1H F2024 reporting season

Reporting season was mixed for the portfolio. Some wonderful companies continued to deliver over and above market expectations. At the other end, companies we think have the potential to be doing a lot better are either kicking own-goals or the execution of business improvement is more challenging than we thought. The overall scorecard is par relative to the index.

In a little over 12 months, Small Resources have underperformed Small Industrials by almost 30%. Some of this is the implosion of speculative lithium stocks, but there are difficult issues for small producers including but not limited to mine failure, production problems, cost inflation and of course weak commodity prices. All the reasons why many investors avoid the sector. We continue to look for quality businesses within resources – 2022 highlighted the benefits to total portfolio returns of this broad diversification – however the past 12 months remind us why this can be a difficult sector in which to remain invested through the cycle.

The importance of management

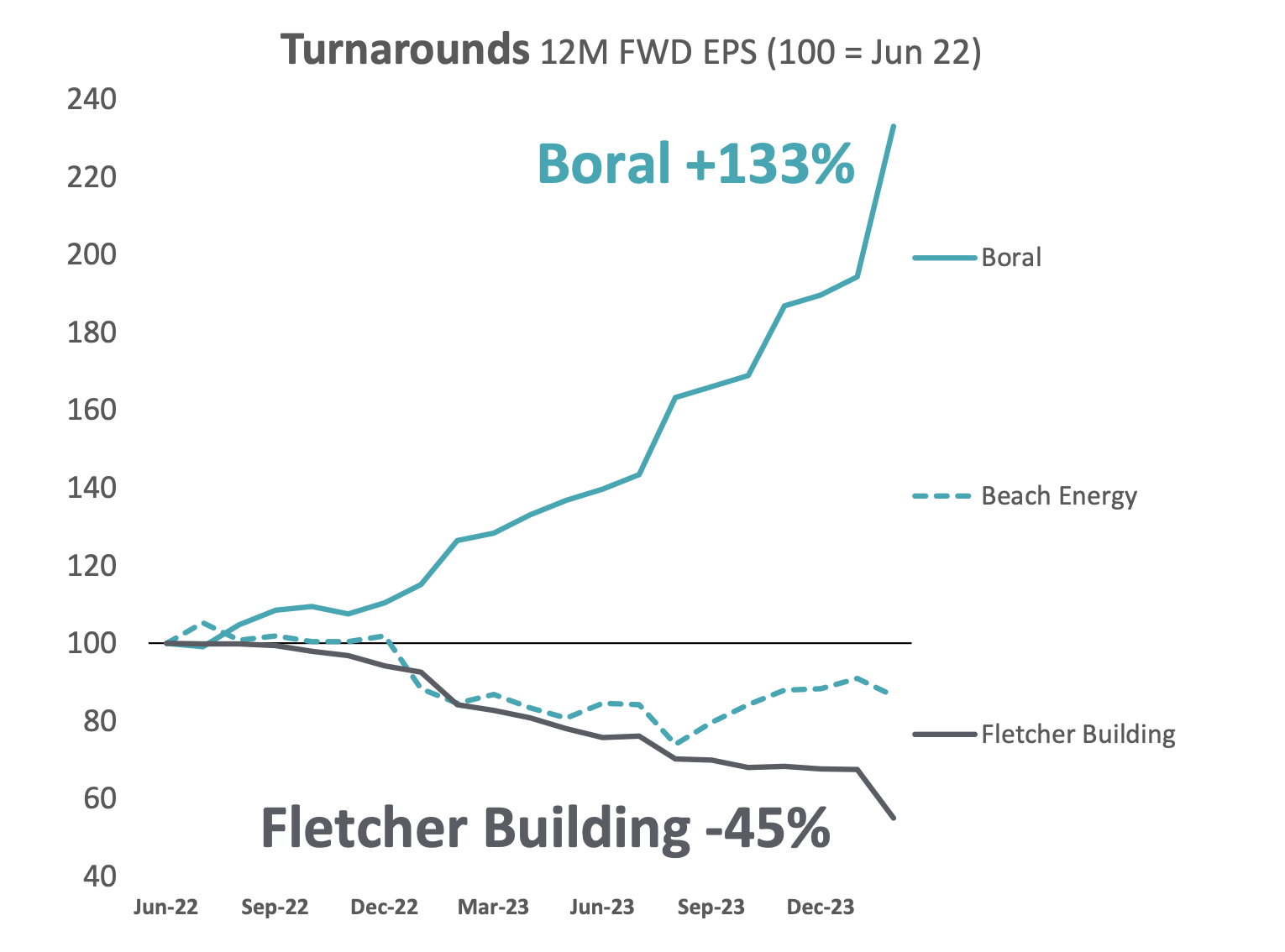

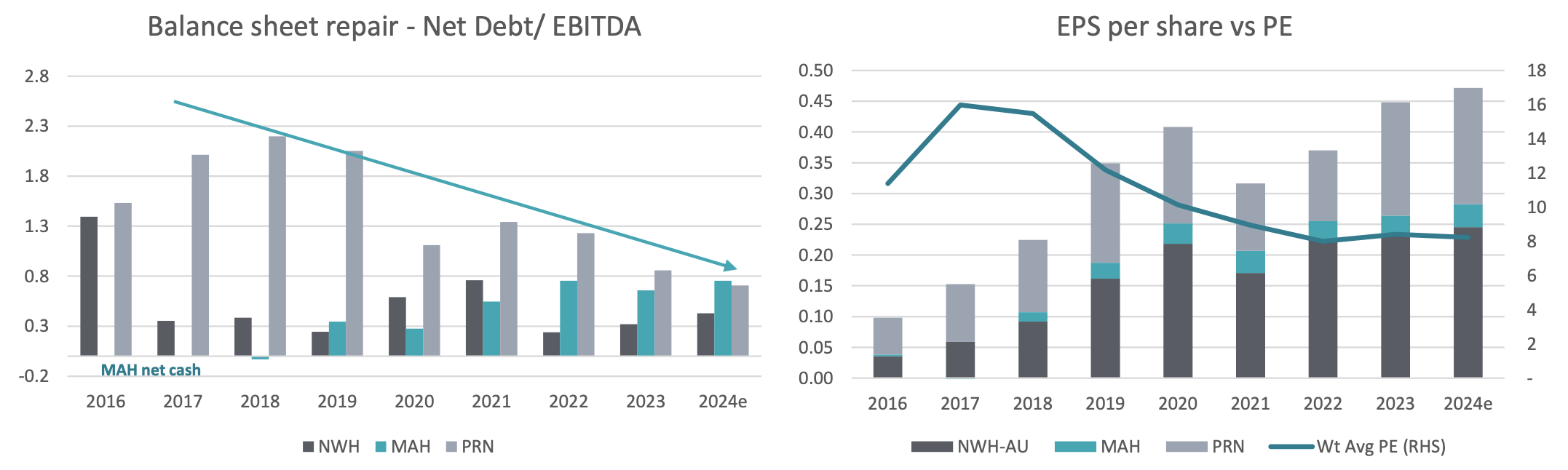

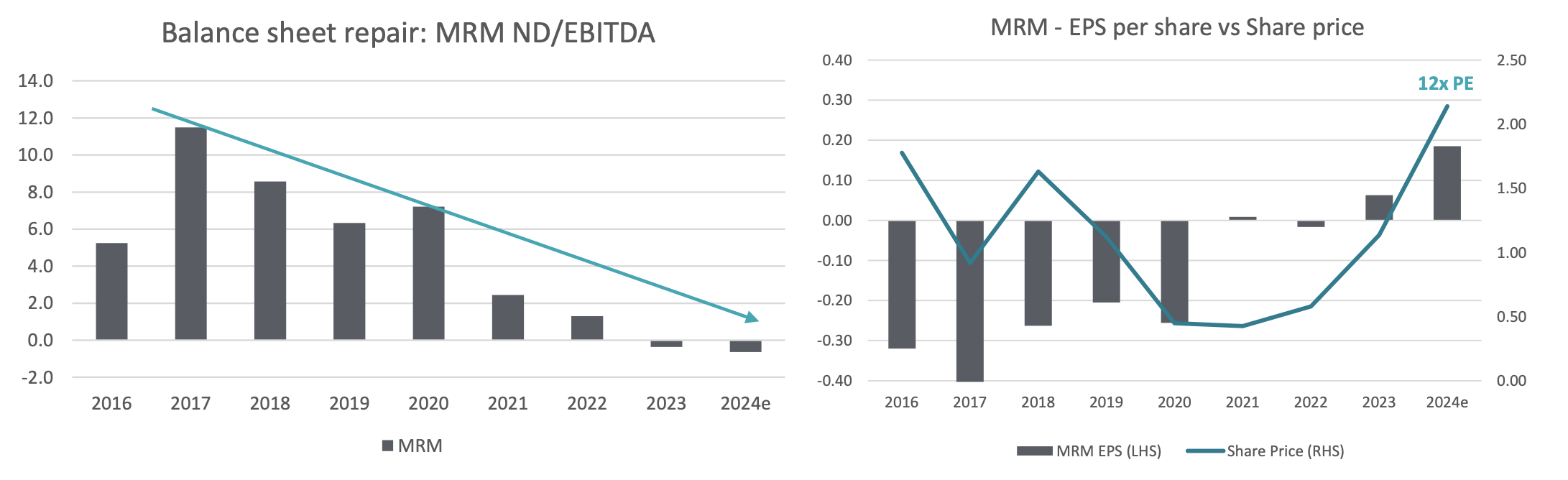

Sharing a strategic shareholder (Seven Group) has us looking at the new CEOs appointed to long-term under-performers Boral and Beach Energy with a different lens. In the less than two years since Vik Bansal joined Boral, the abrupt uptick in operational performance and share price (particularly against their languishing peers Fletcher Building and Adbri) is stark. Seven Group clearly agree as they announced a bid for the minority interest they do not own shortly after the results were released.

