Average is scarce in the stock selection process

Active investors want to do better than average. Index investors are happy with average, at a low cost. What may be lost along the way is just how scarce average is in the stock selection process. Active investors are always looking for unicorns. Maybe not billion-dollar concept stocks in 2023 – but listed companies that possess a combination of multiple attractive traits. High quality business. Strong balance sheet. Capable management, with integrity. High growth and of course a cheap valuation.

This describes most investment processes – with different investment styles emphasising different attributes as being the most important. But how common are these stocks? What is the base rate at which we can expect to find companies with the best of all these attributes? What about just being average or above?

If each of the five traits (business quality, financial robustness, management, growth, value) are independent, and assuming we just want companies that are average or better in each category, what are the odds a company is average or better, (say in the top 50%) in all five?

3%.

3.125% to be exact is the number of companies likely to meet that test (50%5).

An investor who follows this rigorous, benchmark unconstrained process and starts with a universe of 200 names should end up with a portfolio of about six stocks. Six stocks which are simply average or better across all five attributes. How do we get to a portfolio of 30 stocks? We either need to expand our universe of potential candidates (to 1,000) or reduce the number of attributes we care about. There are other approaches, but these are the most obvious two.

We think investors would find these numbers unintuitive. How rare it is to find companies who are just average or better – but across multiple dimensions. It indicates trade-offs investors must be making, when building concentrated portfolios within the S&P/ASX 200 universe. Seeking even higher hurdles in any attributes will dramatically shrink the population that passes the test.

3% was just to be average or better. Which of course most active managers don’t want. They want the best. The highest quality business, with the best balance sheet, run by superb, highly aligned management who can grow fast. And it needs to be purchased below fair value.

So if we only want companies in the top quartile across all of these attributes, what are the base rates? Well if we start with 10,000 opportunities, 10 will pass the test.

0.1%.

This also assumes that we can determine these attributes to be true in advance. That we don’t mistakenly believe that a company is in the top 25% which turns out to be worse. That top quartile management don’t leave. Importantly in small caps, it also assumes that the Cambrian process of natural selection for commercial fitness in emerging industries can be accurately forecast. We do not believe this is realistic with anything like the accuracy needed to pick 10 small cap stocks out of 10,000.

We observe the reality of investing in small caps is the process by which new winners emerge. The process in many ways mirrors the biology of undirected variation and evolution rather than the outcome of intentional design or directed evolution.

Source: Blackstar Funds.

Natural selection: mutation – fitness – amplification

Evolution by natural selection occurs when random mutations meet the current environment and those poorly suited for fitness (adaptability to the environment) fail to reproduce. Those characteristics passed on become amplified in subsequent generations. The process here is randomness, exposure to reality and failure. Evolution is not a process of positive attributes being actively selected, it is a negative process of unfit attributes being selected out and what remains amplified.

New businesses tend to go through a similar process. Tens of thousands of enterprises are started. Most fail to be fit for the public market. Even then, of the 1,000 plus Australian small cap stocks, hundreds will fail. Either actually fail (receivership) or fail to achieve an acceptable return on capital invested.

Nice theory. What does reality show?

