Key takeaways from reporting season

Communication Services

“Due to fragmentation, it is increasingly hard to generate mass reach quickly in mainstream media.” oOh!media

Money follows eyeballs… The shift away from traditional media does not appear to be stopping anytime soon. As audience numbers continue to decline for traditional media, earnings surprises in this space have mainly been driven by cost control rather than revenue growth. Despite challenges for traditional media, the Outdoor segment has demonstrated its ability to attract advertisers. oOh Media! has closed out 2024 with a much less risky contract expiry profile and has commenced the new financial year with revenues up double digits.

“As of the end of September, collectively, Challenger’s made up some 19.8% of the market. We believe this multiyear trend has plenty of runway left and now see our long-term vision of the challenges as a group reaching 30% is perhaps understated.” Superloop

Although Telcos have traditionally been thought of as defensive stocks, the latest result from Spark NZ would suggest otherwise. The tough New Zealand economy has led to spending cuts, mobile fleet reductions across government and business and aggressive price competition in mobile segment. All this equates to lower revenue and with ongoing cost inflation another earnings downgrade. The operating environment is not as tough in Australia, with local Telcos able to pull the price lever without material impact on churn.

As large telcos are looking to protect and grow earnings via their Mobile business, challenger brands such as Aussie Broadband & Superloop continue to take market share in the broadband segment. Superloop appears to be on track to become profitable in FY26.

Consumer Discretionary

“BYD is running at 170 orders a day versus 60 this time last year. So it’s through the roof. All you need to do is look at how BYD perform in China relative to those same competitors. And it’s a gorilla. It is them, then there’s daylight and then there’s whoever’s next” AP Eagers

Supply and demand are a pretty good indicator for price, and few places in the past five years was this more evident than in auto retailing. The three listed retailers (AP Eagers, Peter Warren and AutoSports) saw their pricing power and margins benefit enormously when supply of new cars was constrained during and post COVID. Car dealers withdrew volume from lower margin channels (such as novated and fleet) and removed any discounts for new car buyers on their lots. As supply returned, their privileged position in the market receded as did their margins.

On the other side, the novated leasing companies (SmartGroup and McMillan Shakespeare) saw a return to growth in ICE vehicles, on top of the government stimulus assisted growth they have enjoyed in EV and Plug-in Hybrids. AP Eagers are indicating at this result they believe retail margins have bottomed, although for them this may be as much about capturing greater finance margin as margins on the car itself – Peter Warren and AutoSports were not as confident. We still prefer the capital light model of the novated leasing companies.

“In short, we faced a more cautious consumer, a more aggressive competitive set and rising essential operating costs.” Super Retail Group