It wasn’t lost on us that incoming Beach Energy CEO Brett Woods shares some similar characteristics. A technically proficient operator from Santos with a focus on structural efficiency improvements and improving returns through self-help. Boral had underperformed the market for six years prior to Bansal’s appointment, Beach Energy for four years before Woods. They are different businesses each with unique challenges, but we are guessing effective management is likely to be a common denominator at both.

Source: Longwave Capital Partners, Bloomberg Consensus Estimates

Source: Longwave Capital Partners, Bloomberg Consensus Estimates

Fletcher Building could hardly have had a less effective management team or board over the past few years, and Boral in particular shows investors the opportunity cost of having market leading assets (as we still believe Fletcher does in NZ), poorly managed and governed. It took a new owner in Boral for this to change and we suspect the opportunity and playbook is similar at Fletcher Building. Sell non-core assets (Australia) for a good price (they are decent assets in the right hands – and buyers of building materials businesses are around – just ask CSR and AdBri), reset the balance sheet, rule a line under sloppy risk management and renew board and management. The upside for the effort could be significant. Without some of these changes unlocking value looks hard. In his outgoing remarks, the Chairman made it very clear why this was never going to happen with the incumbents in place: “The core businesses are doing really well. They are more focused and profitable, with improved earnings, margins, and returns. Looking forward, is our view that it is in the best interest of the business for us to hand over to a new Group CEO and a new Chair who will be able to focus on leading the organization forward” – Bruce Hassell, FBU Chair on his resignation. We are not sure what business Bruce is looking at – but it certainly sounds nothing like Fletcher Building under his watch.

