Sometimes there's just not enough cake

“The art of manipulation is only successful when the manipulator remains undetected”

ESG Integration: The benefits of being on the tools

Longwave integrate ESG research and proxy voting responsibility into the day-to-day workflow of our team of analyst/PM’s. We’ve long believed that integrating ESG into normal analytical workflow can ensure that we bring a complete and wholistic view of ESG and financial elements to bear when working out what is likely to be of material risk. Integration also allows us to make better judgements on the appropriateness of remuneration structures when we’re voting (evidenced by how many more Remuneration reports we vote against than our proxy advisor). And finally it also allows us to spot patterns and anomalies in the data that others might not see.

Its this final point that led us to investigate the subject of this report. As we voted during the most recent AGM season, we noticed that it felt like time and time again we were voting against a remuneration report where the Chair of the Remuneration Committee happened to be female. This didn’t make a lot of sense to us as we also knew that the representation of females at Australian Council of Industry Super’s (ACSI) 30% target hadn’t been hit by every board we looked at. We also know that the number of Chairs who are female sits at 13.7% for the ASX300 [1], so we would have expected to potentially see something commensurate for committee chairs.

Voting decision making in practice

The thing that piqued our interest in this rather arcane subject though, was how the interplay of voting decision-making and board composition priorities can work. We have seen a few different decision making models when it comes to proxy voting across our careers and we are aware of how final decisions can be arrived at in both large and small managers. Sometimes, voting a particular way is not particularly black and white despite the best intentioned and detailed proxy voting guidelines. As with all things in life, its quite difficult to craft a policy (or process) that deals with every edge-case that can arise. This is why human judgement still has a role to play even in the most rigid of decision-trees.

Take (for example) a set of governance guidelines that both encourage best practice (strong alignment to shareholder outcomes) on remuneration but also sets a very strong target that all boards should have more than 30% of women on the board. These voting guidelines outline a cascading set of consequences for companies that don’t demonstrate improvement in their governance or movement towards targets that are considered to be best practice.

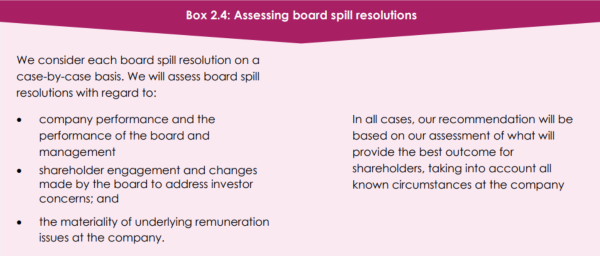

In the case of problematic pay practices, Australia has a well-accepted regulation of two-strikes (against Remuneration report) and board spill motion. But as we have written about in the past, we notice that shareholders rarely take advantage of the board-spill motion to convince boards that they’re serious about remuneration governance. ACSI outline their stance on assessing Board Spill resolutions as being on a case by case basis. The key elements in here (we think) are the statement that they’ll take into account the materiality of underlying remuneration issues (materiality generally being thought of as more than 10% of NPAT) and assessment of what will provide the best outcome for shareholders.

ACSI Governance Guidelines 2023

In the case of companies who are not meeting board diversity targets (which are moving from the old 30% to the new 40:40:20 target) ACSI outline a consideration of voting against at least one of the following (in descending order)[2]:

- the Chair of the board

- the Chair of the Nominations Committee

- a member of the Nominations Committee; or

- another director seeking re-election

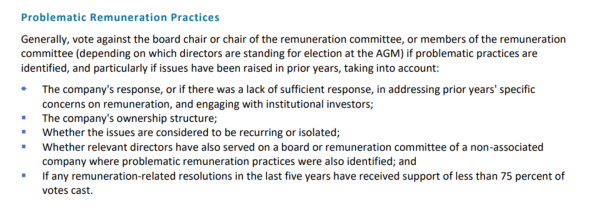

This framework for cascading consequences via voting against Committee chairs is a practice that is followed by proxy advisors and broadened to encompass board committees that oversee other parts of a governance framework. ISS for example states the following:

Source: ISS Australia Proxy Voting guidelines 2024

Now imagine a company that has consistently problematic pay practices, but also only just scrapes through on board diversity metrics. You vote against Remuneration reports across multiple years, but when presented with a Spill motion there is no collective shareholder coordination to stand up a full replacement board so its not in the best interests of shareholders to vote FOR the board spill. The only other options you have (absent engagement with the company to effect change) are to vote against the re-election of directors (Chair of board, Chair of Remuneration committee, other directors on Remuneration committee) or engage further and publicly.

