Forecasting errors in exponential technologies

In 1960, the IBM 305 RAMAC was a 5MB hard disk which weighed 907kg and was the size of two large refrigerators. Today 400,000 times this storage capacity fits in a 2TB SD Card the size of a postage stamp weighing 2 grams. The impact on the physical world (size and weight) of exponential changes in technology are intuitively difficult to grasp.

Let’s say that in the 1960’s, this wonder of digital storage sparked the wonderful idea of digitizing the entire U.S Library of Congress collection, which at the time was about 80 Terabytes in digital equivalent size. We would need to spend US$800 billion on 16 million IBM 305 RAMAC’s, which would weigh about 14.5 million metric tonnes and require 144 million square metres of space. The power required to run these drives would consume around 84% of the total power produced in the U.S in 1960.

Of course, none of this came to pass, and the exponential improvements in storage technology mean you can go to Officeworks today and get 80TB of storage for a couple of thousand dollars and host the U.S Library of Congress from 1960 (which has since more than doubled by 2024) under your desk at home.

When at Schroders, we used to joke about the analyst “Phil Wright” – a phonetic pun on the forecasting method of just using the last few years of observations and hitting “fill right” in excel to populate forecasts of what the future would look like. No thinking required. Today, the world is relying on Phil to calculate how many dollars will be spent for how much Artificial Intelligence compute, housed in how many data centres consuming how much power over the next 10 years. AI is a technology about as early in its lifecycle today as digital storage technology was in 1960. We have no idea how this technology will change in the next decade. We would bet many of the infrastructure investments currently being made rest upon incorrect assumptions, as progression in the underlying technologies proves to be exponential and not linear.

We discussed data centres in April, and the obsolescence risk here from the changing infrastructure needs of AI vs general cloud compute is already showing up. Unlike infrastructure built for people and their goods (houses, offices, roads, airports, warehouses, power stations), infrastructure built for technology is much riskier. Probably why many operators who know these assets intimately are currently rushing to sell into a very optimistic market of financial buyers.

Even the most recent technology revolution, the commercialization of the Internet and the massive telecom infrastructure investment that accompanied it 25 years ago played out very differently to what was expected at the time (as evidenced by the number of companies that failed completely when that bubble burst). It did setup the world for a real digital revolution – branded at the time Web 2.0 – and serves as a reminder why being early is not as important as being right.

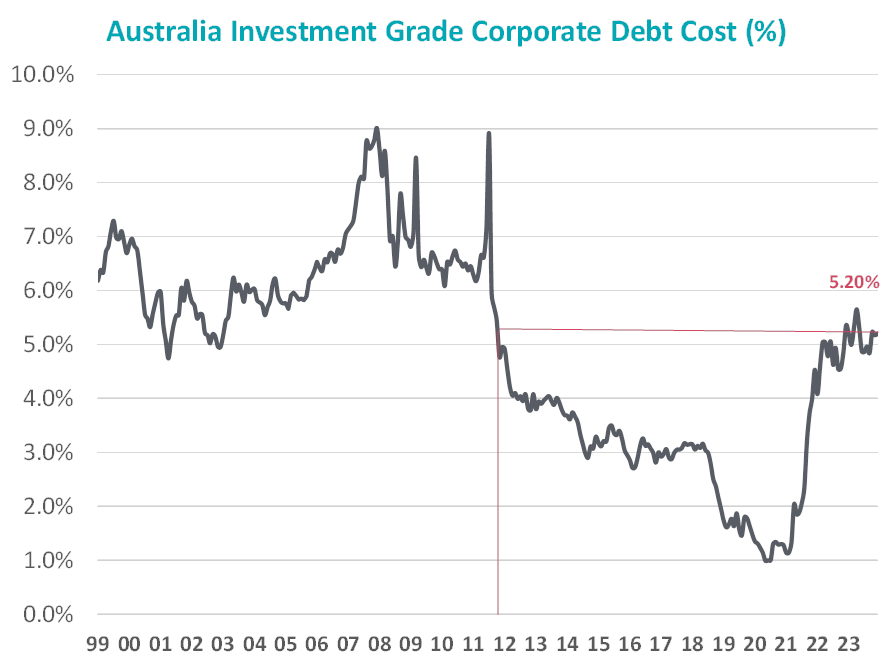

About those AUSTRALIAN interest rate cuts….

Back in the real world, things remain tough. Ongoing evidence of consumer weakness in company trading updates weighs on company profits. Australian inflation stickiness is putting upward pressure on interest rates – an additional pain neither the consumer nor many corporates can easily tolerate. Having been removed from the list of things investors needed to worry about for most of this year, the prospect of needing to raise equity to shore up over-levered balance sheets is coming back into focus for many small companies and their shareholders.

Source: Bloomberg

Source: Bloomberg

The City Chic (CCX) asset sale and capital raising during the month was an example of this. As we discussed last month, we think more of these will need to happen in the next six months.

There are some bright spots – Bapcor (BAP) received a takeover approach, consumer gaming companies Tabcorp (TAH), Light & Wonder (LNW), and Jumbo Interactive (JIN) appear to be doing better. McMillian Shakespeare (MMS) and SmartGroup (SIQ) are benefiting from the improved vehicle supply and ongoing EV adoption, although this is coming at the long overdue expense to auto retailing margins at Eagers Automotive and Peter Warren.

The latest speculative bubble in the Aussie small cap market to show the all-too-familiar signs of coming back to earth is Uranium. Paladin (PDN), Deep Yellow (DYL), Boss Energy (BOE) and Bannerman (BMN) have seen one way traffic – with share prices all up 120-150% since the end of 2022. The story has been compelling, as prices reflect the hopes and dreams of a nuclear future. Like the lithium bubble most recently before it, the reality of mine commissioning, insider selling, capital raisings and the more mundane commodity considerations of supply and demand have weighed on prices in June. The uranium spot price has pulled back 20% from the most recent peak, and the stocks are all down 15-20% in June. Paladin is no longer a small cap, having been promoted to the big leagues of the ASX 100 during the month and large cap managers are likely to be the ones dealing with the harsher reality of production at Langer Heinrich as they did for Liontown (down 66% since ASX100 inclusion late 2023 and now kicked back down to the Small Ords) and Arcadium (formed as part of a merger between Allkem and Livent in late 2023 and also down 50-60% since).

The expected infinite need for power to feed the millions of IBM 305 RAMACs, sorry Nvidia GPUs, will likely keep nuclear power as a hope for years to come. Much like lithium mine investments, made to profit from the inevitable transition from ICE to EVs, investors may discover the returns from uranium mining stocks and AI infrastructure a bit more elusive.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.