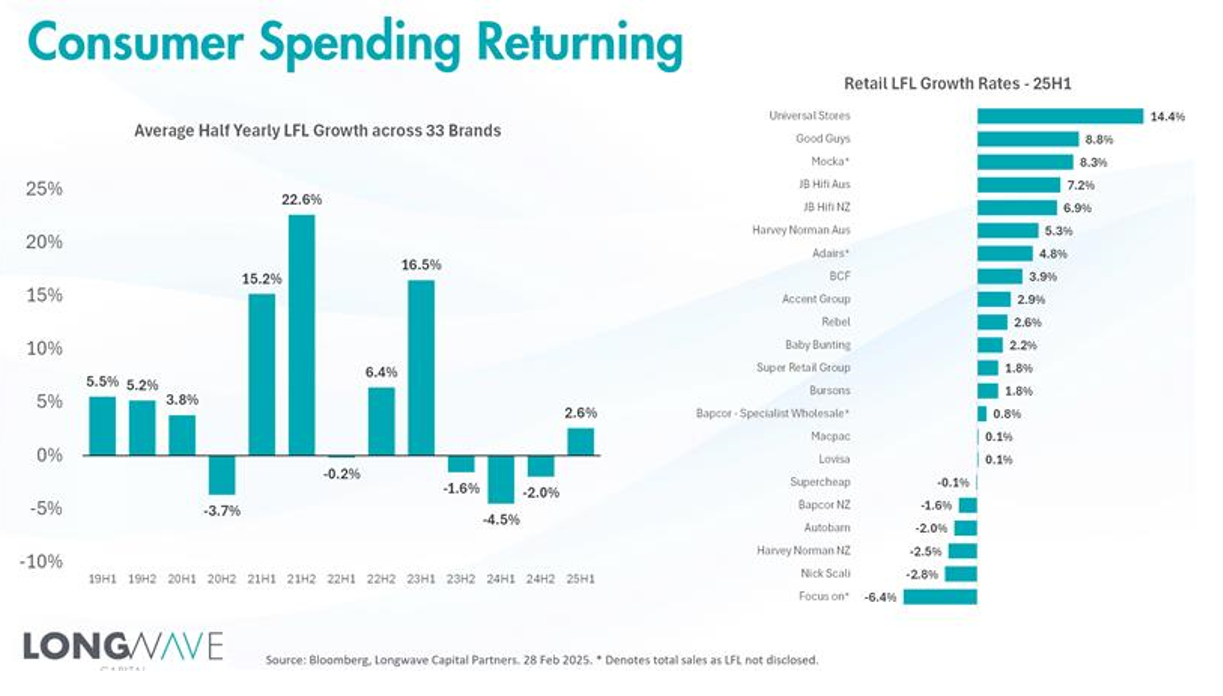

Post-Covid, retail management teams reassured the market that they have changed consumer behaviour and are able to generate growth without the same level of promotional activity. This may be the case to a certain degree, but the tough consumer environment has translated into higher levels of promotions and in most cases contractions in gross margins. Super Retail and Bapcor in particular faced elevated competitive intensity in the Auto retail market, profit margins were squeezed as they were unable to offset with cost savings. Certain categories such as consumer electronics performed especially well as seen in the results of Harvey Norman and JB Hi-Fi, which highlighted that the consumer was still spending but was just more targeted.

While pure play online retailers saw strong growth, execution varied across the industry. Temple & Webster impressed the market with strong revenue growth in the period while maintain a disciplined approach to marketing. In contrast, Kogan shocked the market with their trading update, spending heavily to chase growth at the expense of profit.

Consumer Staples

Despite pressure in the cost of living and significant consumer down-trading evidenced in the Coles and Woolworths results, Bega grew their branded segment sales and margin during the half year more than might have been expected in this type of environment and they also saw a significant bounce back in the profitability of the commodity bulk business. Despite this, many of Bega’s forward-looking comments were slightly negative (challenging consumer environment, farmgate prices likely to rise in FY26) and coupled with the management telegraphing that they would like to buy the Fonterra Consumer business that is up for sale, the stock price underperformed post result.

Energy

Beach Energy saw a negative market and sell side reaction to a slightly lower 1H dividend payout, rubbing salt into the wounds of the disappointments of Waitsia commissioning – but in our view overlooking the three things that will matter over the medium term. Gas production at Beach is increasing, costs are declining and market prices due to a shortfall in supply are rising. Little in this result changed our view that these three drivers of our investment thesis remain intact.

Uranium is the most recent carrier of the most-loved commodity batten, swiftly taking over from Lithium in early 2023. The four horsemen of uranium in small caps are Paladin (since promoted to the ASX100), Boss Energy, Bannerman, and Deep Yellow. Between early 2023 and mid 2024 their share prices were all up 150-200% as the uranium price doubled (From US$50/lb to US$105/lb). As uranium has since retraced back to US$64/lb so too have the prices of these stocks to levels close to where they started in early 2023.

Financials

Funds management companies like Platinum and Magellan continue to struggle with their turnaround strategies. Both companies have had significant turnover in both management and investment teams and this has continued in recent months leading to a continuation of recent outflow trends. Perpetual is another turnaround story which has done less than hoped to reassure the market of their progress. Following the collapse of the KKR deal, management is seeking alternative buyers for their Private Wealth business. Debt continues to increase while earnings in their core Asset Management business are under pressure. Pinnacle was a rare bright spot in the sector, producing a result that was hard to fault, with strong inflows and performance fees for the period.