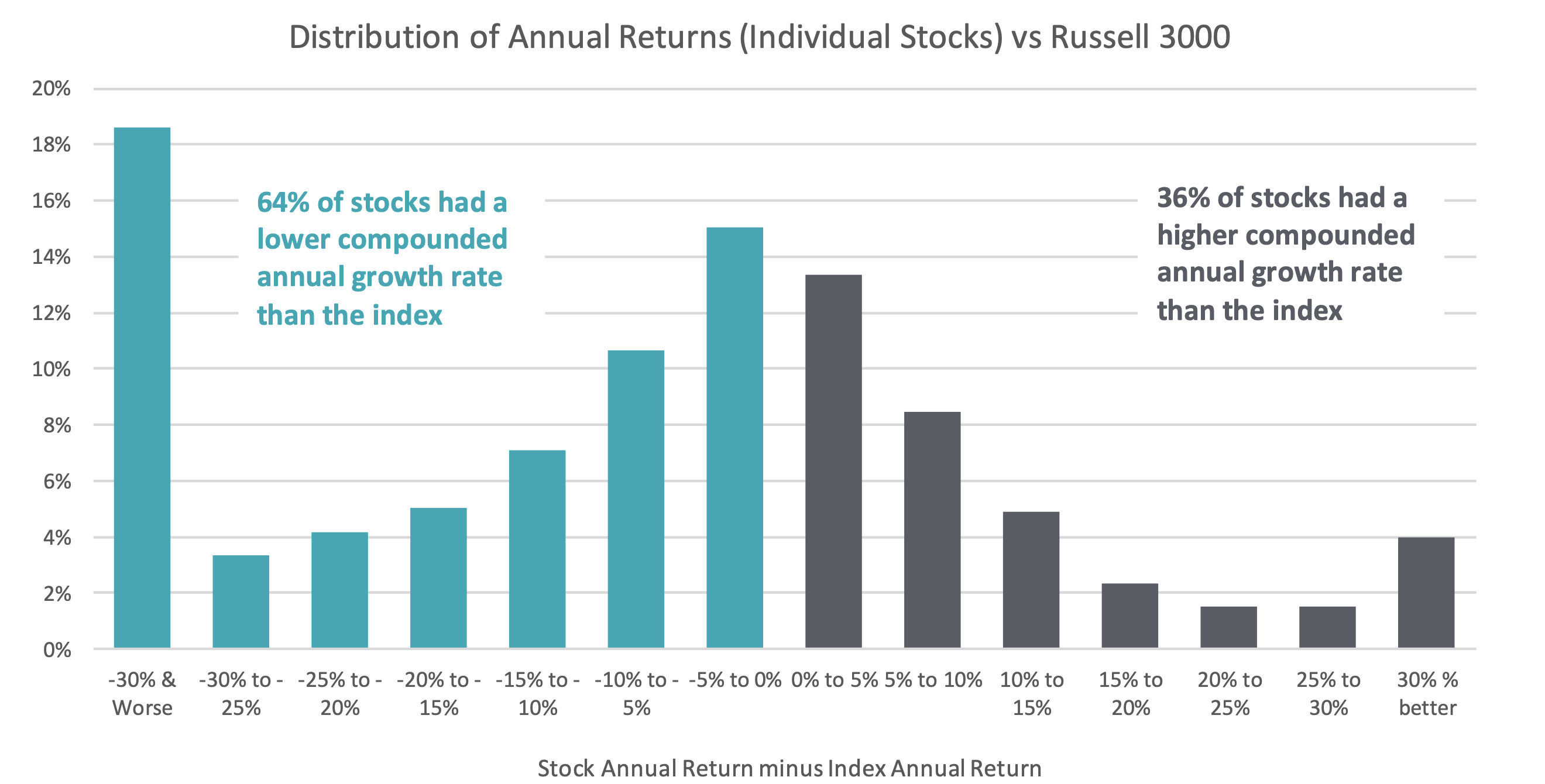

One way of seeing the small cap evolutionary struggle is to look at the skew of stock returns. It was a surprise to many when Hendrick Bessembinder demonstrated that positive skew meant the median US stock underperformed US treasuries, despite the total stock index (the average) doing significantly better. It gets even more exaggerated when you look at US small cap stocks. The median lifetime returns of the bottom third of the US market cap is actually negative, despite small cap indices doing very well.

