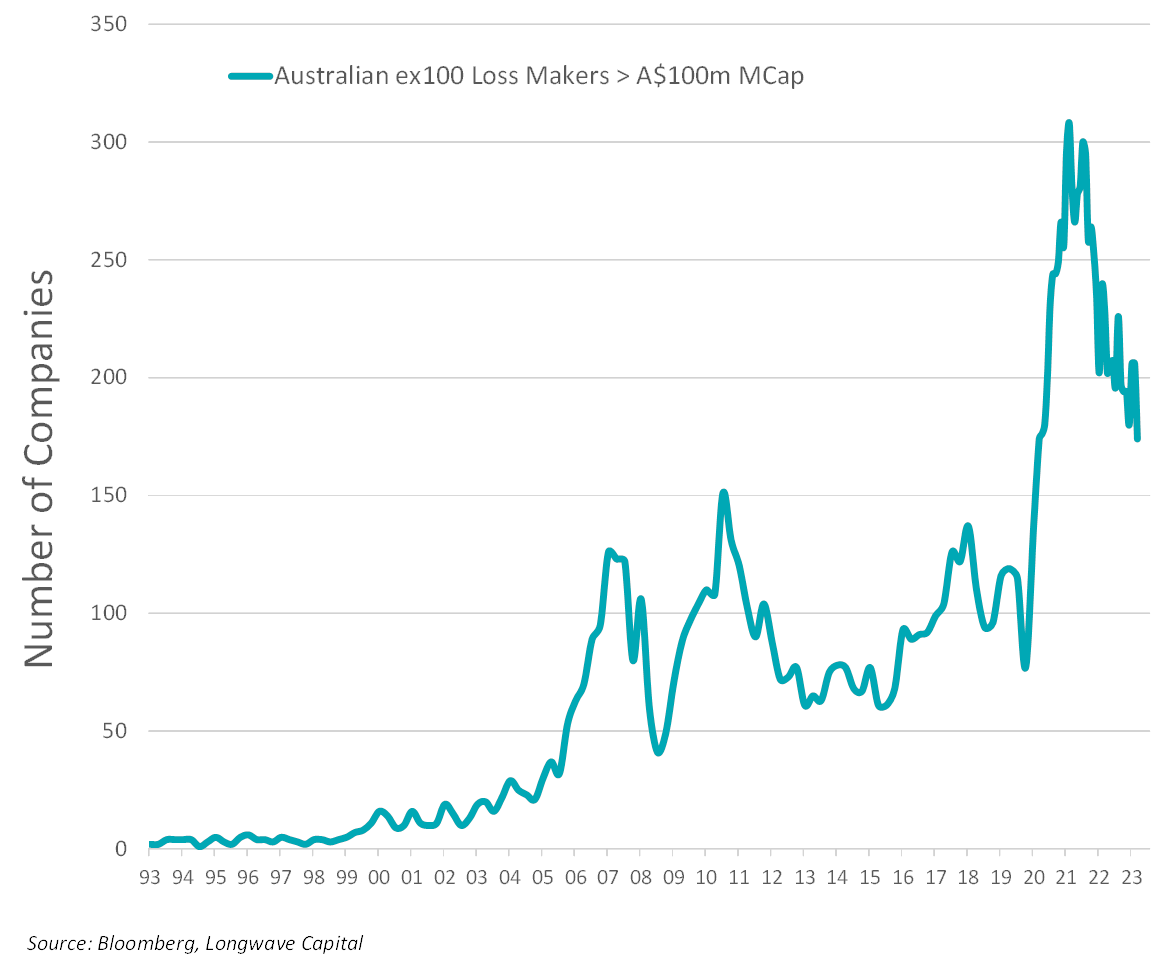

The death of magical thinking

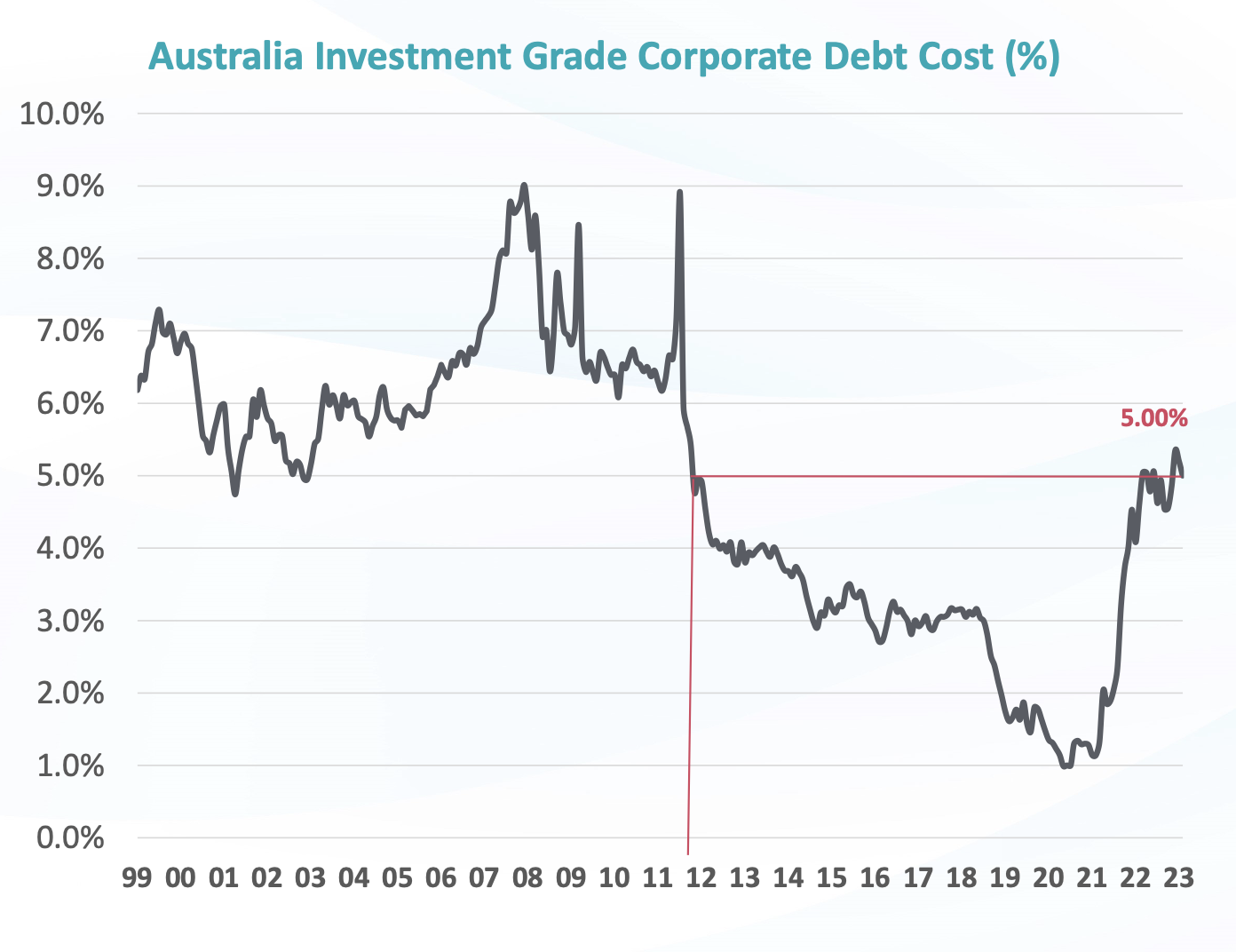

Magical thinking has died for one simple reason: the cost of capital. For more than a decade, interest rates had been declining. Debt got close to being free only a couple of years ago.

And free money makes people believe in magic.

