Reporting Season

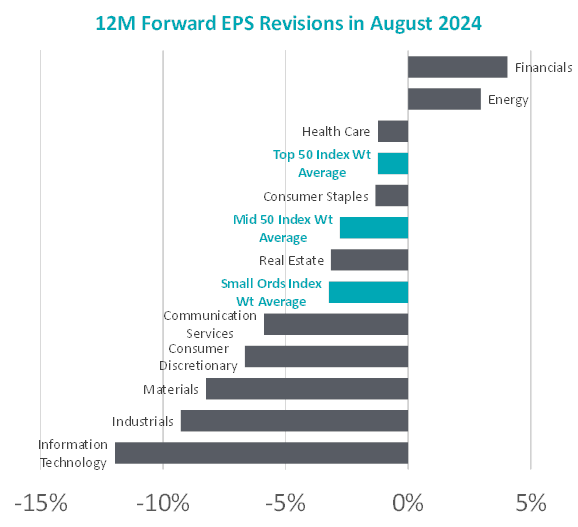

This reporting season was not great across the market, with forward EPS downgrades in large (-1.2%), mid (-3.5%), and small cap (-3.4%) indices. Some of the biggest downgrades in each group included Mineral Resources (MIN), Seek (SEK) and Bluescope (BSL) in the ASX top 50, Whitehaven Coal (WHC), Telix (TLX) and IGO Group (IGO) in midcaps and Audinate (AD8), Tabcorp (TAH) and Nufarm (NUF) in smalls. This year our portfolio had more than its share of the short-term disappointments, directly contributing to the underperformance during the month.

The year to August 31, 2024, also shows some interesting performance trends, with Small Caps (+8.5%) underperforming Mid-Caps (+9.8%) and Large Caps (+16.3%) echoing the revision to earnings expectations.

One observation across these results was the evidence of demographic changes in specific sectors. It is not just office occupancy dealing with changes in consumer preferences. Drinking, gambling, fast food, traditional media and active funds management are all seeing structural headwinds. A decade ago, these were still considered growth industries. In 2024 most companies in these industries can’t even pass on inflation. Large cap investors often contend with sector themes that dominate results – banking, iron ore and supermarkets tending to be the calls that make or break an active funds performance. Reporting season is once again a reminder of just how varied the businesses, industries, and performance outcomes are in small caps.

Source: Bloomberg, Longwave Capital. Sep 2024

Resources

Within small caps the price performance divergence between industrials and resources has become extreme, with one year returns +12.2% (Industrials) vs -1.8% (Resources) respectively. On a two year basis this increases to a 26% difference (+14.7% vs -11.5%). Although we have avoided the speculative parts of the energy and mining sectors (lithium and uranium) we do invest meaningfully in small resources and have been impacted by the relative underperformance. Specifically in August, our mining investments in coking coal producers – Stanmore and Coronado – both performed poorly. In energy, Beach Energy was one of our largest detractors as delays at the commissioning of Waitsia and the unexpected reserve downgrade at Enterprise undid what we think is good progress in the reset of the business. This is a company still in the early stages of new management and our thesis over the next three years here is simple – growing production at lower cost, selling into a market seeing structurally higher prices over time as the east coast gas shortages become more acute. The near-term results have been testing, but we continue to believe the investment merit in the medium term is sound.

Financials

This sector was the largest performance detractor for the month, but it really came down to not holding positions in Zip, Judo and Pinnacle Investments (which we cannot hold under our investment guidelines). There continues to be bifurcation in the fund manager results, and lots of turbulence as new management (Platinum), a new board strategy of M&A (Magellan) and almost everything going on at Perpetual compares with the continued march upwards of GQG (at least in FUM terms).

We do not favour balance sheet lending businesses in small caps as through a cycle the bad debt experience tends to overwhelm any short-term illusion of profitability, but there are lots of other interesting quality financial sector businesses which in general performed well. These include modern platforms (Hub24 and Netwealth) who continue to take business of legacy providers (including Insignia – IFL), payments businesses (Tyro), Insurance Brokers (AUB Group) and other financial services companies (Helia, OFX Group, EQT Holdings).

Communication Services

We reduced our investment in Spark NZ during Q4 2023, but given the trading update and price performance in August we wish we sold a lot more. Not owning Chorus, who were rewarded after bumping up their dividend even though the underlying business saw similar EPS downgrades to Spark, showed just how much we held the wrong NZ telco during the month. Chorus does have the benefit of being a regulated asset from a certainty perspective, and although Spark have the potential to reinvest in growth opportunities (like NZ data centres) their track record hasn’t warranted the market paying for this potential right now.

The other observation from these results would be that if you think the economics of the traditional media business can’t get any worse, you maybe just need to give it more time. Whether it is Pay TV, free to air, newspapers, radio or even outdoor advertising, the movement of dollars to where eyeballs have gone (online) and the inability to reduce operating costs at anything like the same rate shows up in profits dropping further and faster than expected.

Consumer Discretionary

Stock prices mostly followed the direction of travel for the underlying business trends, with Tabcorp, Corporate Travel, Lovisa, Cettire, Adairs, Jumbo Interactive and Collins Foods all showing operating weakness and trading down accordingly. Harvey Norman was probably unfairly treated in our view but reporting on the last day of the month means the on-the-day price reaction (which often weeks later proves to be the completely wrong interpretation of results across the small cap market) was captured as the months performance.

On the other side, Breville continues to be rewarded for delivering as expected results (which to their credit includes a long-awaited reduction in inventory) and although we struggle to make sense of the pricing relative to global market peers (such as De Longhi), it wouldn’t be the first Australian stock to sport such a premium. Sometimes they come unstuck – such as Domino’s Pizza, and other times they set new record highs like Pro Medicus or Wisetech.

Information Technology

IT has again become one of the more interesting sectors in the small cap market. We have seen some remarkable business turnarounds here in the past 2 years, such as Bravura and Nuix, as well as some remarkable negative surprises, this time from Audinate and Megaport. Our portfolio has more of the “slow and steady” tech companies which in general delivered results in line with our investment views (Codan, Objective, RPMGlobal, Gentrack and Infomedia for example). We don’t mind quality compounders in tech at all – not everything needs to be feast or famine!

Industrials

The Industrials sector remains the largest overweight in the fund and was a positive contributor during the month. SRG Global, Auckland Airport, Freightways and NRW Holdings all delivered strong results. Although the price reactions for SmartGroup and McMillan Shakespeare were both sharply negative, we think the results were solid and the opportunity in novated leasing and EV uptake remains a tailwind to both client activity, revenue and margins. Once again, it may take a few weeks for the initial price reaction to settle down and reflect the underlying fundamentals of the companies.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.