The consumer

Overall, the consumer remained robust and companies are not seeing the recession fears analysts had assumed and many stocks had been priced for. This sector saw the most upgrades along with the Energy and Financial sectors.

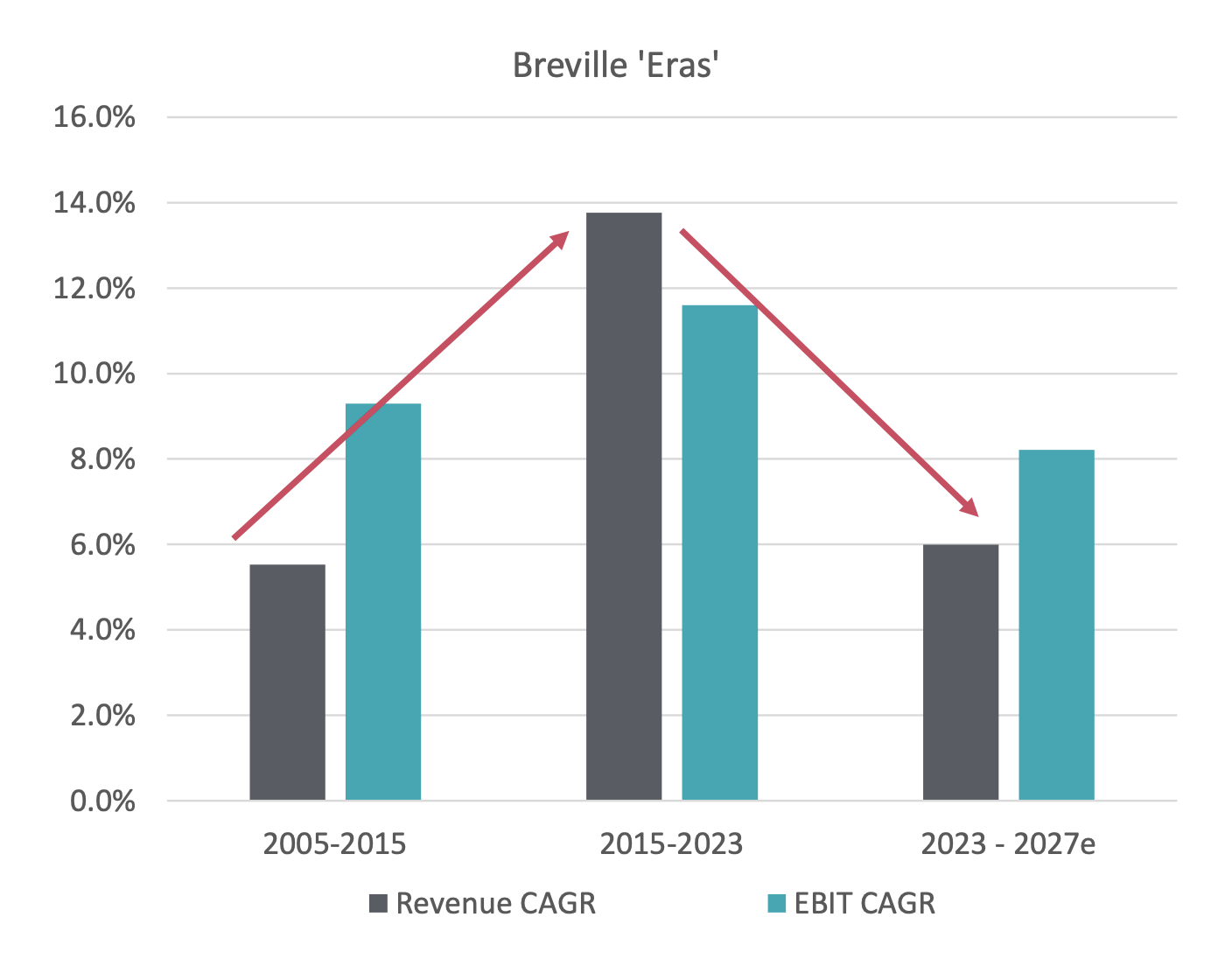

One polarising consumer stock is Breville Group. For a decade (F2005 to F2015) Breville grew revenue (excluding the disposed homewares business) at around 5% p.a, and EBIT at 9% p.a as margins expanded. The stock traded at an average forward P/E of around 13x over this decade priced as a cyclical, mostly domestic, appliance maker. New management (still in place) accelerated focus on global markets and delivered revenue growth of almost 14% p.a between F2015 and F2023, albeit at a slight cost to margins resulting in EBIT growth of around 12% p.a.