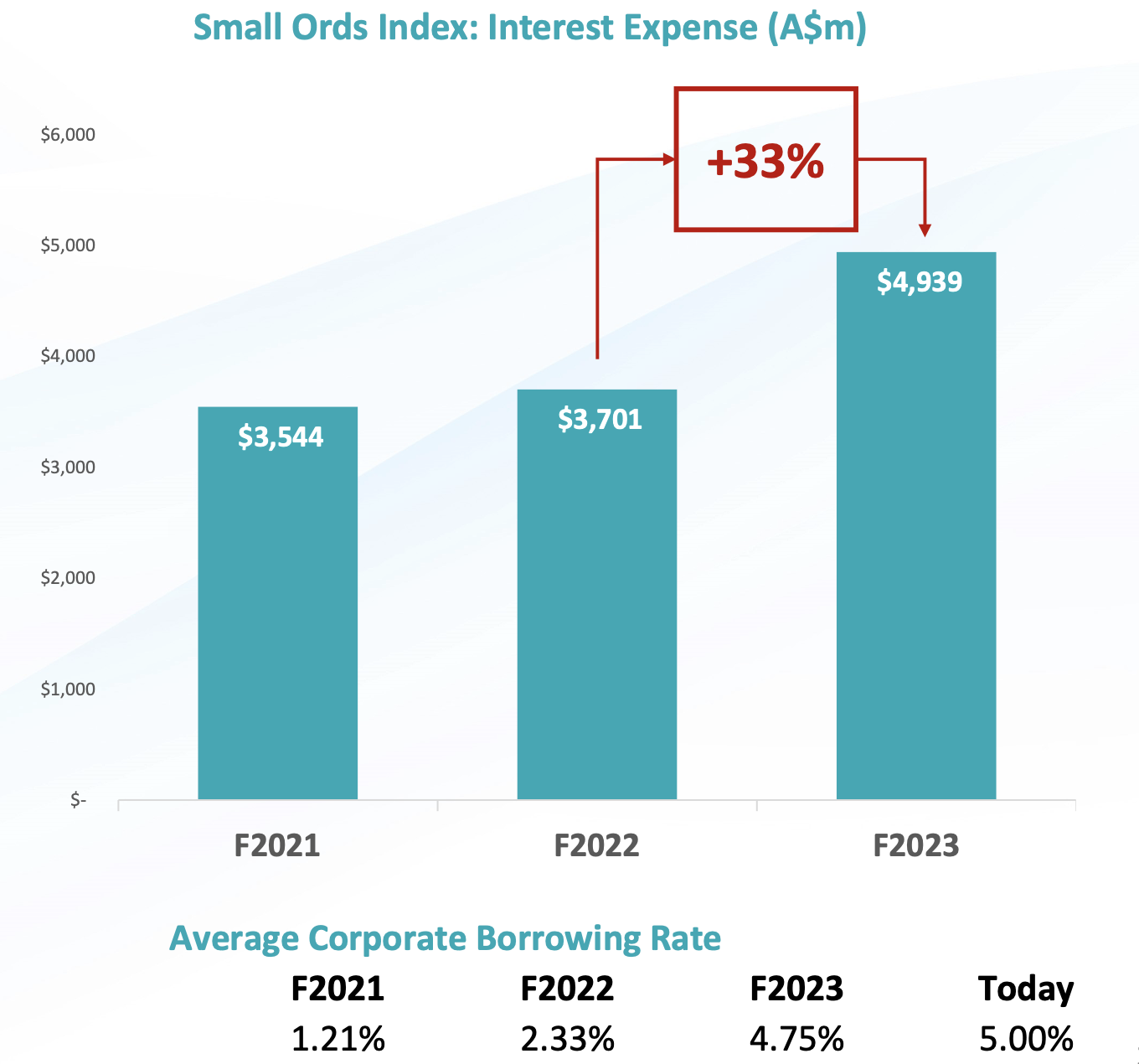

Source: Bloomberg, Longwave Capital.

We have seen a decade of speculation and financial engineering start to unwind in the space of two short years. In the financial year just reported, the interest expense bill was 33% – more than a billion dollars – higher for small caps in the index than it was in F2022. Historically, peak interest expense at listed companies happens around 12 months after official interest rates peak due to interest rate hedging and other lags in the system. Given where interest rates have been for the average of the past few financial years, and are currently above those levels, equity holders are going to give up more of their operating profits in the next year as well.

Reporting season gave us a good look at how companies across the market are performing. We estimate around 50% of the EPS downgrades through reporting season were due to higher expected interest costs and 50% due to slightly weaker operating conditions. Overall EPS downgrades were around 2% at the index level – hardly a recessionary outcome.

Reporting season observations

Impacts of higher interest rates: We saw many examples of higher interest rates in these results.

- Upward pressure on property cap rates (downward pressure on valuations) in the A-REITs, reversing a decade of upward revaluations,

- A number of A-REITs are also starting to flag leverage levels (debt to assets) approaching covenants. A tricky issue to resolve given their equity trades at a discount to NTA and asset values are likely to keep falling in many sectors,

- Small cap lending businesses may have benign customer defaults for now, but the impact on profitability of increased funding costs is anything but. As wholesale funding rates reset higher, and the RBA Term Funding Facility matures, the negative net interest margin impacts were flagged as significant in F24,

- Levered yield-based stocks such as NZ Telco infrastructure company Chorus (CNU), are hit on both sides, as higher interest expenses eat into the cash flow available for distributions and the yields they offer look less and less competitive relative to higher risk free interest rates. Chorus was also hit by inflation in their maintenance capex estimate – which was NZ$161m in F2022 and expected to be NZ$230m in F2024, further reducing cash flow for distributions.

