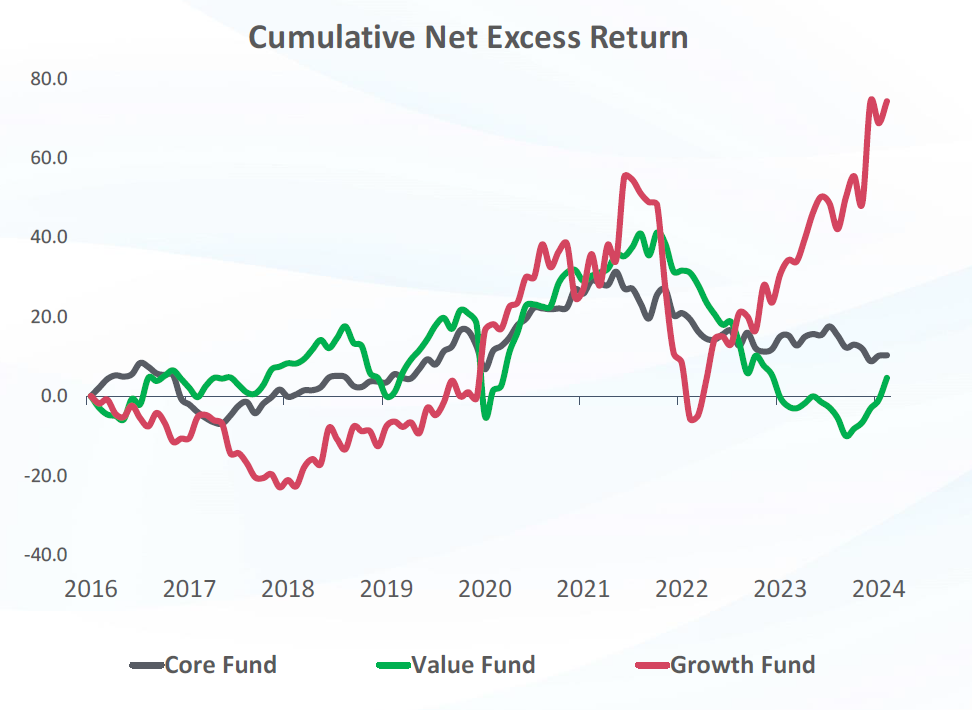

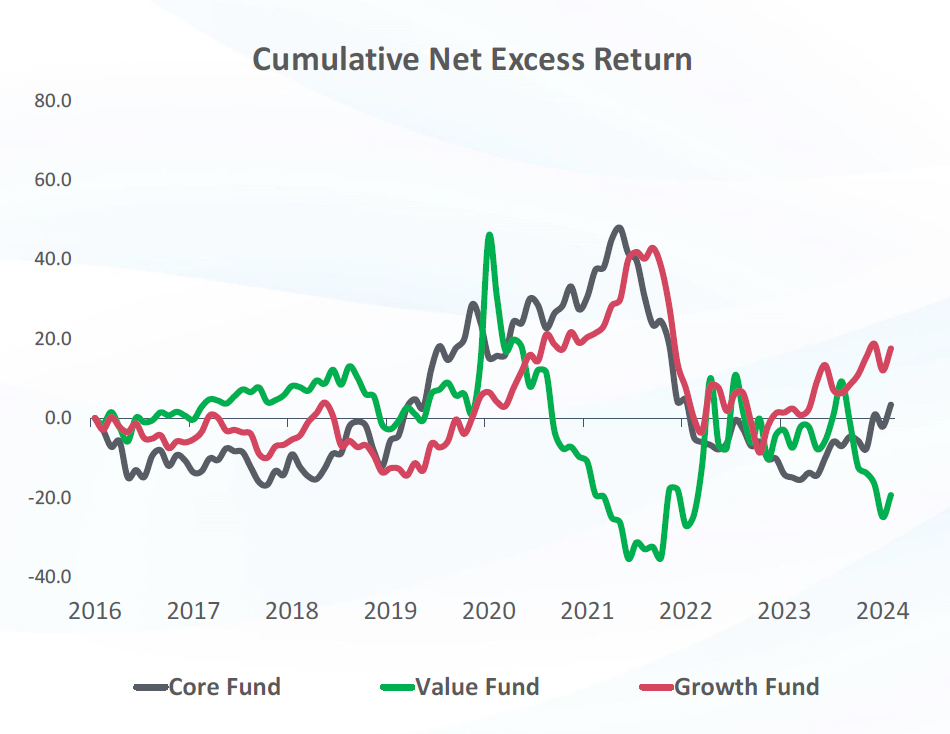

At Longwave, we often talk about the wild ride in small cap alpha. This is driven by two features of almost all small cap funds

- Concentration: it is accepted wisdom that to outperform you need a concentrated portfolio. 30 maybe 40 stocks maximum. This concentration – in a part of the market which is already very volatile – creates a wild ride for fund investors.

- Style and Sector Bias: funds often have a strict style bias which creates what the wonks call “regime dependence”. This means that value funds only outperform when value as a style is “working”. Same for growth funds. Same for funds which exclude or only invest in specific sectors (eg: only industrials, no resources).

Source: Morningstar (Fund), Bloomberg (Benchmark), Longwave Capital. June 2024.

We have met with hundreds of investors over the past five years, and the wild ride and episodic performance of small cap funds creates real problems for them and their clients. The most common feedback we hear on the asset class is:

“A volatile small cap fund means I spend half of my annual client meeting discussing a fund that is less than 5% of the portfolio”

“As my clients approach retirement, consistency becomes more important than the highest returns”

“I only want one or two small cap funds for my client portfolios. I don’t have the time to blend multiple managers”

“The fees on small cap funds are too high”

Source: Morningstar (Fund), Bloomberg (Benchmark), Longwave Capital. June 2024.

At Longwave we are focused on more consistent alpha at lower fees to help solve these challenges.

How do we do this?

By combining three key features into a single, integrated, diversified and risk managed fund. You can think of Longwave as a CORE fund and a VALUE fund and a GROWTH fund all in one. Like the iPhone, we believe the benefits of taking a novel approach to small caps are compelling to the end users – regardless of what current industry standards are. We push back on the idea of concentration and single style investing being the only way.