Source: Longwave Capital Partners, Company Accounts, Bloomberg Consensus Estimates

Source: Longwave Capital Partners, Company Accounts, Bloomberg Consensus Estimates

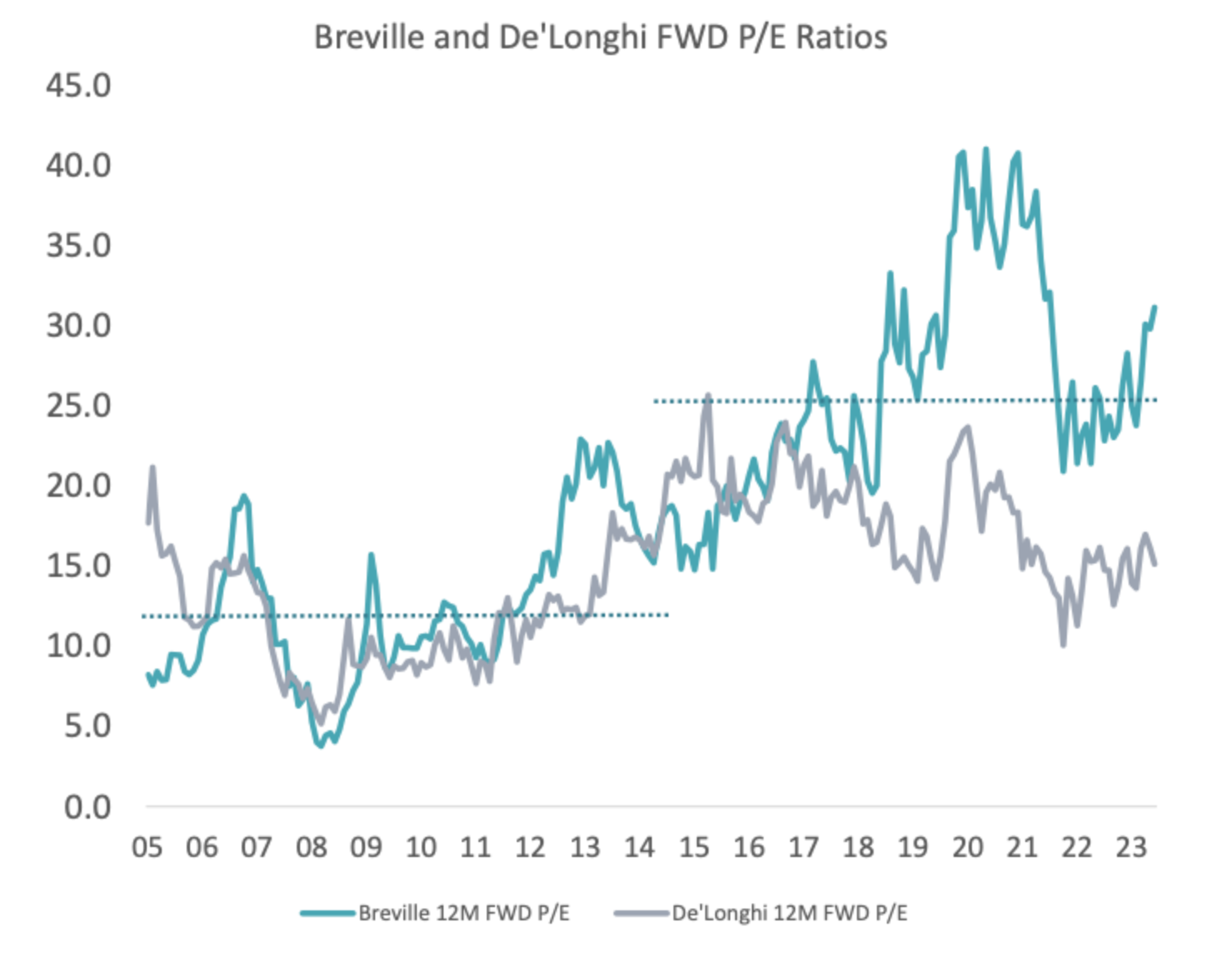

The market rationally rewarded a well-executed global expansion and the stock traded at a forward P/E that averaged 28x. It appears this new market entry growth has largely run its course. The business has fewer levers to pull on either margin or revenue growth and at 30x forward earnings, the stock is still priced for the glory days of future global growth rather than the more realistic return to mid-single digit growth. If investors applied the De Longhi P/E multiple (15x) to the consensus BRG F2025 EPS (A$0.91 cps) the stock would be trading under A$14 – a far cry from the A$27 it trades at today, saying nothing of the downside risk to F25 EPS estimates given evidence of slowing growth.

Source: Longwave Capital Partners, Company Accounts, Bloomberg Consensus Estimates

Source: Longwave Capital Partners, Company Accounts, Bloomberg Consensus Estimates

We saw conflicting messages coming out of the travel sector. Some (Corporate Travel and Flight Centre) feel that the post COVID recovery is now complete and the next five years will be about gaining market share. Others (Qantas, HelloWorld, Auckland Airport, Tourism Holdings) still see more upside back to pre-COVID levels of spending. There are some good businesses here that we think can compound earnings at double digit rates for many years but the rising tide lifting all may be coming to an end sooner than we thought. Competitive advantages and execution will matter more than ever.