The ongoing shift to specialty platform providers shows no signs of slowing as Netwealth and Hub24 continue to break net flows and profit records while incumbents such as Insignia and AMP struggle to stem outflows. While Insignia’s cost-cutting initiatives are progressing, the business remains in decline. The company has received multiple bids from private equity to acquire the business which serve as support for the share price.

Healthcare

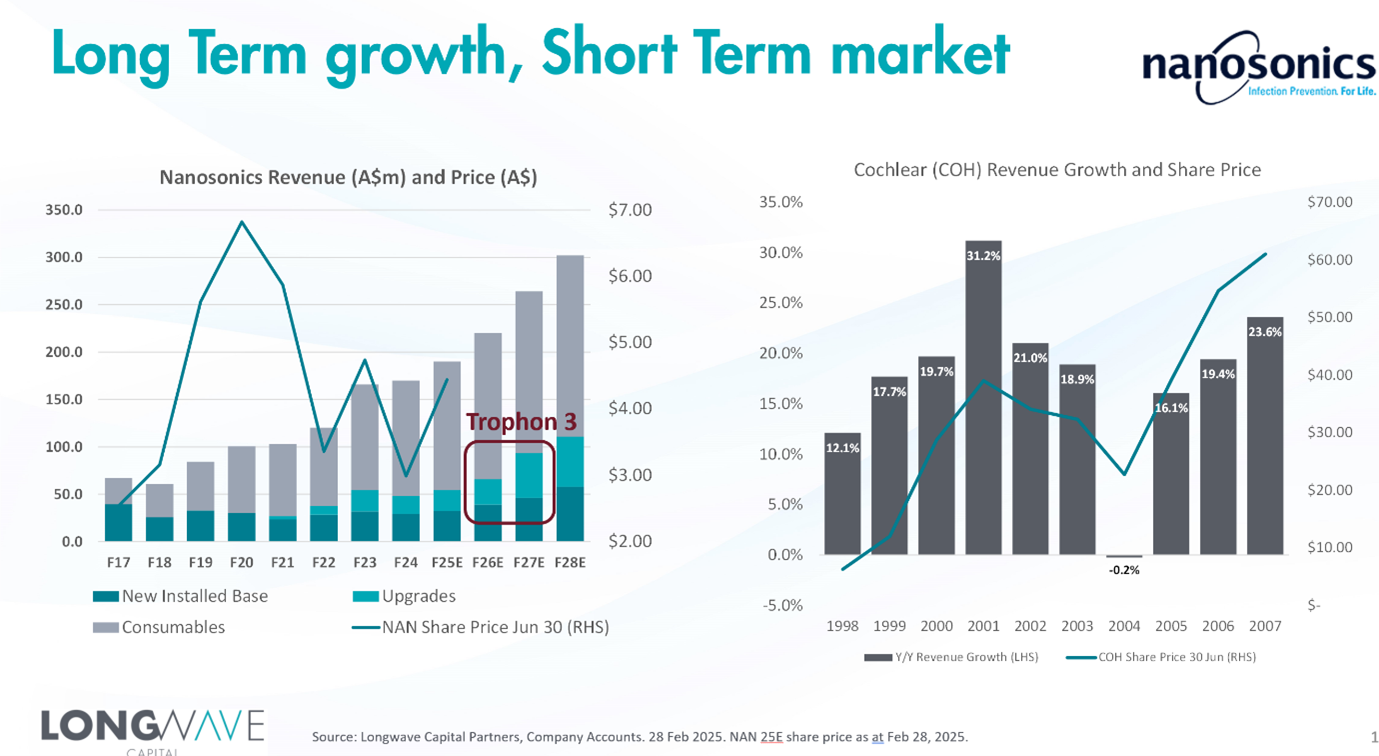

“There’s an upgrade opportunity for over 10,000 devices in terms of aged units. The absolute majority of those units currently get their service from GE Healthcare. Our experience so far with all our upgrades is even if people had been prior serviced prior with GE they switch over to Nanosonics.” Nanosonics

Nanosonics has been a long-term holding in the fund, which we added to in late 2023 with terrible timing as short-term growth was downgraded within months, and the share price followed. As we wrote at the time, and since, our thesis was about a long-term structural growth business and this result reinforced the decision we made to increase our position in mid-2024 on the premise that we were seeing a temporary lumpiness in the growth rate, rather than a structural slowdown due to misjudging the long-term opportunity. Trophon is performing very strongly again, CORIS will likely launch in some form this calendar year and Trophon 3 is ever closer to providing a new product cycle uplift to upgrade sales which will also come with service contracts.

