The Brutality of Smallcap Consumer Retail

Consistent with many small cap sectors, existential risk is ever present for retailers, and the best way to find the few opportunities that lead to outsized returns is to focus on the quality operators. Like Darwinian evolution, the hostile environment for new entrants can improve the longer-term returns for those that adapt and survive. Investment base rates are not favourable for small cap retail stocks. The base rates appear further skewed against retail turnarounds – despite the mirage of significant valuation appeal and potential upside if they work.

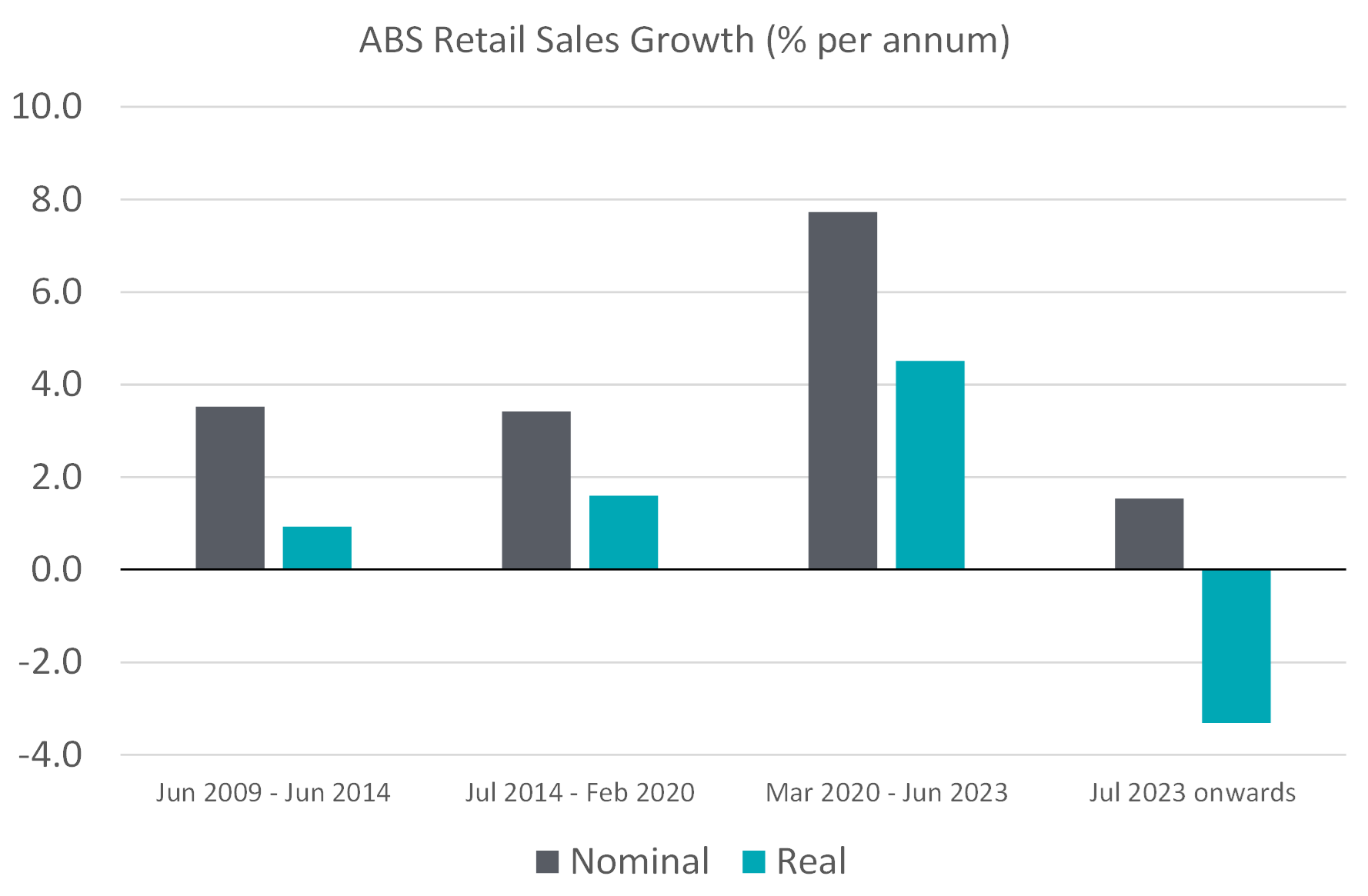

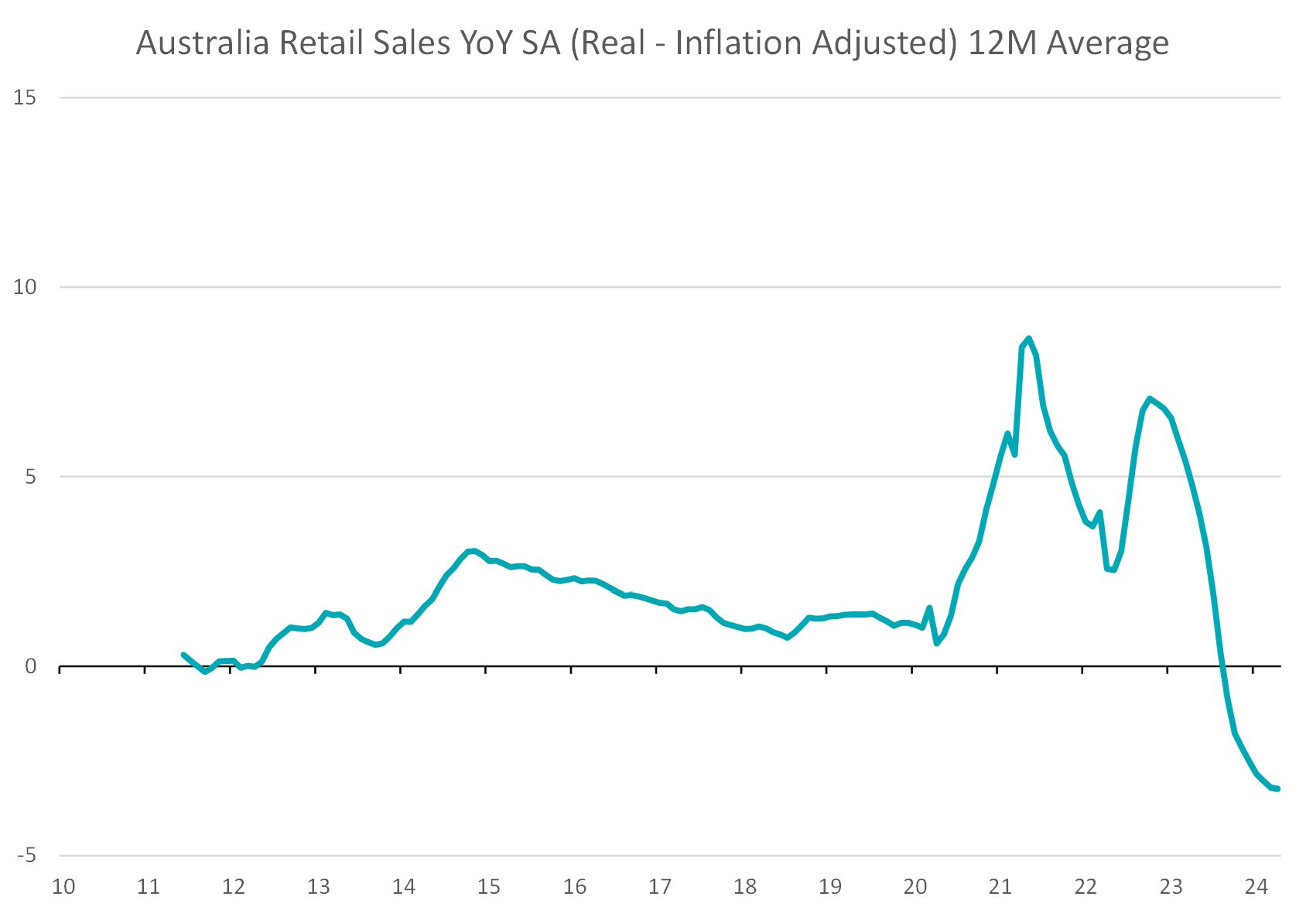

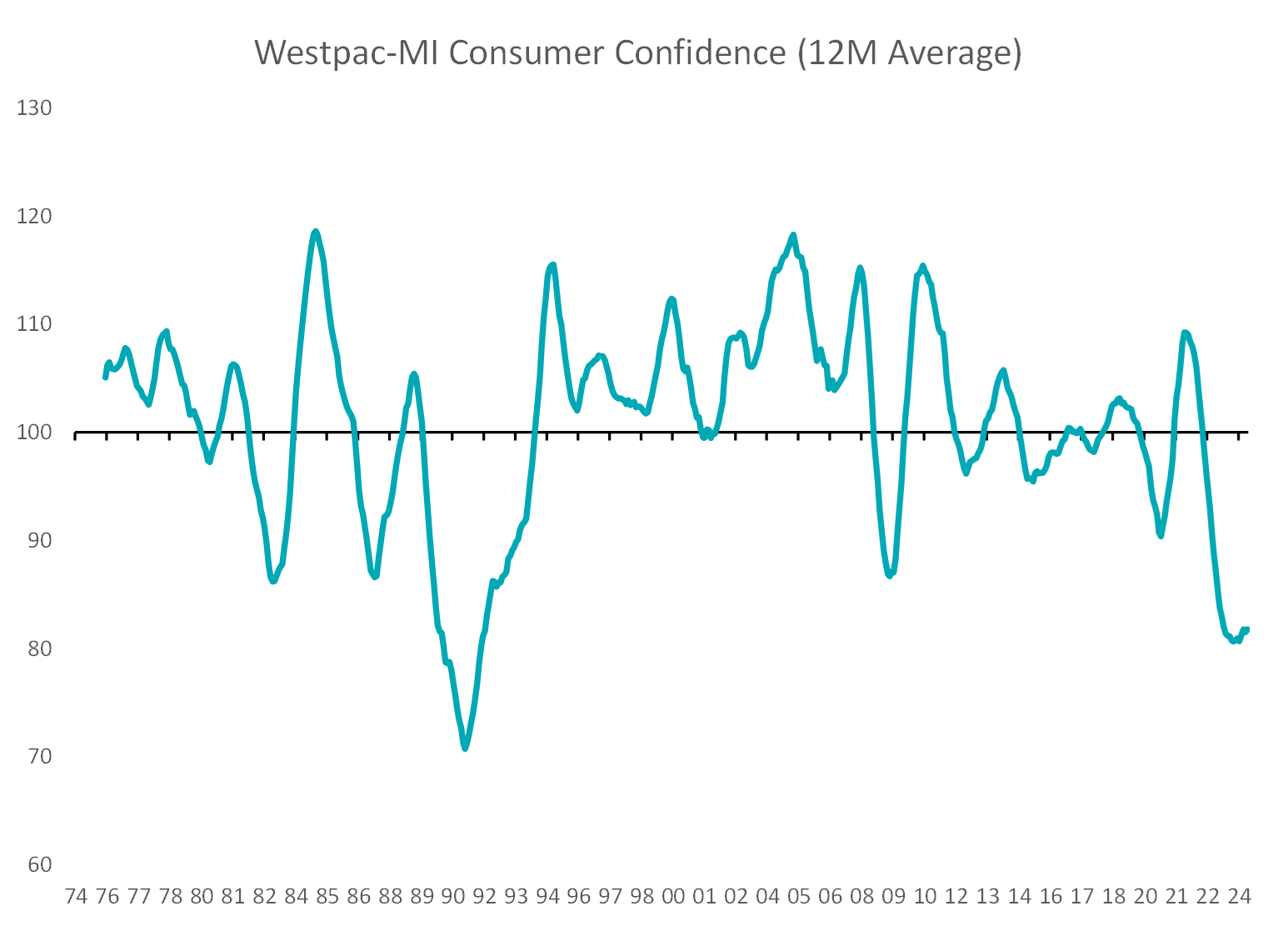

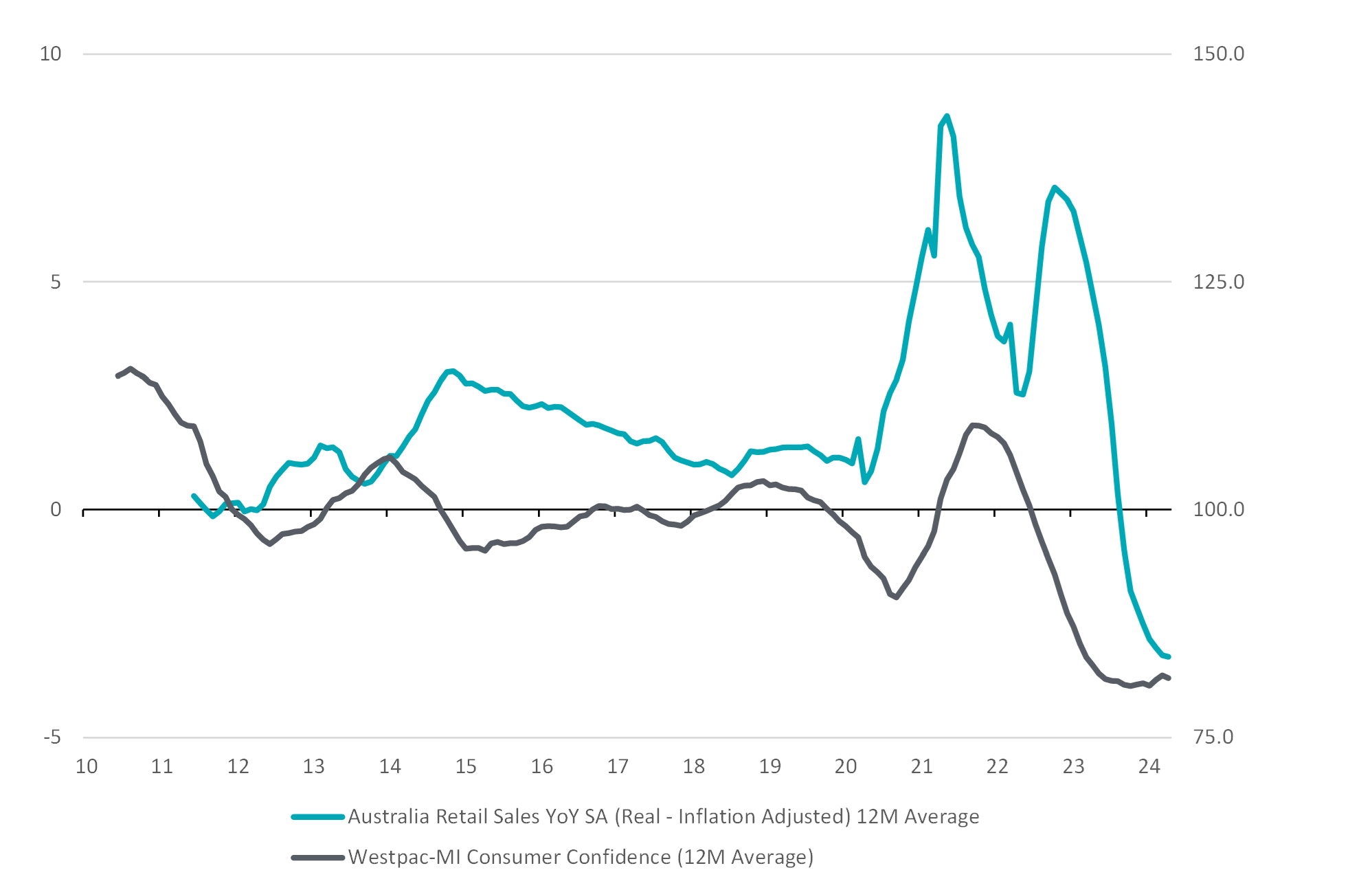

Over the past 10 years, the trends in Australian retail have been tough, with a brief period of respite in the immediate pandemic aftermath. Chronologically we have seen the emergence of ecommerce as a competing force (2010 onwards), growth in Australia of Amazon as a local competitor (2017 onwards), house price declines (2017-2020), COVID (2020 – 2022) and finally rapid interest rate increases (2022 – 2024). Throughout almost all this time, growth (both nominal and real) in retail sales (per Australian Bureau of Statistics) remained positive. This changed in early 2023 as real sales turned negative in February, and by September 2023 were negative on a 12-month rolling basis. They have only gotten worse since then.

Source: Australian Bureau of Statistics, Reserve Bank of Australia

Source: Australian Bureau of Statistics, Reserve Bank of Australia

Source: Australian Bureau of Statistics, Reserve Bank of Australia

Source: Australian Bureau of Statistics, Reserve Bank of Australia

Negative real retail sales growth is a big deal for retailers, as high fixed costs from rent and wages are likely to increase with inflation, putting significant pressure on margins. We have already seen a number of retailers lose profitability given weak sales and rising costs.

Source: Westpac – Melbourne Institute

Source: Westpac – Melbourne Institute

Source: Australian Bureau of Statistics, Reserve Bank of Australia, Westpac – Melbourne Institute

Source: Australian Bureau of Statistics, Reserve Bank of Australia, Westpac – Melbourne Institute

A decade of small cap retail stock returns

To better understand the base rates of success and failure investing in small cap retailers, we examined a broad selection of listed small cap retailers in Australia and New Zealand over the past decade. As a group of companies, the base rates of stock performance have not been good. The average small cap retailer has underperformed the Small Ords index by 8-10% per annum.

There have been multiple complete failures (Surfstitch, Pumpkin Patch, Sunbridge, Smiths City) as well as outcomes that differ from complete failure in form only (Booktopia, Oroton Group, Wellington Merchants, MarleySpoon, Mosaic Brands, AMA Group, Country Road) given shareholders lost 90% or more of their investment.