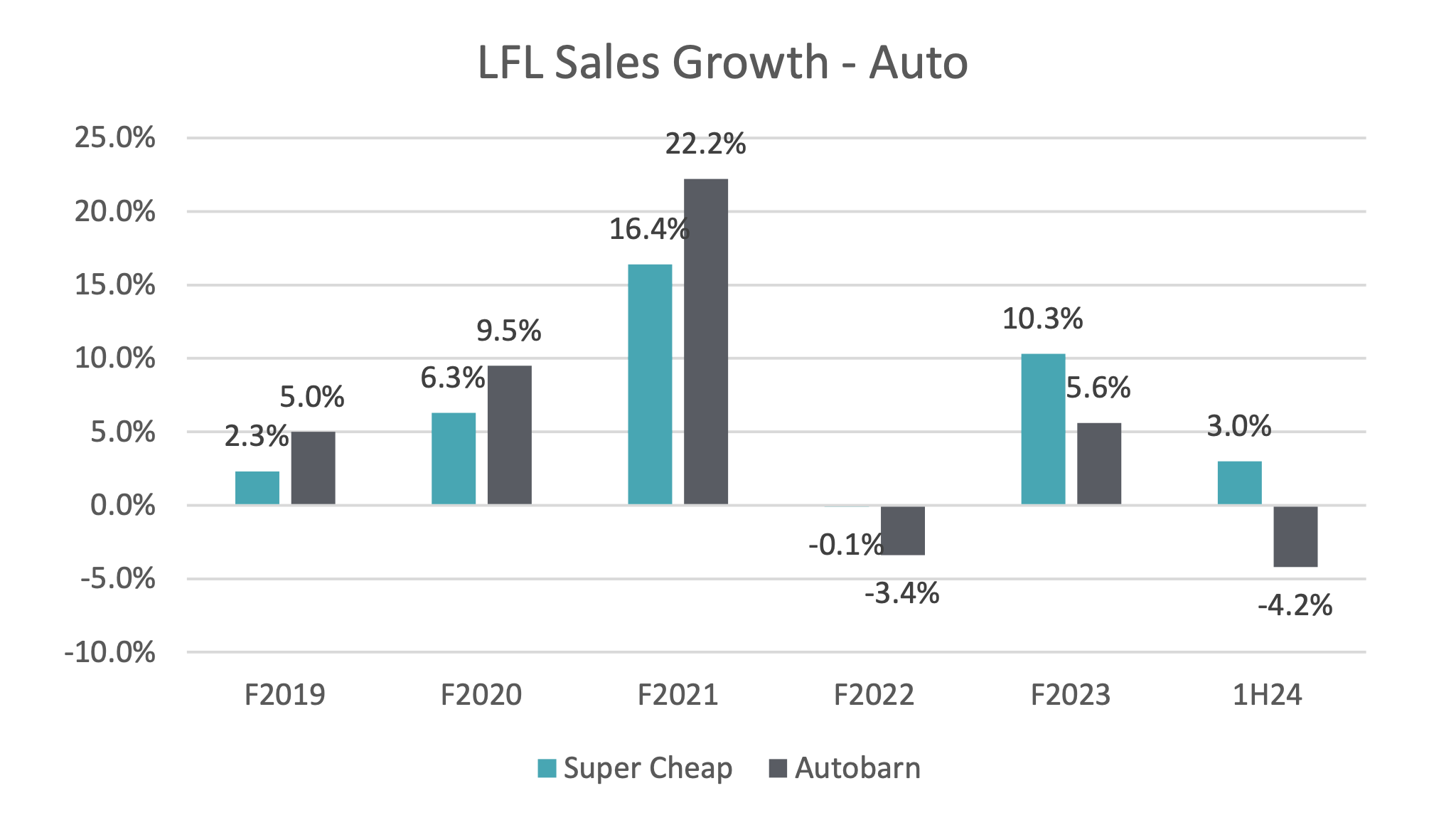

Since the pandemic, limited availability of new cars was seen in a) the novated lease providers inability to fulfill their order books and b) the retail auto dealerships able to significantly improve margins through mix (fewer cars going to fleet and novated buyers) and discounting (as in, there wasn’t any). Novated lease providers were given a lifeline in the form of Electric Vehicle (EV) Fringe Benefit Tax (FBT) relief, but the eventual return of ICE and Hybrid car supply will help them address their full pipeline. Investors should also expect a decline in margins for retail dealerships as the benefits accrued to them from tight supply abate.

Source: Longwave Capital Partners, S&P Cap IQ (Actual and Estimates)

Source: Longwave Capital Partners, S&P Cap IQ (Actual and Estimates)

