Longwave christmas gift 2023

– Melinda White, December 2023

In 1977, my grandfather Barry celebrated my birthday by buying a parcel of shares in my name. It was a small parcel of shares in Adelaide Brighton. Every birthday and Christmas after that, my grandmother would give me $25 to buy something “nice” and Barry would gruffly declare that his present was $100 towards the share portfolio.

Even at a very young age, I had a sense that this was unusual. Other people’s grandfathers gave them things. Barry (a country doctor, lover of lawn bowls, player of the church organ and a mean jazz pianist), gave me a promise for the future. Something I could neither touch, nor feel, but that gave me so much more than the “nice things” I’m sure I bought but can no longer remember.

Barry had one very simple idea at the genesis of the grand-children’s portfolios. All he wanted to do was to hand us each a parcel of stocks at our 18th birthday that would be enough for a deposit on a house or to buy a car. But over time, as he slowly started to introduce chat about the shares into pre-golf breakfast-table conversations, they became much more.

Alas, for me, Barry was not the world’s greatest investor. My 3 stock portfolio did passably well, but at 18, was not enough for a house deposit in Sydney and I was in no need of a car. It did, however, make all the difference when I interviewed for my first job as a junior office assistant with a fund manager at 19 (I knew what a stock code was and what the stock market was for). And it taught me a number of life lessons I am deeply indebted to Barry for.

In the years before my first job, I viscerally learnt the value of delayed gratification, saving and patience. Investing is a long-term game. There is no such thing as getting rich quickly. Or more precisely, the shorter your investment horizon, the higher the probability that you will lose rather than win.

At 15, I learnt the difference between working for a wage and saving to invest to earn dividend income. I still have his tiny doctor’s prescription papers with his (typically illegible) doctors scribble on it, spelling out my dividend income for the year. Imagine comparing your $3.65 per hour wage earning potential to a $300 dividend.

At 18, when I was handed the shares and my grandmother tearfully and forcefully instructed me to never sign them over to a man, I learnt the freedom of ownership. Her father had instructed her similarly in 1947 when she married to never give Barry her Southcorp shares. On her death, she still had the original bearer certificates stored away in a safe. For her they had always represented independence. During the golden age of the 1950’s housewife, she had had the freedom to leave or to provide for children if domestic violence or misfortune overtook her married and dependent life.

This year, we’ve decided to carry on Barry’s tradition. We’d like to give you – our clients – a gift to give your children, nephews, nieces or grandchildren. Each year, at Christmas, we will write about one stock in our portfolio that we feel would have a place in a portfolio for your grandchild. What we think of as a 20-year stock. A business you can buy today that has a high probability of being a valuable contributor to a portfolio over the next 20 years.

Our vision is to help you pass on the life lessons that we have learnt from working and investing in capital markets to the next generation. To this end, we will endeavor over the years to both talk to our investing framework and to give you stocks from a variety of industries and sectors. Some your special young people can identify with (there’s nothing like knowing you own a miniscule share of Smiggle to understand the power of capitalism). And others that are just good businesses that should compound over a long time-frame.

20-year stock framework

We have talked a lot this year about the types of companies in small caps our process is designed to identify and keep us invested in. Our process recognizes that small caps are different to large cap businesses for a number of different reasons: very early in their life they are more fragile, more prone to failure during external economic shock or if the competitive landscape suddenly changes. As a result of recognizing this fragility, our definition of what quality looks like in small caps is different to what you might look for in a quality mega-cap.

But small-cap businesses are also where you find the exciting, high growth businesses. The new technologies and innovation that play a part in driving human evolution forward. The challenge of investing in small caps is to balance the desire to be part of everything new and exciting against the risk of losing your equity capital all-together.

When selecting a 20-year stock, we are looking for a couple of key characteristics:

- The business needs to have exited its highest probability of failure phase and entered what we think of as the “sweet spot” its lifecycle. This is its highest growth period where the business has not only proven it has a product it can sell for real revenue, but has also reached a point where the profit from that product is observable to shareholders,

- It needs to have a long runway for either growth in earnings or capital value,

- It needs to have a balance sheet and capital discipline that leave us confident that growth in earnings at the aggregate will result in earnings per share growth.

Nanosonics

This year, we have selected Nanosonics as our inaugural 20-year stock. Nanosonics is a global business founded in Australia in 2001 and listed on the ASX in 2007. It’s core product is an ultrasound probe disinfection device that reduces the rate of what is called “cross-patient contamination” in clinical settings where ultrasound probes are used for ‘internal’ examinations. Most of us who have visited a clinic for an internal ultrasound examination have probably never thought about where the device has been before. We have a high level of trust that the device is clean and we won’t pick up an infection from the visit. The current wide-spread standard of care involves a human dismantling parts of the device and manually cleaning and drying it by following a minimum 16-step cleaning and drying process. This is highly prone to human error and omission and can result in bacterial deposits remaining on the probe.

The Nanosonics Trophon device is an automated solution to this error-prone human cleaning process. The operator simply places the entire ultrasound probe into a cabinet that delivers a patented sonically activated disinfection mist that is designed to comprehensively kill bacteria and viruses that lurk on easy and hard to get to parts of the device.