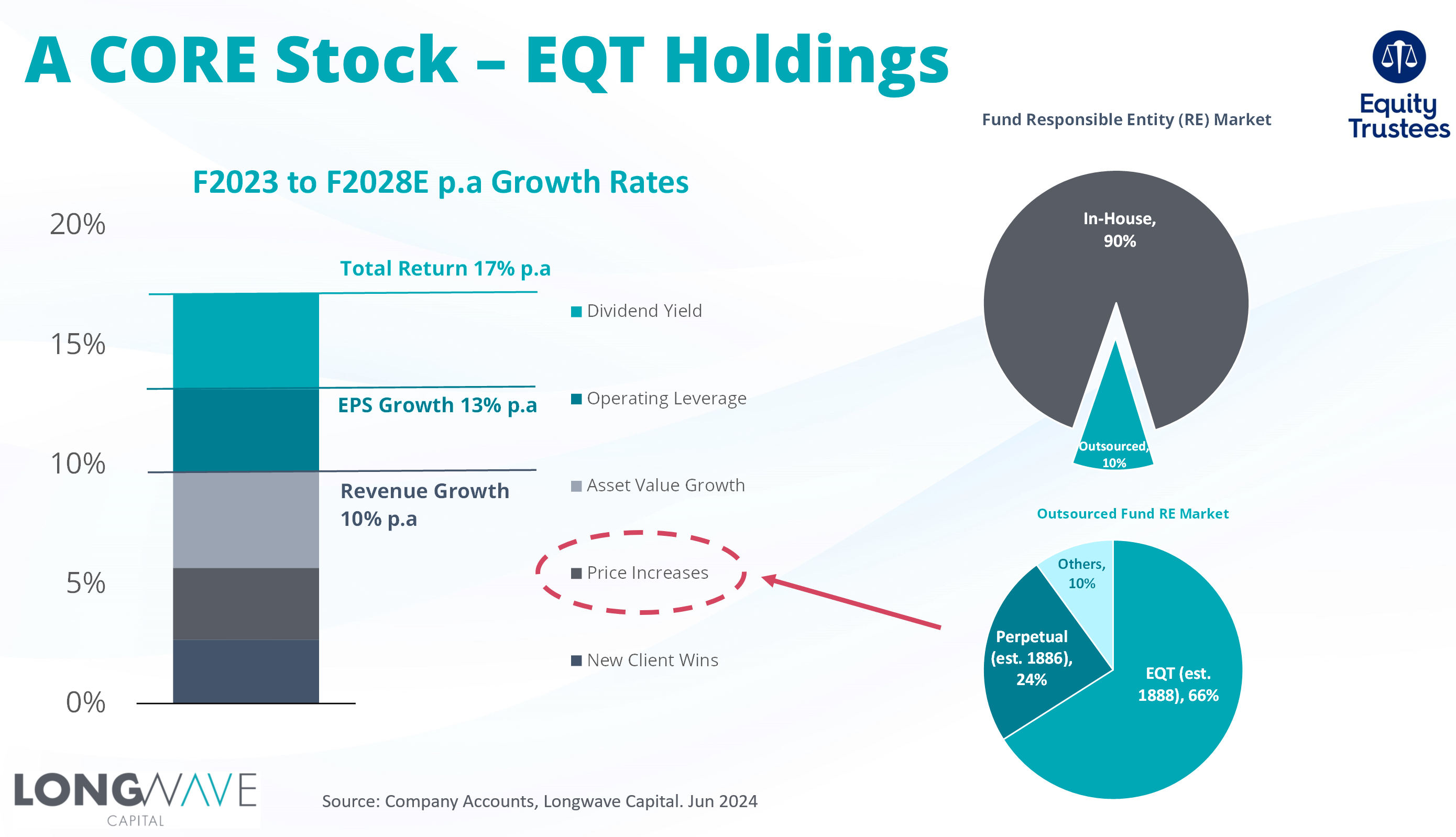

So what are CORE stocks? We think of core stocks as strong franchises with solid growth, often available at reasonable value. EQT Holdings – better known as Equity Trustees – is an example of a core franchise we hold in the portfolio today.

They have several business lines, but one of their oldest and most valuable is the provision of Responsible Entity (RE) services to both superannuation funds and public offer managed investment schemes. Now only 10% of this market is outsourced, but for those funds that rely on outsourced RE services, EQT and Perpetual have 90% of the market between them.

How does this translate into solid returns for investors? Let’s build up where we think returns will come from in the next five years:

Firstly, new client wins. EQT is growing market share across their business lines. Secondly price increases. We have a modest increase in prices assumed but the duopoly market structure means that price increases are put through at above CPI level in most years. Finally at the revenue level, growth in asset values – as some of the EQT fees are linked to funds under management. This can be volatile with market levels but tends to grow over time.

These drivers underpin around 10% per annum revenue growth. For earnings, we then have the benefit of operating leverage or margin expansion. Some of this comes from the synergies from the recently acquired AET business, and some from growing costs at lower than the 10% p.a revenue growth. This combines to give us low double digit EPS growth.

Finally dividends. EQT requires little capital to grow organically and can payout free cash flow as dividends. Adding a 4% p.a dividend yield results in a total annual return of around 15-17% per annum.

VALUE stocks are probably more familiar. Stocks that are out of favour, cyclically depressed or businesses in need of a turn-around. Often the upside is not obvious and requires some digging to uncover.