In this case, there are two competing priorities at play. Which priority wins out and how should they be balanced? In our time in the market, we know that there are robust discussions around voting against the re-election of a female director in order to send a message about other problematic governance practices including Remuneration. Proxy advisors from time to time will also call out the balancing act (for example “shareholders may want to vote against the re-election of (Insert Director Name), but may also want to consider board gender diversity sits at 27%”).

So when we noticed (heuristically) that there were more female chairs of Remuneration committees than we would have expected, we wondered whether this is actually companies gaming the proxy voting system. Could companies be aware of the competing priorities and know that putting a female board member in as chair of the Remuneration committee at the margin will head off big Against votes for some director re-election ballots?

Our process – observe and check the data:

We think its very important to make the link between these heuristic observations and the actual data. To do this, we generated a complete dataset of the names of the Remuneration Committee Chairs for each company in the S&PASX Small Ords.

The results are interesting although not as stark as we initially expected (based on our heuristic sense).

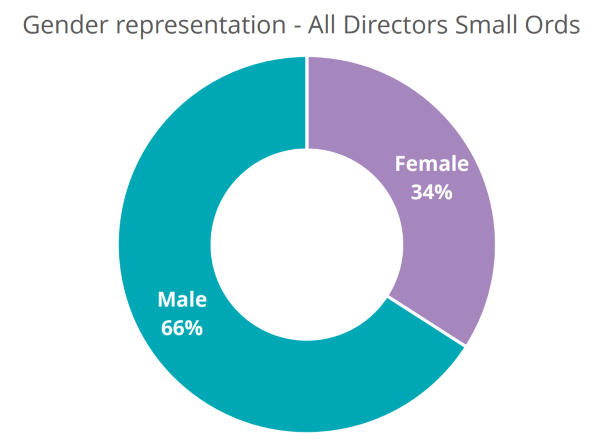

Lets look at the Small Ords first. At the index level, the average gender split across all boards is 34% female and 66% male. Boards have done a good job of increasing this representation from a starting point of 17% in 2016.

Source: Longwave, Citigroup data

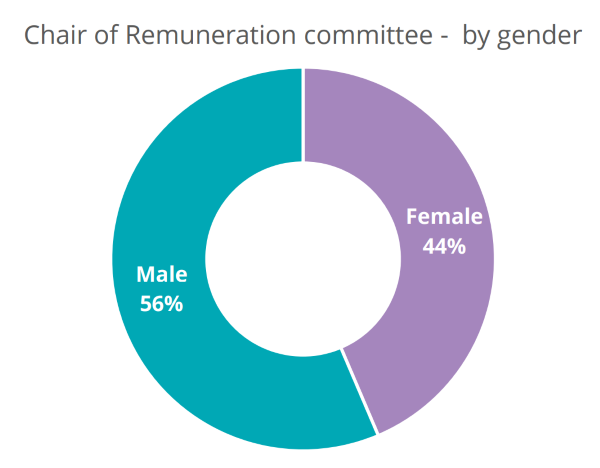

When we look at the Chairs of Remuneration committees however, the numbers are quite different. Women are over-represented proportionally by 10% compared to the whole board level. Now you could argue that this is a good thing. By giving women on boards committee chair positions, their total board earnings are boosted and they gain valuable experience of chair roles. Arguably this could be preparing them for future Chair of board roles. Although we’d note that the progress on female chair’s has been relatively glacial.

Source: Longwave

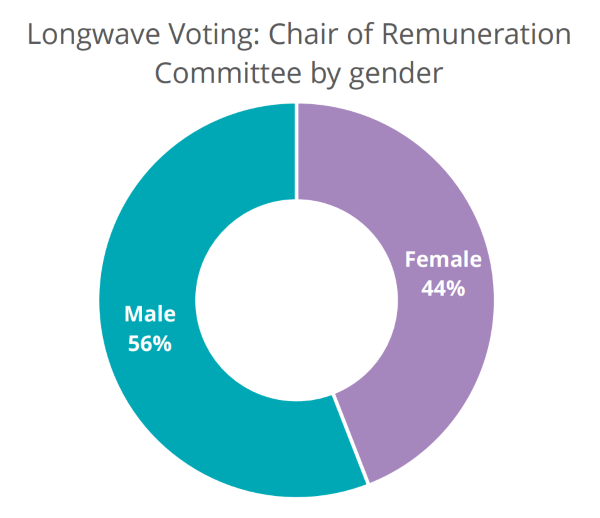

Now let us turn to the Longwave voting across renumeration related resolutions. In 2024, we voted on a total of 258 Remuneration related resolutions. These include approving a Remuneration Report, approving issuance of performance rights to specific executives (or board members) and approving the renewal of performance right plans.