“Rent started at 8% of revenue pre deregulation, it’s now 20% of revenue.” Australian Clinical Labs

Pathology is an oligopoly in Australia that hasn’t seemed to grasp how they should behave to benefit shareholders. Continued intense competition in an industry dominated by three players (Sonic, Healius and Australian Clinical Labs) results in what should be attractive economics leaking out to fragmented suppliers. Healius struggling to earn a 1% margin and ACL in high single digits is a long way from the historic industry profitability. It is also a long way from what we think can be achieved under a more disciplined and more efficient approach.

Industrials

Although it is diversified under the hood, Industrials posted a mixed bag of results and the majority of companies fall into the second-half club.

“we’re in great shape. We’ve never had this order book. All of our programs are let. We have visibility for the next 8 years”. Austal

Austal Ships has gone from completely unloved in mid-2023 to market darling in recent months. This is a well-managed low margin, lumpy contracting business facing the right industry for the times (global naval re-armament). With its recent US Navy Steel ship awards and submarine component manufacturing agreement with Electric Boat, it has more than proved it will be part of the Naval shipbuilding program for the USA industrial base for decades to come. We have held Austal in the fund over the long term and added the position during 2023 when it was trading below net tangible assets. The recent run in the share-price reflects future optionality in the submarine component manufacturing contract and the yet to be awarded Australian Naval shipbuilding contracts.

“Still have a bit to go in margin improvement, but the last half a percent is incrementally harder to get than the first 2 percent. We have a clear path but not an easy path” mining services CEO

We’ve liked the mining services sector for some time due to the increasing sector discipline on contract pricing and capital expenditure, improving returns profile and cheap valuations. That said, most contractors at the half year experienced unexpected margin weakness. Some of this was explained by extended Queensland coal-field wet weather (consistent rain reduces productivity and parks up fleet) or the impact of lower margin, but capital lite businesses being folded into earnings. A range of contractors require quite strong 2H results to achieve their guidance which has weighed on stock prices immediately post-reporting season. Order books and pipelines are strong, however, and the competitive landscape is still very good from a performance and margin perspective.

Johns Lyng was the worst underperformer during reporting season. This is a capital-light business model with a large potential total addressable market. However, its growth has largely been driven by acquisitions, making true historical organic growth hard to see in the accounts. Although Johns Lyng only downgraded guidance for the full year by mid single-digits, it requires a significant 2H improvement to earnings to reach that guidance, and the magnitude of the earnings miss in the first half was large, with organic growth the biggest disappointment.

In addition to this, the newest growth pillar in the USA is yet to prove it can grow at a double-digit organic growth rate. We were un-surprised by the lack of organic growth in Australia as we had detected some time ago that this was a “growing organically by acquisition” business model (one where the presentation materials say one thing, but picking apart the numbers gives you a different picture). The newly added USA business is struggling to demonstrate the double digit organic growth rate originally promised. We think they may eventually get the execution right in the USA, but as always, its not as easy as the theory on a spreadsheet.

“A 21.6% [gross margin] is not terribly surprising to me. As I said, 20% to 22% is the range you can expect from Redox. Last year’s number I pointed out many times was pretty unusual.” Redox

Redox is a relatively new industrial company to the ASX, one of the few IPOs in the last four years. Up until this result, investment performance was as we all hope for from an IPO – three results reported and the stock up more than 100%. This latest result clipped the RDX wings a little as the over-earning (at the gross margin) and need for higher investment in operating costs both flagged prior to this result – although the market didn’t want to hear it until the 1H25 result confirmed the reality. We have looked at RDX in some detail but haven’t owned it.

Information Technology

The tech sector had been outperforming since August 2024, at one point being up over 20% relative to the broader market. February 2025 saw this retrace almost entirely, with the sector being the most downgraded on earnings.