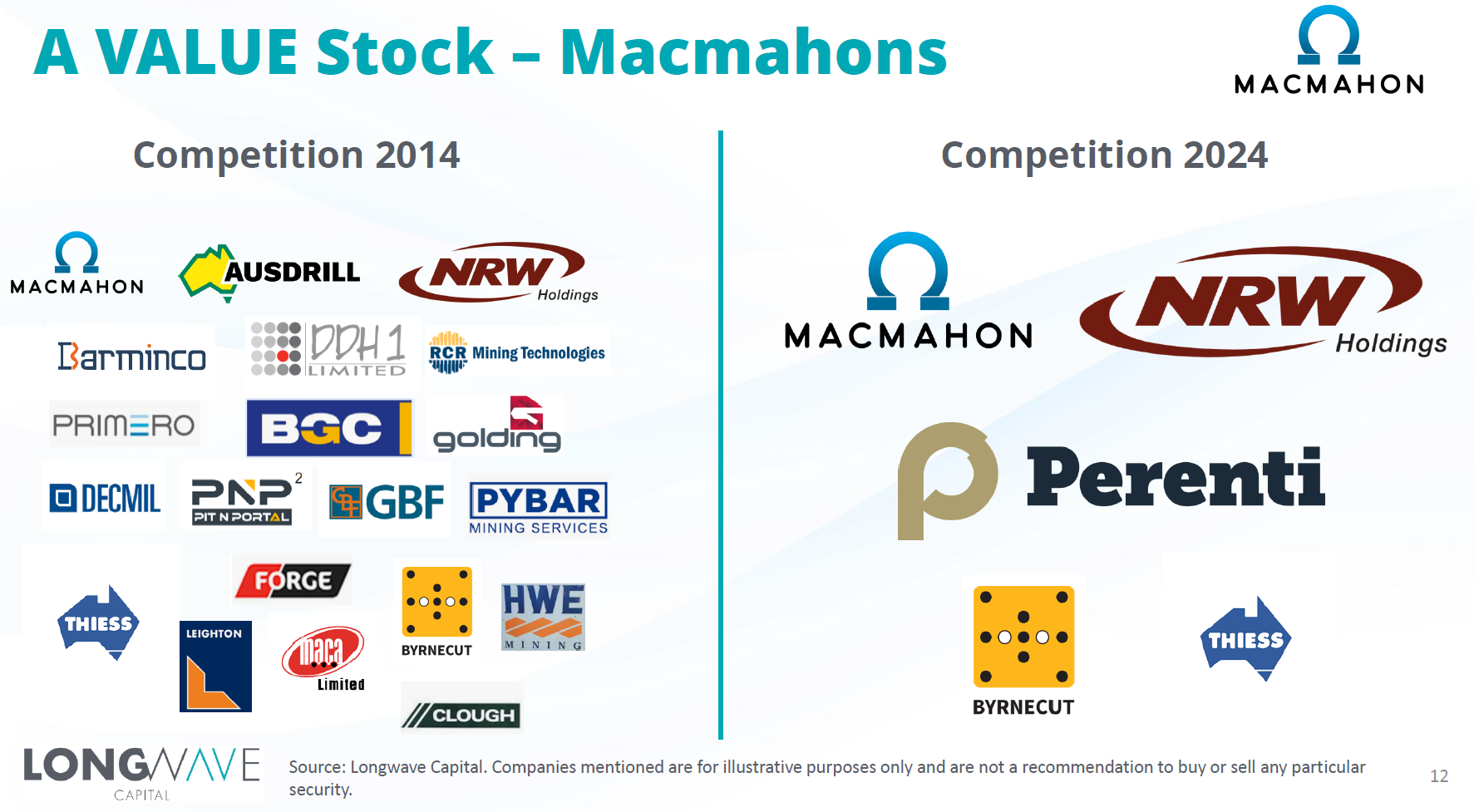

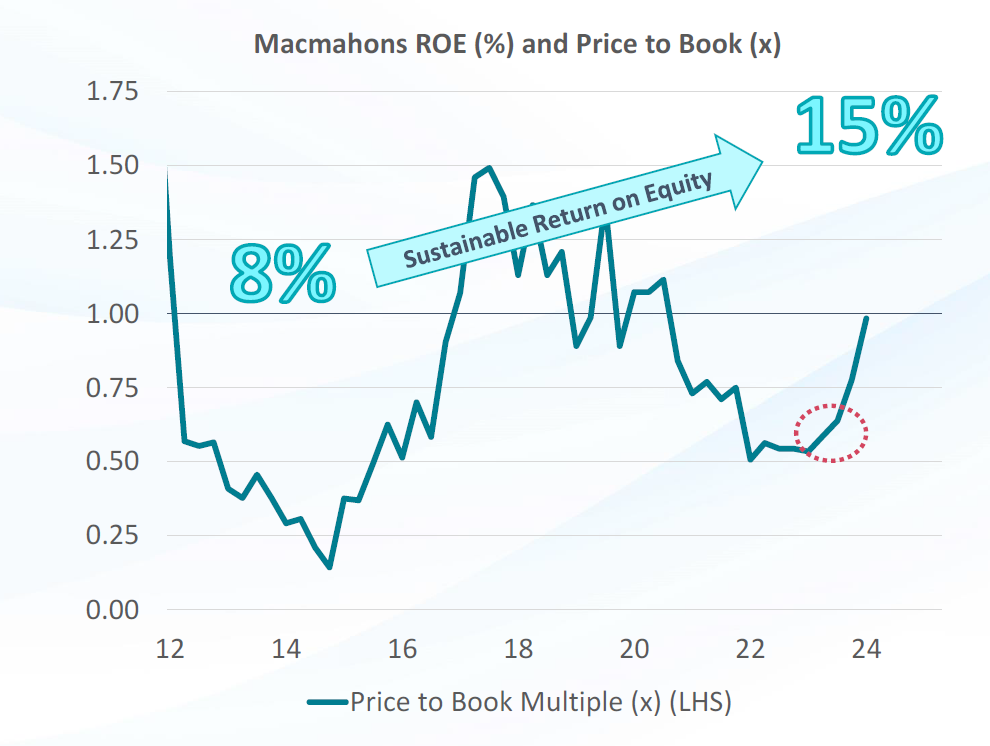

Before we talk about a value stock – Macmahon Holdings – we need to talk about how the contract mining (surface and underground) industry in which they compete has changed. A decade ago, as the mining boom was coming back to earth, the industry was a complete mess, left with intense levels of competition. Many companies competing for a declining level of work. This meant that return on capital for almost all players was low – below the cost of capital – and volatile.

This was not sustainable and over the subsequent decade we saw a consolidation in competitors from 20+ to 5-6.

What this has meant for Macmahons – who was active in the consolidation activity – is greater bargaining power over customers and most importantly for Macmahon shareholders the prospect of higher sustainable returns on equity. Macmahons is cyclical, had been out of favour for many years and an industry turnaround was underway. To us, this meant that the stock trading at 50% of book value in 2023 was too cheap and Macmahon represented a compelling value opportunity.

Source: Company Accounts, Longwave Capital. June 2024.

