Long and variable lags coming home to roost

“The term “long and variable lags,” initially coined by economist Milton Friedman, has appeared prominently in the way that central bankers talk about the impact of monetary policy. It can take changes in interest rates some time to affect the macroeconomy (the lag is long), and that time can differ unpredictably across episodes (the lag is variable).”

Bill Dupor – Federal Reserve Bank of St. Louis

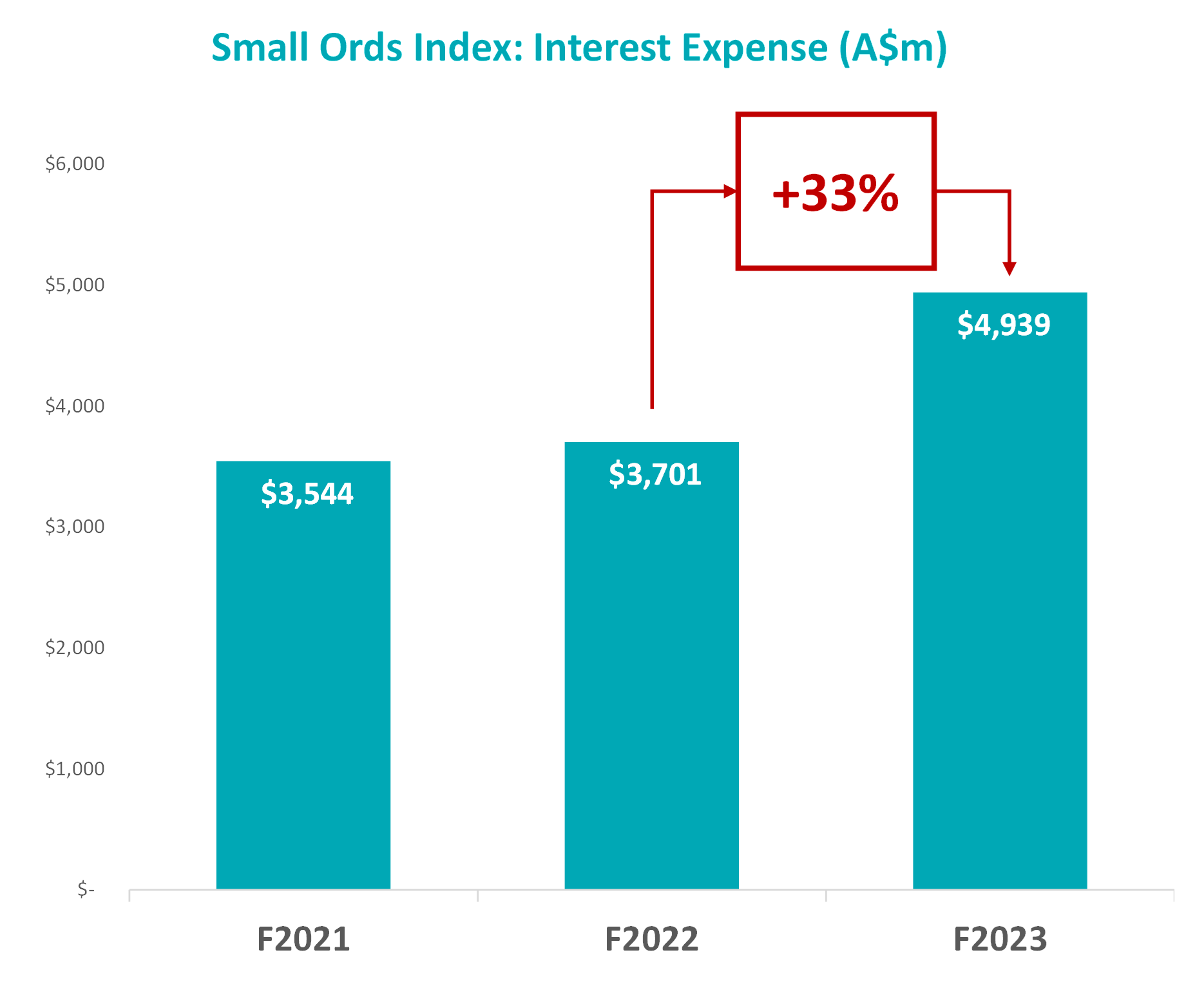

For the past two years, the market firmly focused on the residential mortgage refinance cliff, as low-rate fixed home loans from 2020 and 2021 rolled off to higher variable rates. Attention was distracted from the same phenomena taking place across corporate Australia. With average corporate loans fixed for around three years, the early lack of higher interest rates impacting corporate earnings was reassuring, until debts started maturing this year. The pain of higher rates has only just begun.