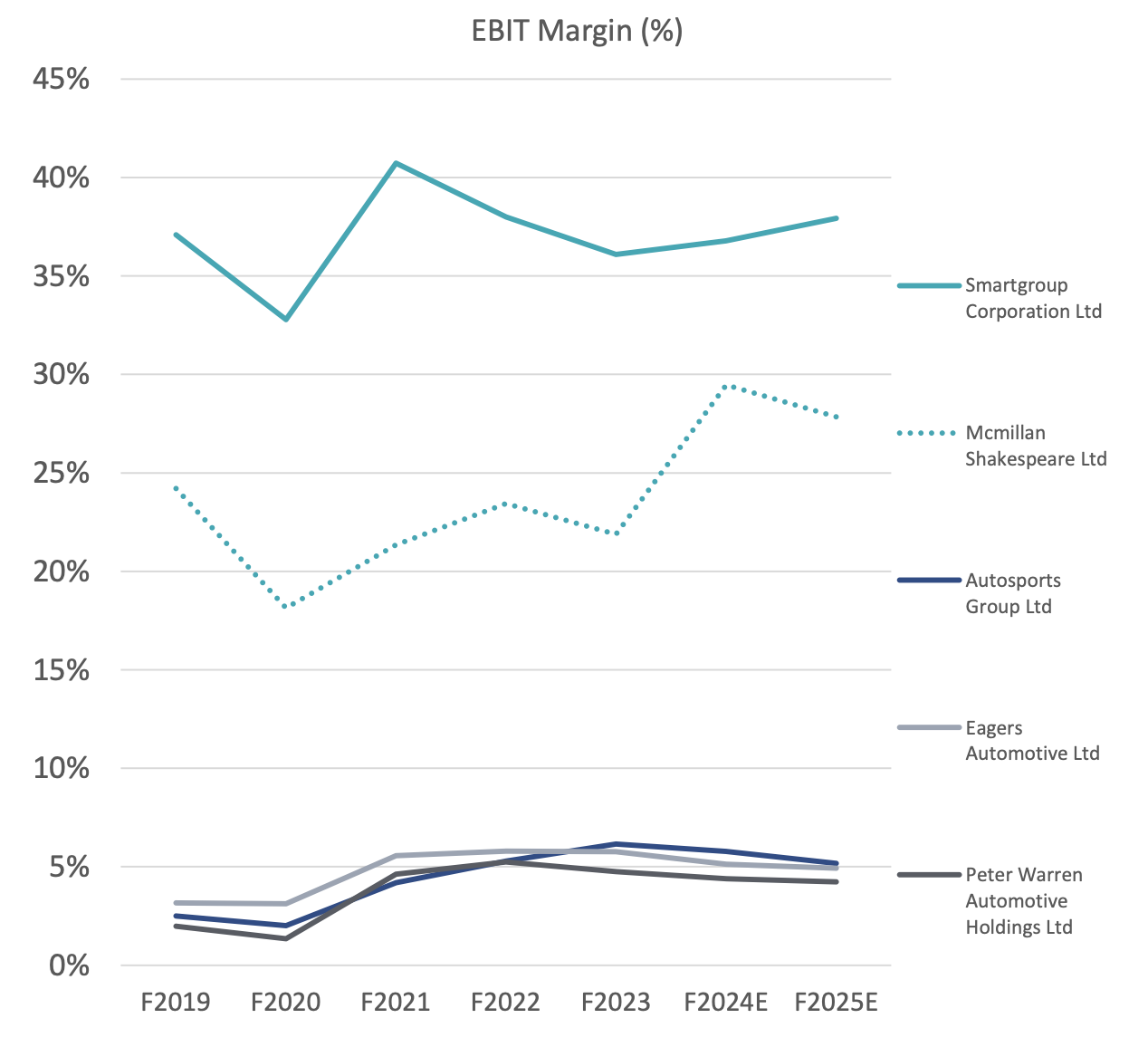

Growth in EVs stimulated by government policy resulted in a strong revenue and earnings increase at McMillan Shakespeare and SmartGroup. Higher prices in general for EVs means higher dollar margins per sale. Since Peter Warren Automotive listed in April 2021, the two novated leasing players have outperformed the three major auto retailers by 20-30% per annum.