The representation of male vs female Chair of Rem committees across our entire universe of remuneration resolutions mirrors what we can see in the ASX Small Ords:

Source: Longwave

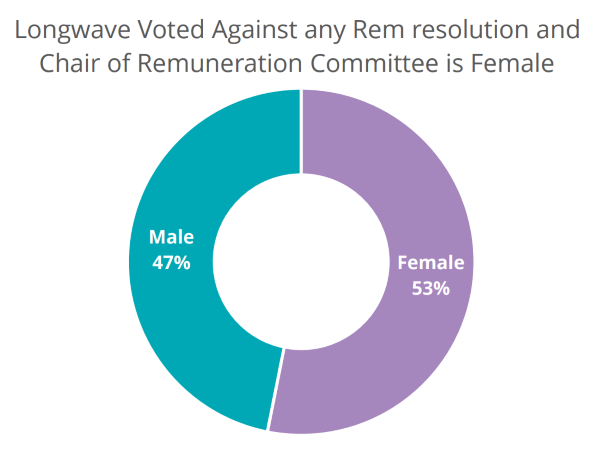

What’s interesting to us is what happens when we look at where we are voting against remuneration resolutions. The gender representation of the Chair of the Rem committee flips around from mirroring the ASX Small Ords Chair of Remuneration Committee to being 9% over-represented again.

But why is this important? Let’s return to our earlier fleshing out of the tools investors are given to convince boards that they are serious about good governance. If boards are aware of the competing governance outcomes that investors are attempting to solve for and also aware of how the decision trees are worked through and weighted, could it be possible that appointing a woman to the Chair of Remuneration committee is a first line of defence against any kind of public reprobation like a big against vote for a director?

Related to this, how many boards have avoided these signals in the past because of the competing governance priorities that are being solved for?

Source: Longwave

We want to stress that we are not accusing any specific companies deliberately giving investors a set of double-bind decisions, only shining a light on disparities we’ve observed. We understand that most company management and boards are largely trying to do the right thing and achieve a balance and outcomes that meet a complex and ever-evolving set of shareholder priorities.

Our final observation would be the gender split amongst the Remuneration Committee Chairs for companies that have problematic pay practices that progress to a board spill motion. Here the numbers we’ve highlighted below make a dramatic reversal. During 2024, Longwave was presented with 13 board spill motions to vote on. A board spill motion tends to happen when boards have been slow to recognise and align pay practices to shareholder expectations. Of these 13 companies that progressed to a board spill motion, 62% of the Remuneration Committees were chaired by men and 38% were chaired by women. We will leave readers to draw their own conclusions on what this may signal.

The great ESG cooling – sometimes there’s just not enough cake

We would be remiss in this bi-annual report if we were not to mention the seismic cooling in both the rhetoric, support for ESG initiatives and reporting requirements across the globe that are likely to impact the way the investment community continues with its ESG efforts.

The combination of legal action both here (greenwashing accusations) as well as in the USA (prioritizing climate change over fiduciary duty) we think will impact how large investors view ESG data transparency on their products. More transparency tends to invoke more scrutiny and more work to justify every decision that required a trade-off between a good ESG-related outcome and a good investment or shareholder-related outcome. We hear this often from boards and management teams in private conversations. They want to do the right thing, but often feel like they are presented with a wish-list of outcomes that deny the real-world trade-offs that are at play every day in every facet of running business enterprises.

With the election of Trump, the sharp roll-back of US government backed programs and the fact that the new climate has now given many business leaders permission to express their long-held private views, we detect that companies are likely to re-prioritize their efforts somewhat over the coming years.

As ever, being on the tools across both investing and ESG elements in our process will be an advantage and we look forward to dealing with this ever changing environment.

Voting Observations

In the year to 31st December 2024 we cast 654 ballots for 124 company AGM’s. Of those, 17% were AGAINST votes, but this hides the fact that we voted against at least one resolution in 41% of the AGM’s we voted on.

Many of these AGAINST votes (again) related to Remuneration practices (both Remuneration reports and Equity issuance to executives or board members).

[1] https://www.aicd.com.au/news-media/media-releases/2024/number-of-women-directors-climbing-but-not-women-chairs.html

[2] https://acsi.org.au/wp-content/uploads/2023/05/ACSI-Voting-Policy-%E2%80%93-Gender-Diversity-in-the-ASX300.May23.pdf

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.