Source: Longwave Capital Partners, Bloomberg. 31 Oct 2023.

Some examples of what this looks like in small caps include:

- Star Entertainment: started the year trading at around A$1.70 with 952m shares on issue, carrying around A$1.3bn in debt. Raised A$800m in February at A$1.20 to pay down debt. Still had A$750m of debt by June 2023 and raised another A$750m at A$0.60 in September to retire this debt. Stock last traded at A$0.54 (down 68% YTD) with 1.55bn shares on issue.

- AMA Group: started the year trading at A$0.18 with 1.07bn shares on issue, carrying A$210m in debt. Raised A$55m at A$0.075 per share. Stock last traded at A$0.057 (down 68% YTD) with 1.77bn shares on issue.

- Judo Capital: Net interest margins boosted by cheap finance from the RBA emergency Term Funding Facility (3 years fixed at between 0.10%p.a and 0.25%p.a) – now rolling onto higher funding cost. Issued a Capital Note in October priced at BBSW (last 4.35%) plus 650bps implying cost of 10.85% (!). Judo have other sources of funding, but when lending to SMEs at BBSW + 450bps the risk equation here is upside down (stock down 24% YTD).

- Credit Corp: purchasing delinquent debt in the US market and finding consumer patterns around repayment plans are falling below expectations. Higher interest rates are forcing consumers to prioritise other needs and Credit Corp is a casualty here (stock down 35% YTD).

You can bet there are property and lending businesses in peril from higher rates, but there are also healthcare, software, transport, gaming, communications, commercial services, building materials, mining, chemical and retail businesses in the same position. We won’t name these companies for obvious reasons, however investors only need to look at readily available information, such as the reported financials from the last results, and management guidance for the current year (and heavily discount claims of a “robust balance sheet” from management) to form a view on just how prepared a business is for higher interest rates, less forgiving lenders and any potential operating weakness.

If you are observant, you can see the market “sniff out” stocks that carry too much debt. You can almost feel the desperation of the Chief Financial Officers, hoping for a bit of a rally in their share price and a few weeks’ respite in the bond market to open the raising window and make the much-needed equity issuance a bit less painful.

If your debt to market cap is say 50%, and you want to cut your debt in half, you are looking at a 1 for 4 equity raising. In fact, if debt to market cap is already at these levels, you will probably be offering a steep discount to entice shareholder participation, and the dilution will be even greater. At the end of the day, survival is more important than dilution and equity recapitalisations (recaps) that need to happen will – even if shareholders are not thrilled by the cost and dilution.

We will undoubtedly have some of these events in our portfolio (we already have with Credit Corp). As much as we try and understand and avoid – or at least control – the risk from excessive levels of debt, experience tells us we will be unpleasantly surprised. If we believe in the quality of business and the capability of management we are likely to be part of an equity recap solution. Experience also tells us that sometimes, despite attractive discounts, we may have made a mistake on the investment thesis. We can fall into a behavioural trap by throwing good money after bad – and the right thing to do is exit the position. Another option is to participate in the recap for a business we don’t currently own. If the only thing we didn’t like about a prospective investment is the balance sheet leverage, and we can participate in removing that risk, we will consider it. There is no one answer here – each potential opportunity is assessed on its own merit.

One lasting lesson we took away from the GFC is that survival and growth are not modes of operation a company (or a human) can pursue simultaneously. Over the medium to long term, companies fighting for survival get overtaken in their markets by companies not distracted and who can focus on growth, execution and winning.