Upgrades only came for Audinate, which was off a low base as customers work through inventory backlogs; Data#3, likewise resolving uncertainty around Microsoft contract changes; and Codan, which is the standout with organic growth exceeding guidance and steady margin expansion. Codan’s results are off the back of several years of efforts to reshape and diversifying its business. They are the quiet achiever in the sector – they don’t get the headlines as the market whipsaws on short term expectations, rather they go about the business of reinvesting for long term growth and delivering consistent outsized returns.

RPM Global divested its consulting business with management believing that a pure software business will make more sense to the market. Indeed whilst overall earnings were downgraded, the focus on high quality SaaS based recurring revenue streams was well received.

Two stocks with similar EPS downgrades over the past few months, and downgrades after results but with very different post result share price performance were Megaport and Siteminder. Siteminder ended the month 22% lower than its pre-result share price, likely due to revenue growth declining for a third half year in a row, and at 13.9% p.a well under the 30% p.a growth rate promised by management. Since 2022 marketing to sales dropped from 40% to under 30%, and product development to sales dropped from 35% to 20% which begs the question whether the need to reduce these costs in order to get the business to break even is also undermining the ability of the business to hit those medium term 30% p.a growth targets. They would not be the first company to make this discovery.

“Probably one of the most important things is to take a new product to the existing customer. It’s very hard to sell someone something if they’ve bought everything that you’ve got. If you’ve got something new, you can expand.” Megaport

The Megaport share price rose 18%, ostensibly on FY25 guided revenue and EBITDA numbers that were largely unchanged, if anything trimmed slightly by consensus. The difference here however is that MP1 has sustained its profitable position while investing heavily in new go-to-market capabilities, and new products which this result showed the first signs of paying off. Net revenue retention increased, new products are coming to market and most importantly, the signs of the new sales team delivering new logos, new ports and record increases in provisioned capacity all indicate revenue growth accelerating beyond FY2025 and profitably too. We have watched Megaport with interest for over six years and became shareholders for the first time in the December quarter 2024.

We will be opportunistic and if we see that that makes sense, we’ll do that. But we’re not necessarily counting that in. A very important thing for us while we continue to see the user base growing as quickly as it is is not to prematurely move into harvest mode. I am highly confident that we could double revenue extremely quickly, honestly within weeks or months if we got more aggressive.” Life360

Life360 exited FY24 strongly with Q4 seeing positive net income for the first time. Forward guidance is for this to continue and in line with consensus, even accounting for increased investment in new products. The share price fell slightly but it is still up 40% over the prior six months. They have room to grow into adjacent pet tracking and elder care, are more tightly integrating hardware (and giving it away to drive subscriptions). Add to that latent pricing power (management suggesting they could double revenue in a matter of weeks by pulling the price lever), it’s not surprising the stock holds up strongly against struggling peers.

The IRESS FY24 result was the first time the market got a relatively clean look at the continuing businesses since new management started in mid-2022. A lot needed to be done in all facets of the business, selling assets, paying down debt, re-engineering core products. Ultimately, what the market is left trying to price are high quality but relatively mature businesses which need meaningful re-investment to defend their current position and try and find new product growth. The P/E multiple has de-rated to reflect this reality, now at 22x vs the 25-30x over much of the last 2 years.

Nuix has similarities – a high quality but relatively mature business – but in contrast they have new products (NEO) which will expand margins on the existing customer base, and has a potentially very large addressable new market. Execution will require patience and hard work however, and with delays flagged at the result it sold off over 20%.

Materials

Steel and steel related stocks have not been having a good time for a couple of years now. Likely having something to do with the iron ore price falling from over US$220/tonne in 2021 to under US$100/tonne today. Iron ore producers (like Champion Iron and Deterra) and Coking Coal producers (like Coronado and Stanmore) are all suffering from steep earnings and share price declines – no different from those seen in Uranium stocks, but without the thematic excitement. We think share prices are below mid cycle fair value for these stocks, but they are not large positions in the portfolio (less than 3% in aggregate across iron ore and coking coal names).