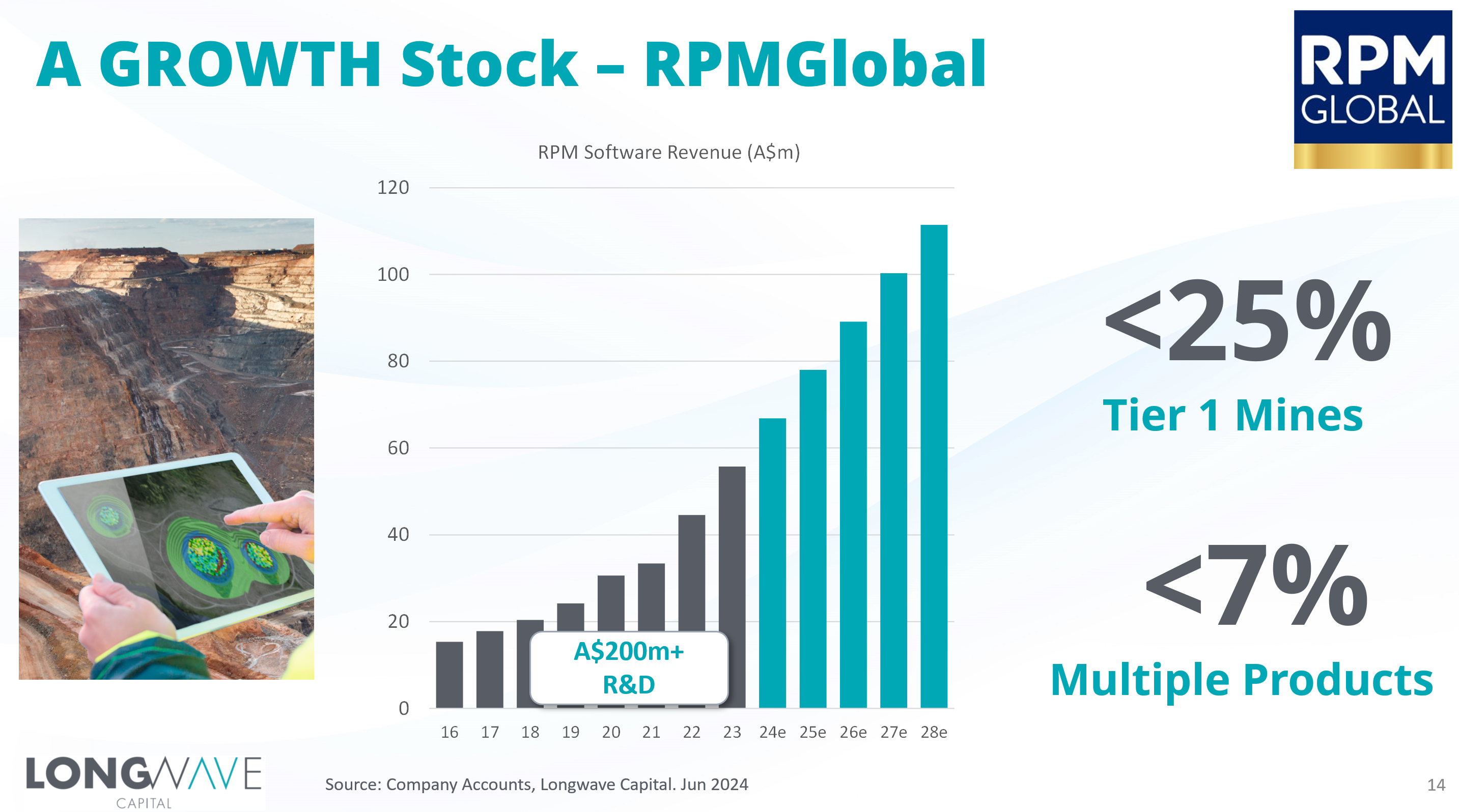

And finally, GROWTH stocks. All anyone seems to want to talk about these days. Companies that have a long runway of strong growth, often into global markets. Longwave only invest in growth stocks that are proven and growing profitably, not thematic or speculative stocks. RPMGlobal is a provider of software products to the mining industry. They aim to cover all the business critical functions such as mine planning, asset maintenance, commodity production and delivery. RPM have spent over A$200m in R&D building a suite of software products tailored to the needs of mining companies. They have had terrific success in the past 8 years and have grown quickly, however the longer term still looks promising. Less than 25% of Tier 1 mines currently use their software. RPM believes all Tier 1 (and many tier 2 and 3) mining companies are prospective customers.

And like Microsoft, once you start using one application, you are more likely to use the same vendor across many connected workflows. Today, less than 7% of their customers are using more than one product from RPM.

Longwave constructs an All-Weather, diversified and risk-controlled approach that combines the benefits of CORE, VALUE and GROWTH in a single lower cost fund.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.