Source: Bloomberg, Company Accounts, Longwave Capital. 31 August 2023

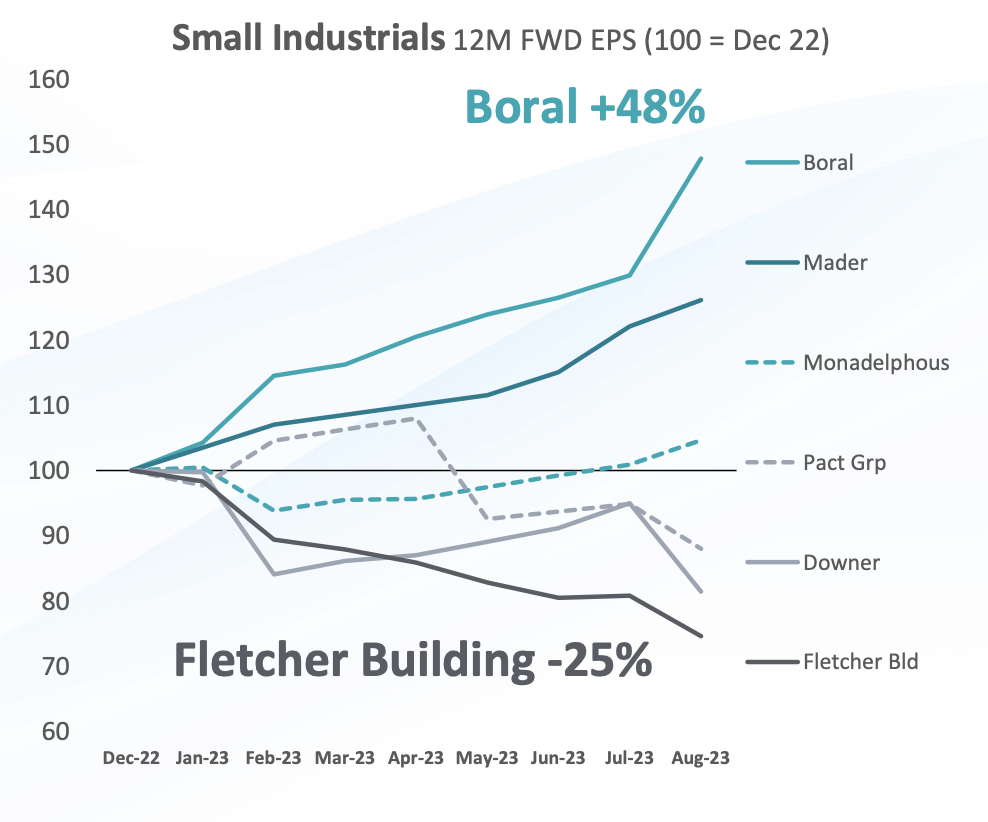

Management Execution: one of the starkest differences in management execution was the performance of Boral (BLD) relative to Fletcher Building (FBU). In order to get price increases to stick, significant management of sales teams is required and BLD delivered where FBU floundered. These execution differences are a large part of why Boral EPS estimates have been upgraded 48% so far this year and FBU have been downgraded by 25%. Unfortunately we own FBU and not BLD.

Source: Bloomberg Consensus EPS estimates: 31 Dec 2022 to 31 Aug 2023

Consumer Discretionary / Retail: a clear takeaway was the softening of the consumer, less so in many of the results reported (as relief from lower freight rates helped gross margins) rather in the more recent trading comments. Cost-of-doing-business inflation (aka wages) are going to be a challenge in F2024 if the consumer stays weak. Interesting comments from CBA and Qantas Frequent Flyer showed ostensibly where the weakness was most apparent (demographically in the 18-34 year olds, and sectorally in Beauty, Clothing and Homewares). But sometimes companies can out-execute the macro, and Lovisa (LOV), Super Retail (SUL) and Accent Group (AX1) all delivered solid results. Quality of earnings continues to deteriorate for market darling Breville Group (BRG), a risk not reflected in the share price.