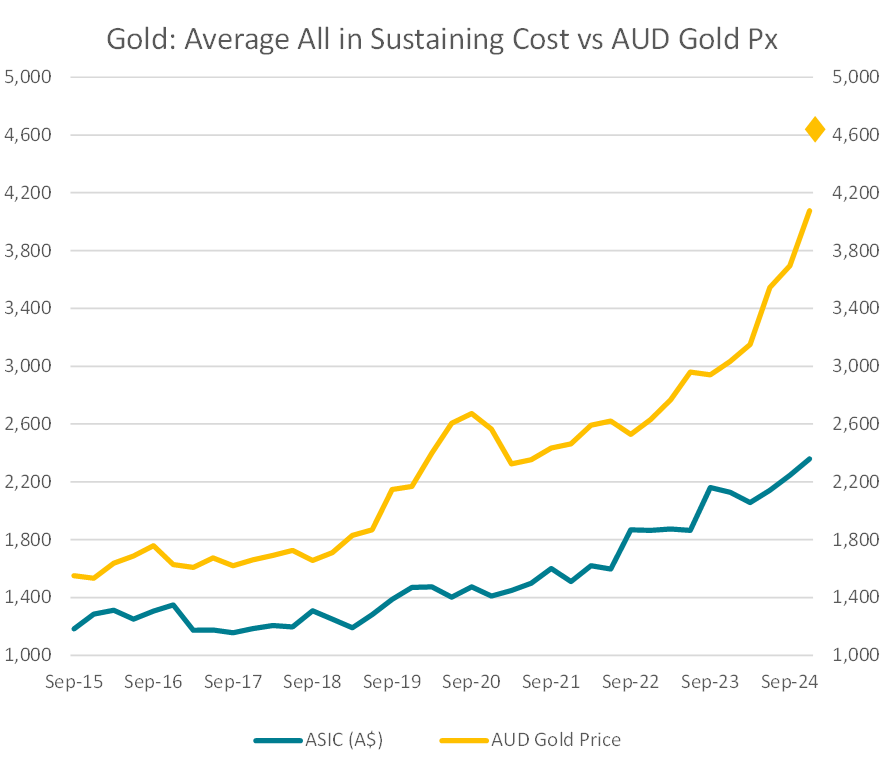

The gold sector saw small EPS downgrades (1%) despite record gold prices. Conditions in the gold sector at the top line are strong, but this also means there is upward pressure on All-In-Sustaining-Costs (AISC) across the gold mining space. Inflation in AISC during periods of strong commodity price growth is driven by a number of factors: mining lower grades, productivity decreases from mining more tonnes and general industry inflation. The sell-side tends to factor in price rises immediately and delays adjustment to cost bases. The sector overall is still making good margins with these record gold prices and given the uncertainty in the world at the moment, we see a strong argument for the gold price staying where it is and the better positioned gold stocks to continue to do well.

Real Estate

The REIT sector saw no movement in EPS revisions as the half year results largely confirmed benign but not exciting forward-looking conditions. Among the pure REITS we have in our portfolio (which are the less indebted ones), organic rent-growth was good, occupancy held up and property valuations appear to have bottomed (rent growth is now balancing out any further cap rate loosening). Interest rate headwinds have largely abated although REITS that have high levels of hedging are still seeing half on half increases in their cost of debt as hedges roll off and their group interest rates normalize to market. We continue to own positions in self-storage (National Storage and Abacus Storage King), childcare (Arena) and BWP Trust, which have relatively strong rent growth prospects into the medium term.

Pexa also sits within the real estate sector, but is more of a technology-driven exchange business exposed to residential property transaction volume. Pexa’s monopoly-like business in the Australian exchange posted stronger than expected transaction growth (+7%) and margin improvement during the half year. The two adjacent growth pillars (UK platform and Insights) improved their loss-making positions, which was positive particularly given the difficult conditions in the UK property market. However, the company gave more detail about the rollout progression for the UK exchange platform which indicates that the process of converting UK banks onto the platform is going slower and may be more difficult to execute than they expected. If property market conditions ease in Australia over the next 12 months, the Australian exchange business looks set up to deliver good earnings growth. This will be tempered through to mid-2026 by an IPART review on their pricing given the interoperability project to open the exchange up to competitors has been killed off by the regulator.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.