Markets are still early in the debt reduction cycle

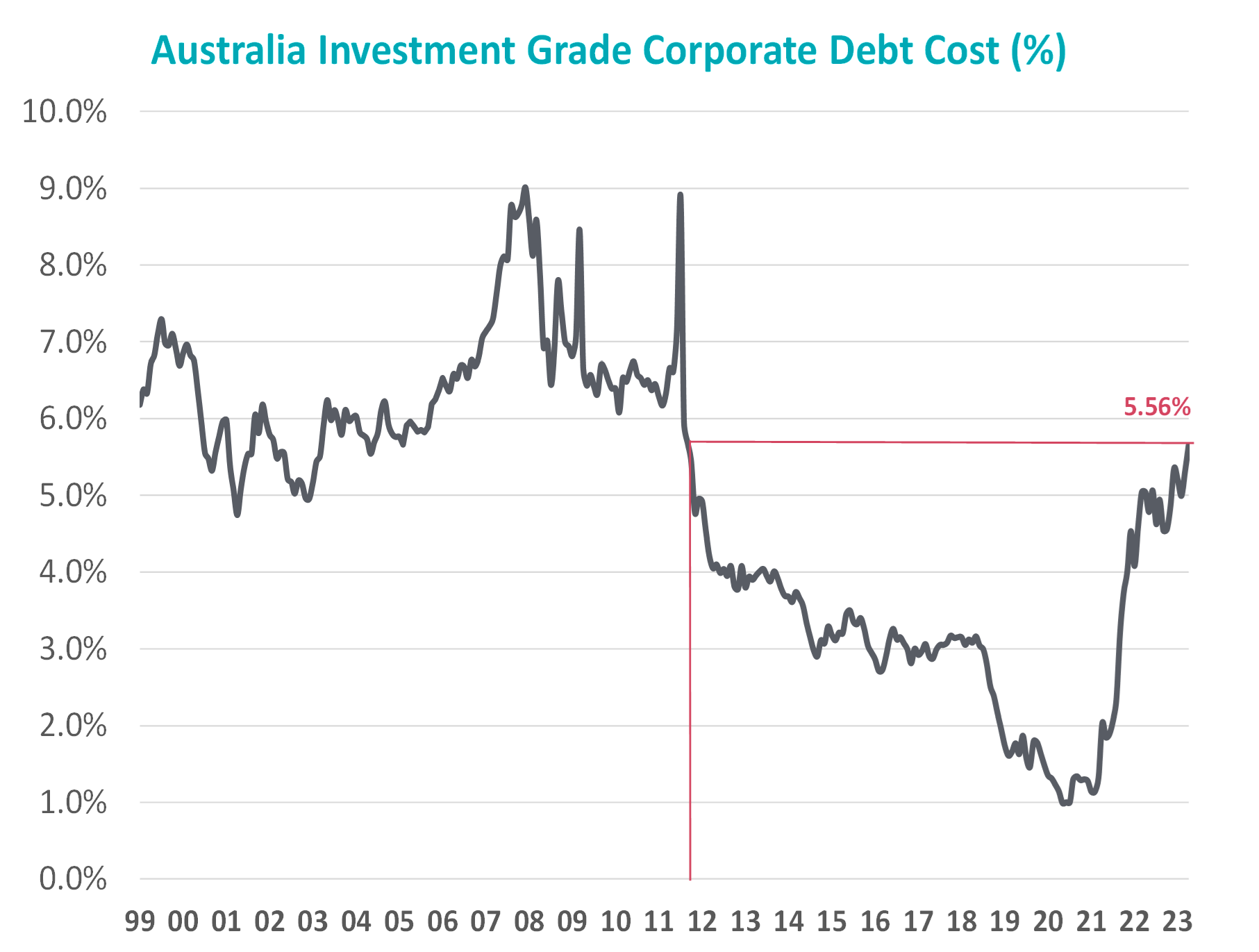

When thinking in late 2023 about the feed through of higher rates into the issues described above, the Longwave team are reminded of the premature calls of transitory inflation in late 2021. As a reminder, commodity prices were still racing higher, and the lags meant what we were seeing in real time commodity prices was months and quarters away from feeding into inflation data. It seemed crazy in the face of this to believe inflation had peaked, and our discussions with corporate executives confirmed as much at the time. US 10-year government bonds ended 2021 at 1.5% – there was no concern about inflation being anything but transitory. Today, government bond yields are still going up. Market measures of corporate debt cost are still going up. Whatever rate a company can refinance their debts at today is almost guaranteed to be more than it was three months ago, or six months ago or pretty much anytime since early 2012.

Source: Longwave Capital Partners, Bloomberg. 31 Oct 2023.

A decade of excess leverage must be resolved and as much as investors want the pain to end, on this front, we fear more pain for the over-levered is still to come.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.