Long term consumer tech winners

In modern consumer technology businesses, what is the recipe for success? With so many examples globally, it has become far easier to look at what works for the business, the range of financial outcomes and how the market prices these companies. Life360 is probably the leading Australian listed consumer tech business. A far greater share of Australia’s successful technology companies are B2B (Xero, Wisetech, TechnologyOne, Pro Medicus) and we recently discussed some of their success factors.

Global listed companies that appeal to the consumer include household names like Meta (Facebook, Instagram and WhatsApp), Netflix, Uber, Pinterest, Spotify, Snapchat, Match.com. Consumer companies are interesting in their appeal to psychological factors and the ability to monetise through advertising – features far less common in B2B software business models.

In this note, we offer a simple three step framework to look at how consumer technology companies succeed and the commercial reality that unless you nail all three of them, the long-term returns are likely to disappoint, and short-term returns will be volatile.

1. Market Success – Can the business find Product / Market Fit? Can it deliver a product or service that is so compelling, millions of people will not only adopt it, but will pay to use it (either through a paid subscription or through advertising). We can measure this via non-financial metrics such as monthly active user growth over time and the translation into revenue.

Why is this hard? Because finding large scale new businesses is a trial-and-error endeavour. Failure is the default mode and even some of today’s large success stories contain pivotal moments where failure was narrowly averted. Winners can look obvious in hindsight, creating a narrative effect used to anoint unproven companies that may look similar.

2. Commercial Success – Can the company translate market success into profit and cash flow? Seems logical, but for many companies, product market fit is found in an unsustainable way. Selling products or services for less than they cost to produce and/or maintain. This begs the question whether the consumers truly like the product, or just like the subsidy they are indirectly getting from company shareholders.

Why is this hard? Because once someone figures out what product or service works, the great potential economic rewards incentivise competition. This could be bidding up the cost of employees. Or customer acquisition costs. Or lowering prices. The world has become more efficient at figuring out what works, and only true competitive advantage will allow companies to generate and sustain growth with profits and cash flow. We saw this is 2022 and 2023, with the move to unlock margin and some businesses showed as soon as they tried to reduce investment, growth slowed dramatically, and the sustainability of their user base became questionable.

3. Governance Success – Can the company align commercial success with minority shareholders relative to the potentially competing interest of founders, management, employees, directors and the government?

Why is this hard? Because once a pot of gold is realised, many people want to extract their rent.

Market success is necessary but not sufficient for a long-term compounding of value in these businesses. Commercial success usually gets you most of the way there, so long as governance risks are kept in check.

A couple of examples help highlight how this can be observed.

Meta – the gold standard. Over 3bn daily active users. A decade of 12% p.a user growth, 30% p.a revenue growth, operating margins averaging 40%, free cash margins averaging over 30%, shares on issue lower than they were a decade ago and a Total Shareholder Returns (TSR) of 22% per annum. 10 years ago, the market paid a peak of around 12x revenue for Meta with all this growth to come. Since 2017 the market has paid between 2 – 8x revenue depending upon how optimistic or pessimistic investors are on risk or growth.

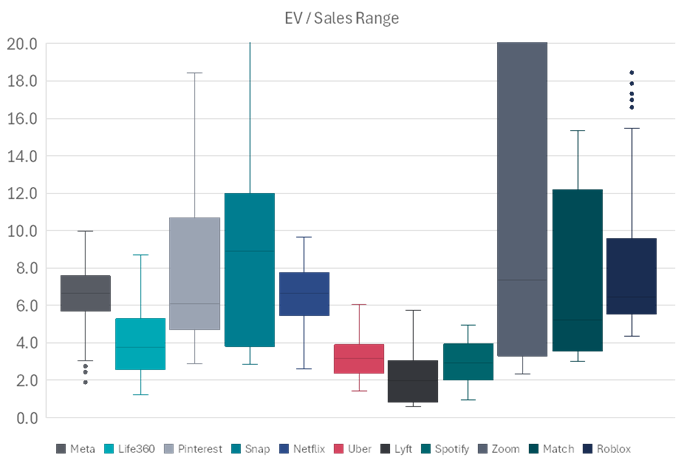

SNAP – Off a smaller base (71m users in 2014) SNAP (and the Snapchat app) delivered a decade of user growth at 20% p.a. Monetisation of users from an even lower base saw revenue growth of 72% p.a and is now a US$5bn a year business serving over 500m users. This is where the good new ends – SNAP has been loss making every year with no benefits of scale showing in the financials. To fund these losses, shareholders have worn equity dilution of 16% p.a (share count almost 3.5x the level of the 2017 IPO) and net debt going from US$2bn net cash post IPO to US$800m net debt today. TSR has been -10% p.a since the IPO and the market having paid 10-20x revenue in the past (2017 – 2021) now pays about 3x as the economic reality of not being “the next Meta” is reflected by investors. Paying 20x revenue in Dec 2020 locked in -32% per annum returns over the next 4 years as the multiple collapsed to reflect commercial reality.