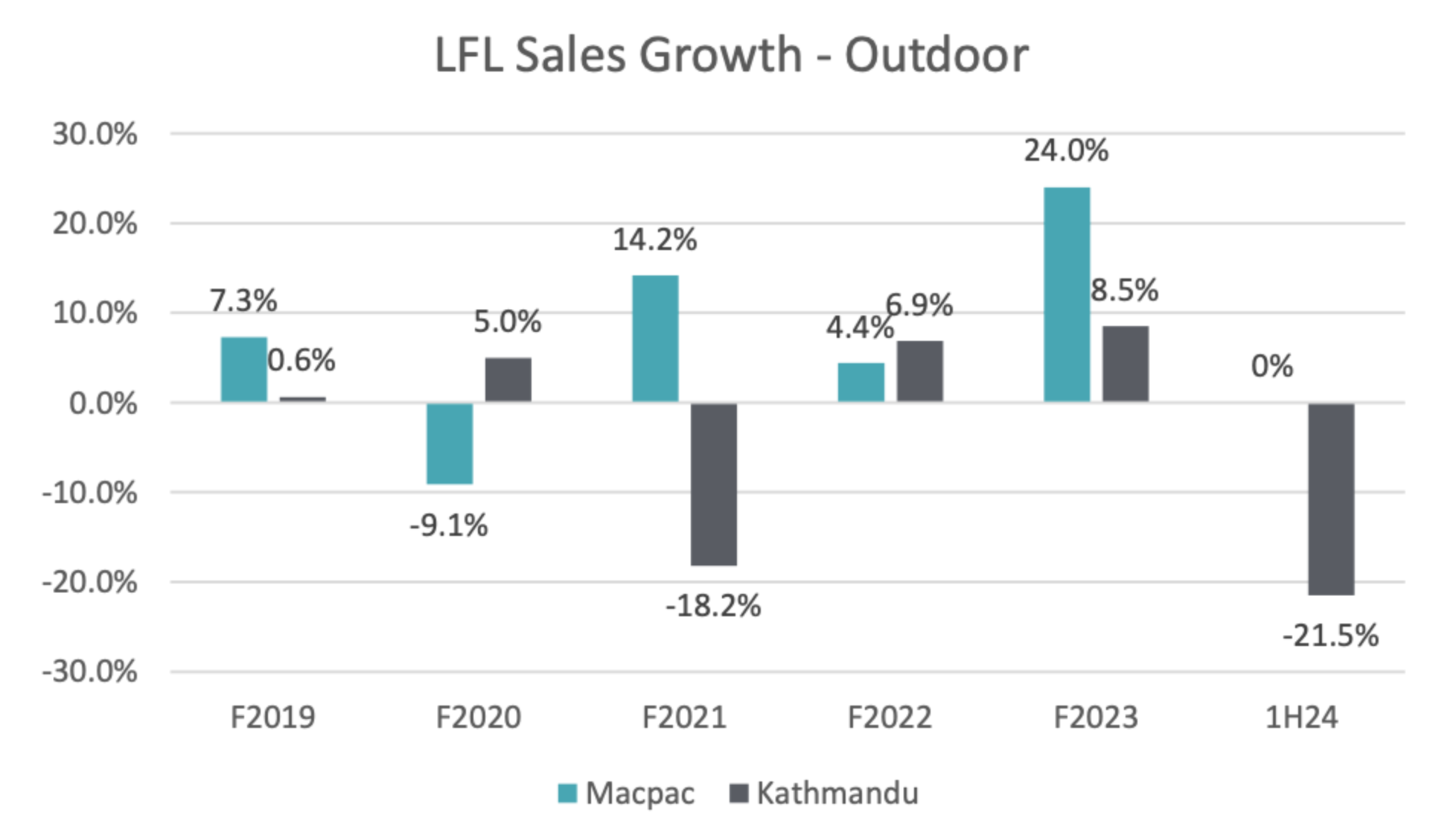

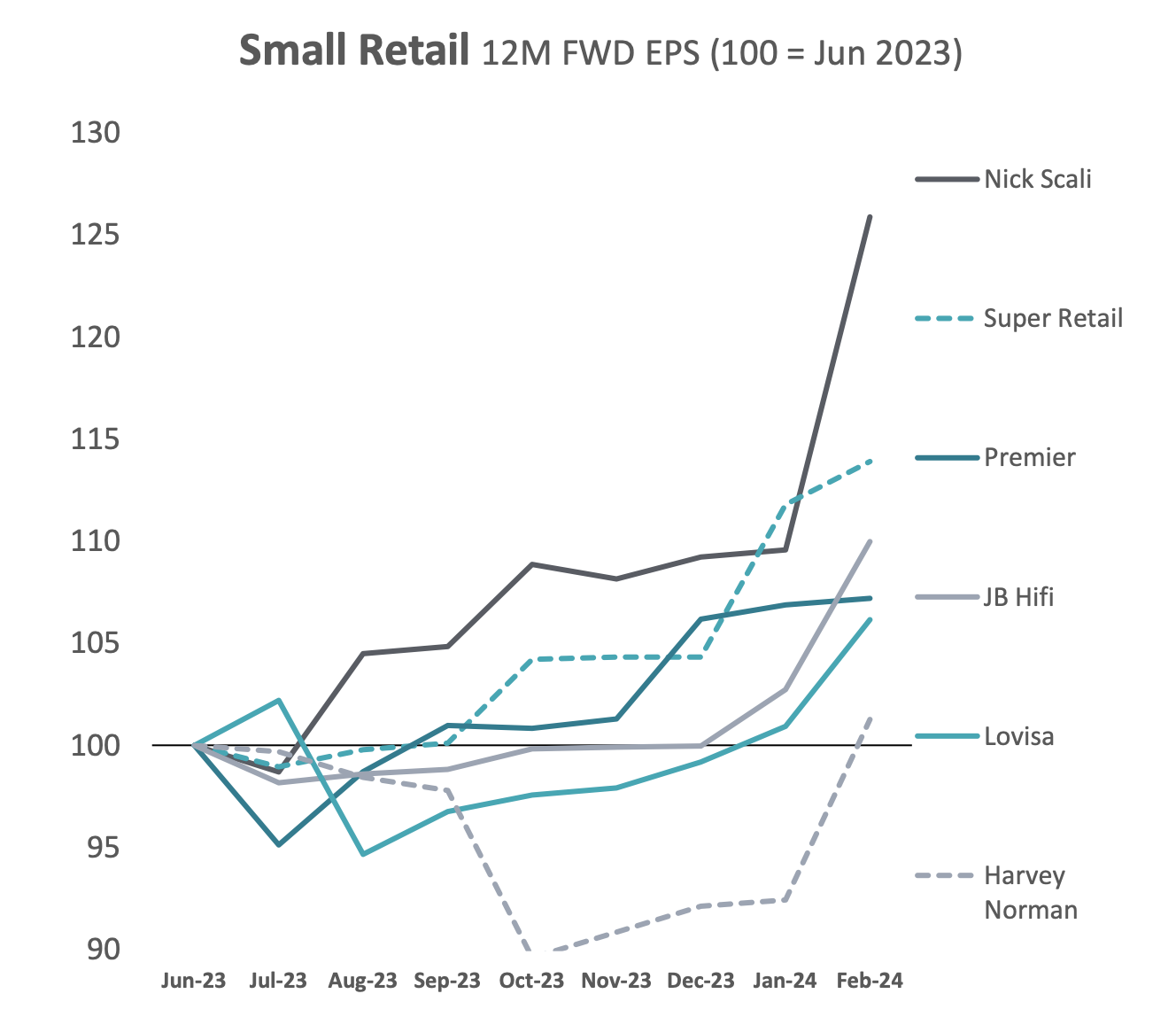

The specialty retail sector is hard to generalize. The one trend we observe is stronger businesses (think JB Hifi, Super Retail, Lovisa, Premier Investments, Nick Scali) appear to handily out-execute their rivals regardless of the macro conditions. Turnarounds in the sector are difficult to affect – some of these lessons we learned the hard way with unsuccessful investments in The Warehouse and Kathmandu, and Adairs.