Source: Nanosonics

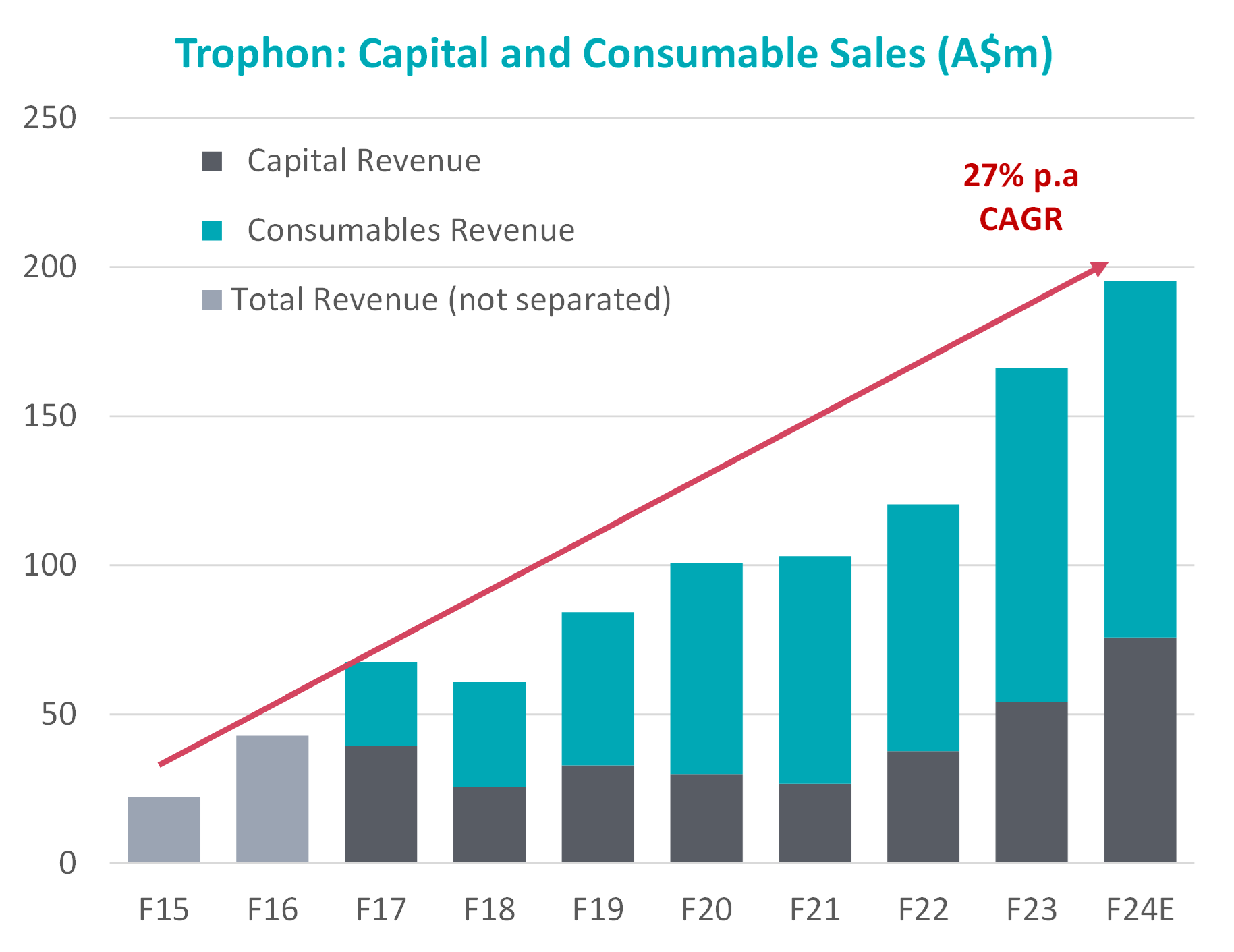

Nanosonics sell this device into hospitals and radiology clinics where ultrasound probes are used. The Trophon unit has a large dollar-cost attached to it, but every year, Nanosonics will also sell the clinic consumables to go with the device.

What this means is that as the installed base of devices grows globally, so too does the annual recurring revenue potential of the business. These razor and razor-blade business models are often very beneficial for shareholders. The margins on the consumables are often very high and the cost of the sales force fixed. Over long periods of time this results in growing EBIT margins as the business gets bigger.

Over the last decade, Nanosonics has grown its revenue from $14m to $166m, or 25% per annum. It became a profitable business (able to self-fund its growth) in 2016 and has continued to be profitable, despite re-investing a considerable amount into R&D to develop an adjacent product in the clinical disinfection market. In its core Trophon market, we estimate that it is only 25% penetrated globally so it still has a long runway for growth in earnings.

Source: Longwave Capital Partners

The new product Nanosonics has been working on has recently been unveiled. Its called CORIS and is designed specifically for cleaning endoscopes between patient use. Nanosonic estimates this market could be just as big as the market for Trophon. This year, the management team of Nanosonics also revealed for the first time that the Trophon business stand-alone made $33m of after-tax income. This is significant, as we can now value that part of the business standalone and view the CORIS technology as future option value

Despite all this re-investment into growing the business, Nanosonics has a rock-solid balance sheet. Its cash balance has grown over the years to $122m and there is no debt on the balance sheet. Some may call this lazy, but it does result in us having confidence that future growth in after-tax profit will go to current shareholders, not debt holders or new equity holders.

If you buy the stock around the current price of $4.40, we think you get a core Trophon business that will continue to grow its revenue between 15 – 20% per annum and its earnings potentially faster. Not only that, you get the option-value of the CORIS business for nothing and because of the balance sheet strength, you can have high confidence that that earnings growth will come back to you as a shareholder.

Whilst Barry taught me many things about investing in equities and over the long term, he probably didn’t appreciate the benefits of portfolio diversification in small caps that we see at Longwave. I would hope, however, that he would have seen the compounding potential and quality of a business like Nanosonics and agreed to include it in a 20-year portfolio.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.