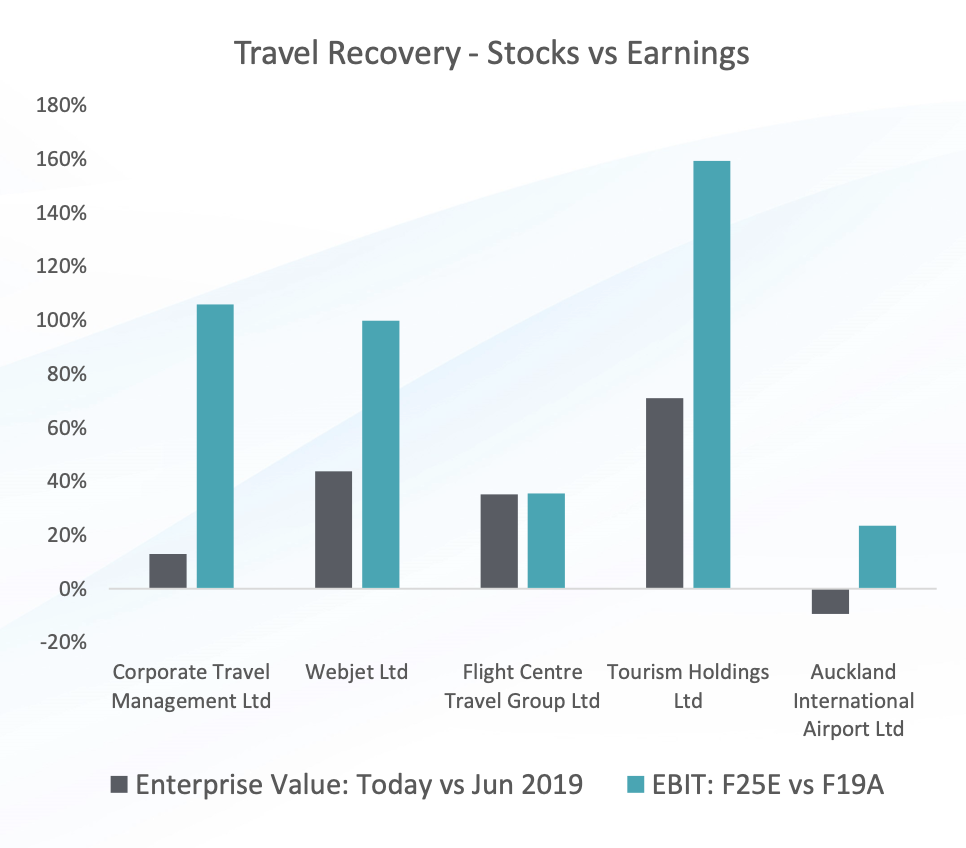

Tourism and Leisure: One area where spending remains robust, and intentions are also holding up, is in travel. Comments from Corporate Travel (CTD), Flight Centre (FLT), Tourism Holdings (THL) and Webjet (WEB) all supported the view that recovery to pre-pandemic spending levels is on track. For CTD, WEB and THL in particular, investments made when competitors were weak are paying off – with the market expecting F2025 earnings (EBIT) to be 100% or more higher than reported in F2019 for all three companies.

Source: Company Accounts, CapIQ Consensus Forecasts for F2025E (31 August 2023).

Technology: There were some promising examples of management getting costs under control and putting some of these businesses in a sustainable position. Probably most impressive was Megaport (MP1) but Life 360 (360), Redbubble (RBL) and Bravura (BVS) are all making progress. There are many other tech stocks – mostly microcaps these days – who are today a shadow of what they promised investors they would be in 2021. The magic for these companies is gone.

The biggest surprise to the market was IRESS (IRE), who finally revealed the true and parlous state of both the business and the balance sheet. It has taken new management 10 months to get their head around what is needed, and it is much worse than they thought in April when they last updated the market in detail. The list of issues within the business appears to be many: across product, technology, line of business focus (divestments now underway), carrying values and a stretched balance sheet. Management noted that paying dividends significantly greater than free cash flow and funding from increasing debt is not sustainable. Seems obvious but was rarely questioned in prior years. Enterprise software turnarounds (such as Bravura and Nuix), can take time to execute. What on the surface looks like a sticky, annuity business with pricing power can in distress uncover bad acquisitions, huge technical debt, bloated costs, and unsatisfied customers. Competitors (and there are always competitors) are acutely aware of the appeal of sticky annuity revenues and are ready with newer shinier offerings to win away business.

Source: Bloomberg Consensus EPS estimates: 31 Dec 2022 to 31 Aug 2023

The issues at IRESS have been building for many years, and Data Centre (DC) assets which underpin the businesses and market values of NextDC (NXT) and Macquarie Technology (MAQ) contain similar long term, unpriced risk. Data Centres are REITs in almost all forms but one – the risk of obsolescence. We learned last month that Scale (older DCs are too small), Cooling (AI GPUs need liquid cooling, which requires a different specification at construction of a DC) and Efficiency – known as Power Usage Effectiveness ratio (PUE) all conspire to make 10 year old Data Centres unable to participate in the current wave of Hyperscaler growth, and old Data Centres are likely to mature and decline far faster than any office building, shopping centre or industrial shed. For now the market is willing to look past this and pay 2-3x book value.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.