This story is repeated multiple times across the market. There is a reason why “winner take all” describes these categories. For every Meta or Netflix that convert market success and monetisation into wonderful business economics and terrific long term shareholder returns are a long list of companies that look like they have the same business model success, but without the financial results to back it up, the shareholder returns just are not there.

Then there is the issue of valuation

Netflix has been a total return monster for shareholders, delivering 34% p.a over the past decade, but shareholders that paid close to 10x revenue in mid-2018 realised returns of 13.5% p.a (below the S&P 500) despite operating profits compounding at 43% p.a over the same period.

Businesses have the challenge of finding market success and converting that into superior financial economics. Investors have the additional challenge of ensuring they don’t pay too much that either a) completely offsets the wonderful business performance (eg: Netflix) or b) suffer a crushing de-rating as the failure to become one of the winners that take all gets reflected in the multiples investors are now willing to pay (eg: SNAP). Multiples swing wildly (a range of 3-20x revenue for Snap in a five-year window is pretty extreme) as investors try and figure out if the market success narrative will convert into superior business economics.

Source: Longwave Capital Partners, Bloomberg 2Yr fwd EBIT Margin and EV / Sales Estimates. 31 Jan 2025.

What does that mean for the Australian market?

We see many stocks here that have achieved great things – finding global market success in their niches – but a far smaller number that have converted that into superior business economics.

Take Life360 (360.ASX). Life360 has a dominant position in the mobile location tracking market (“Family Life”) and delivered the markers of success discussed earlier – strong growth in users, a subscription model which demonstrates value to the user base and converts into strong revenue growth. So far, the financial performance has shown difficulty in converting this market success into commercial success (profits), but there has been progress here as losses have reduced and breakeven is within sight.

The market loves Life360 – which we can infer by the current EV/Sales multiple of ~7.5x, nearly as high as it has ever been (a range of 1.5 – 8x being the relevant history here). The management recently provided investors aspirational goals for the business which we can use to estimate one version of fair value. The aspirational goals are 150m+ active users (double 2024 levels), US$1bn+ in revenue (almost 3x 2024 levels, which tells us monetisation is expected to increase per user – most likely from advertising) and EBITDA margins of 25%+. Adjusting for both stock-based compensation and depreciation eats about 5% of EBITDA, so let’s call it 20% target operating margins.

Source: Longwave Capital Partners, Bloomberg 2Yr fwd EBIT Margin and EV / Sales Estimates. 31 Jan 2025.

If we assume it takes Life360 five years to get to these aspirational targets (est. 2029) what is a reasonable estimate of fair value?

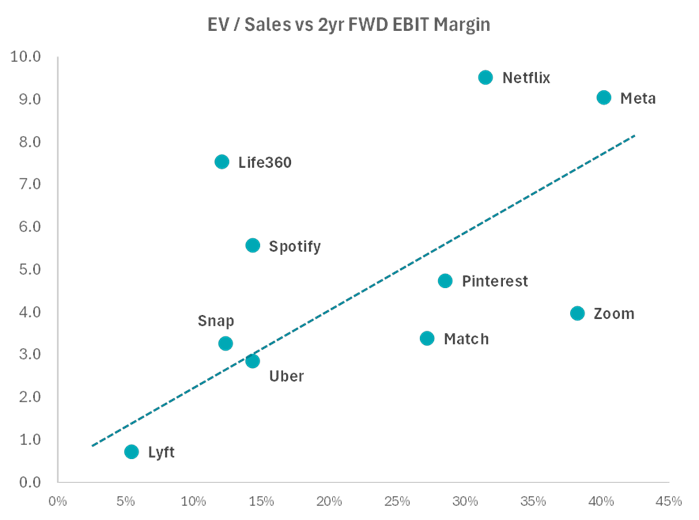

Terminal revenue multiples are linked to terminal margins for intangible based businesses, so a 20% margin business should trade on half the multiple of a 40% margin business all other things being equal (“all other things” being a big bag of assumptions). Meta at 6x revenue and Life360 at 3x both imply a 15x terminal EBIT multiple. When we turn our minds to terminal values, we may start to consider that users of Snap and Life360 have a higher risk of “ageing out” or churn given they are particularly relevant at a specific life stage (ages 13-20 for Snap, and parents with children of a similar age for Life360). So perhaps the value of a dollar of Meta EBIT is higher than a dollar of Snap or Life360 EBIT at maturity given the higher longevity of their user base.

Three times aspiration revenue implies US$3bn of Enterprise Value (EV) for Life360 in 2029, which discounted back to today at a 10% discount rate is equal to around US$1.9bn. The current EV of Life360 is US$3.4bn today (31 Jan 2025). Is it possible that like the investors who paid 10x revenue for Netflix in 2018 (which ended up delivering almost at Meta type margins through the financial statements), investors in Life360 today may end up with a similar outcome even if the aspirational targets are achieved? What happens if the commercial outcome achieved falls short of management aspirations, like so many others – in fact the majority – of companies in this industry? Optimism and recent share prices are positive, but valuation and commercial industry success base-rates tell a different story.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.