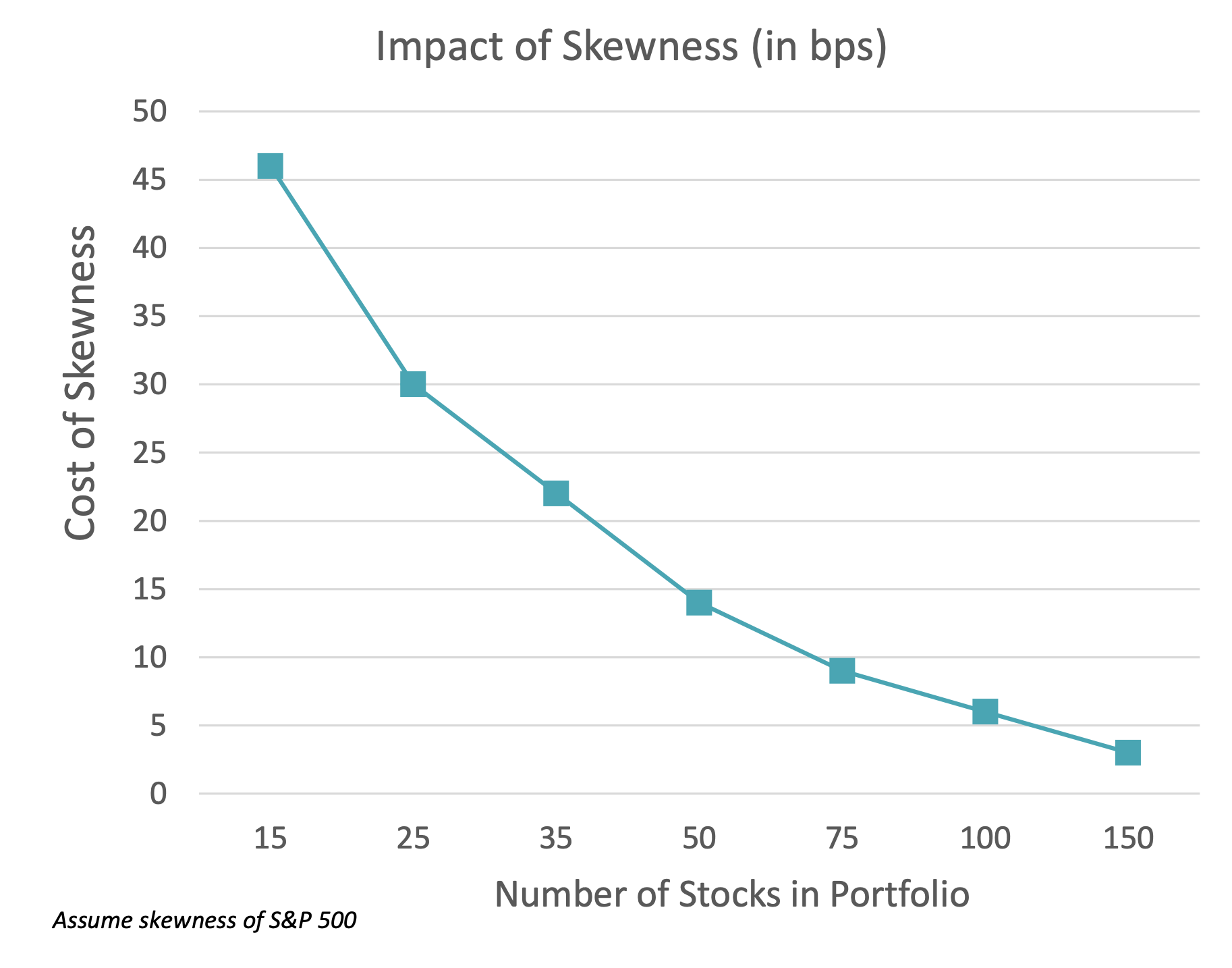

The skew in individual stock returns has been known for a long time but is rarely discussed. One implication is skew imparts a cost to concentrated portfolios, which reduces as the size of the portfolio increases. A 1998 study (Ikenberry, Shockley and Womack. The Journal of Wealth Management) demonstrated that a 25-stock portfolio in the S&P 500 carries around 30bps per annum in skew-based performance drag. This reduces to around 5bps at 100 stocks. Given the higher skew, concentration drag is likely to be greater in small caps.

Escaping the small cap commercial primordial soup is hard and the few big winners deliver all the investment performance.

Source: Ikenberry, Shockley and Womack. The Journal of Wealth Management. 1998.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.