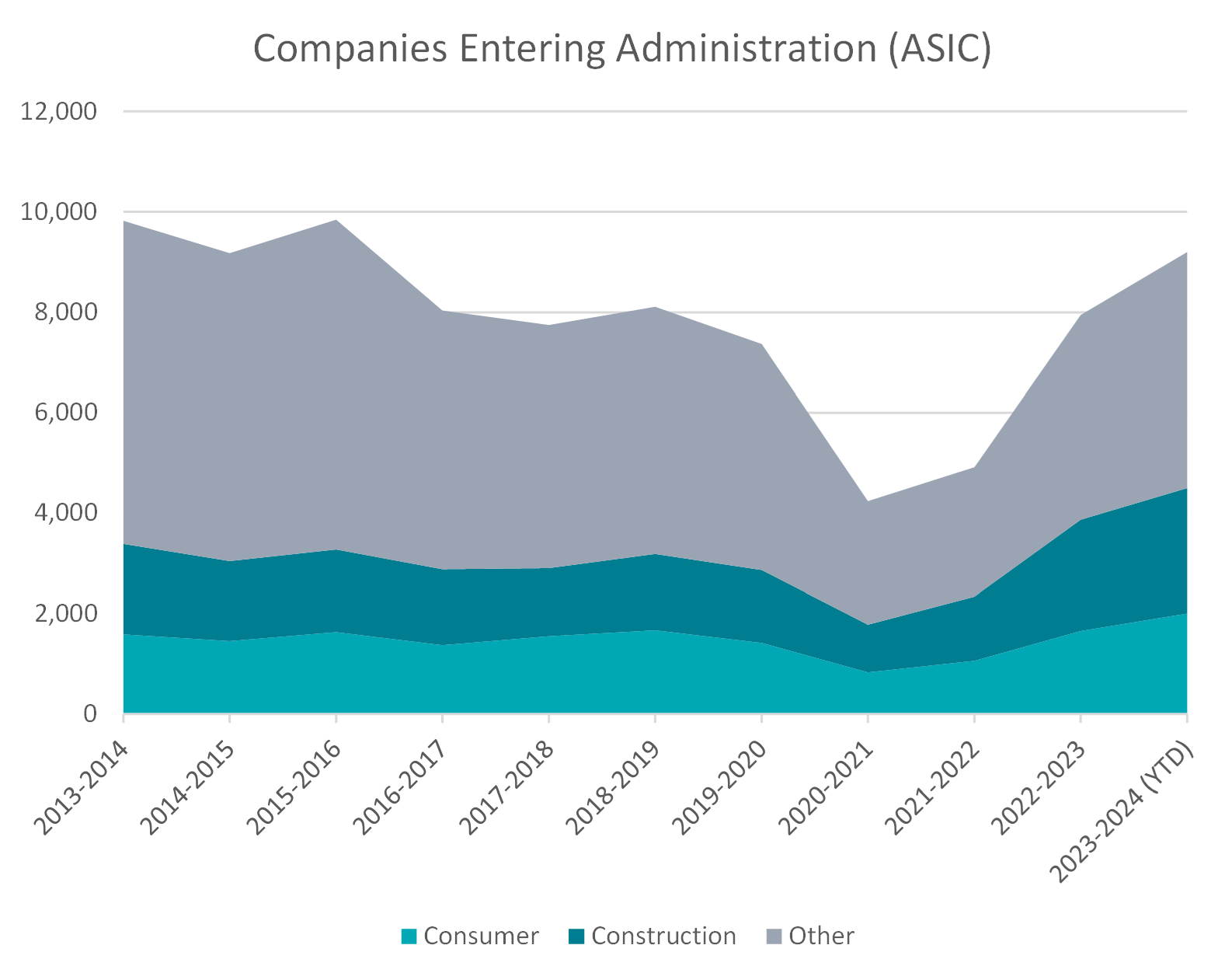

This probably underestimates the failure rate of the overall retail category. Listed companies are likely to have a selection bias toward better quality retailers. Consumer categories in ASIC insolvency statistics (Retail Trade, Accommodation and Food Services) often compete with the Construction sector for the highest levels of insolvency every year – and they are currently rising sharply, almost doubling from (unusually low) F2022 levels and we still have two months of the year to go.

Source: ASIC

Source: ASIC

There is a small group of high-quality small cap retailers who have survived and evolved despite brutal industry conditions. They tend to have management teams that understand the difficulties of winning in this market and what survival requires. They include companies such as JB Hifi, Harvey Norman, Premier Investments, Lovisa, Super Retail Group, Nick Scali, Reece, Accent Group and ironically Myer (!) given they are still around.

Emerging players currently doing well such as Temple & Webster, Cettire and Universal Stores probably need the test of more time to see if they can survive longer term.

Retail turnarounds

The greatest lessons markets teach investors come from mistakes. Over time, we aim to get better by learning from mistakes we have made (and hope never to repeat). Our investment process ensures this is more than just hope, as we code these painful lessons directly into our future decision making.

Unfortunately, there also seems to be an infinite number of new mistakes to learn from!

One of these may be the futility in turn-arounds in the small cap retail sector. Turn-arounds are hard enough, but retailers who have lost their position in the consumers’ minds (and wallets) can find it difficult, if not impossible to regain.

This can be observed in the comparable store sales growth – a.k.a same-store-sales (SSS) or like-for-like sales (LFL) of a retail business – either in absolute terms, or relative to the category. Ongoing negative relative comp store sales can more than wash away any hard-won turn-around gains made elsewhere in the business (product sourcing, gross margins, logistics, rent reviews, store rationalisation, productivity gains, new Point of Sale software, etc).

We have previously made a small number of investments premised on the ability of management to turn around an underperforming retail business – if not to former glory, then at least to something economically sustainable and reasonable. None of them went well and we no longer hold any retailers with this as the investment thesis.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.