Source: Longwave Capital Partners, Company Accounts

Source: Longwave Capital Partners, Company Accounts

Source: Longwave Capital Partners, Bloomberg Consensus Estimates 5 March 2024

Healthcare

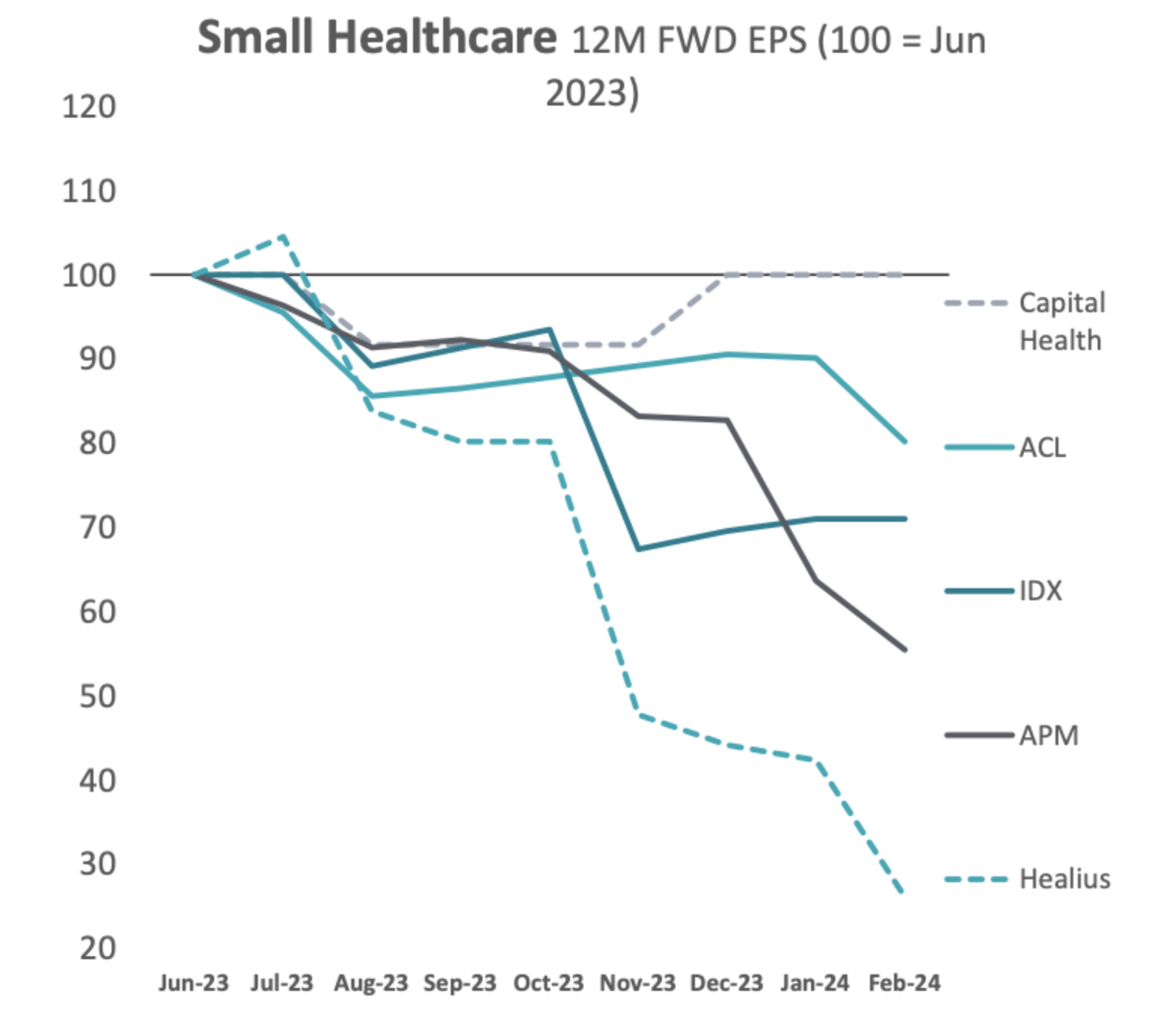

For a sector coveted for government backed certainty, small cap healthcare investing is anything but certain. Healius and Australian Clinical Labs appear to be doing their best to have investors question whether pathology is even a good business to be in anymore. Any business where revenue is capped and costs are uncapped (and subject to considerable inflation) can quickly find the economics inverting. Hoping the government restores your economics can be a painful journey – as Aged Care and Child Care companies have found over the past decade.

Source: Longwave Capital Partners, Bloomberg Consensus Estimates 5 March 2024

Despite what the market is pricing, Nanosonics does not appear broken to us. A new CFO has brought some timely discipline to expenses and the high value consumables continue to grow. Uncertainty over near term Trophon sales and CORIS commercialization costs are dragging down short-term group results, however we continue to believe on a medium-term horizon the core Trophon franchise – without anything attributed for the CORIS product – is worth considerably more than the current market cap.

Mining services

A sector almost as unloved as resources, mining service companies have been a long time improving their results to limited attention from investors. The results across the board ranged from solid (Monadelphous, NRW Holdings), better than expected and well ahead of what the market is pricing in (Macmahon, Perenti, SRG Global) to stellar (if not more well priced) in the case of Mader.

Source: Longwave Capital Partners, Company data, WA Department of Mines, Factset. Wt Avg PE = Market Cap weighted.

Our medium-term expectations are that ongoing commodity demand growth should be met by a more disciplined mining service sector and continued improvement in financial performance. MMA Offshore does highlight that eventually the market will take notice.

Source: Longwave Capital Partners, Company data and reports, Factset

Technology

In a market where sentiment was favourable to growth (eg. Weebit Nano, Brainchip, and Life360 performing well despite either borderline profitability, or none at all), many technology stocks missed the boat (eg. downgrades from Iress, Data#3, Hansen). The technology sector was a net contributor for the Longwave portfolio with it’s focus on organic growth and strong balance sheets. We saw upgrades from Codan, Audinate, and RPM Global.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.