Active small cap investing – turning volatility into alpha

The hottest trend in markets right now is making volatility disappear by investing in private market assets. This is also known as volatility laundering – coined by Cliff Asness of AQR – to describe the practice of making investment risks appear lower than they are. “Appear” being the word doing the heavy lifting in that sentence.

As active small cap managers, we take a different approach. We embrace volatility and see it as an opportunity to convert volatility into alpha.

Compared to the indices (local or global) and the median active Australian large cap manager, the median active small cap manager has delivered significantly higher net returns over the long term. We have previously talked about the many structural reasons for ongoing active management outperformance in small caps, but today we will focus on one.

Volatility.

Large cap vs small cap volatility

If you listen to large cap managers, things are becoming increasingly volatile, with share price reactions during reporting season moving 5-10%. Blame for this unusual volatility is pinned on a moving target of irrational investors – it used to be High Frequency Traders, then it was Quants, then Passive, and now Pod Shops. As an active manager, unwarranted price moves disconnected from fundamentals are an opportunity to add value.

If we look at fundamental volatility – using earnings revisions as a proxy – we observe a very well researched and efficient ASX top 50 market. As such the range of expectations for large cap forward earnings is very narrow range when compared to less well covered small caps. True and significant surprises are relatively rare.

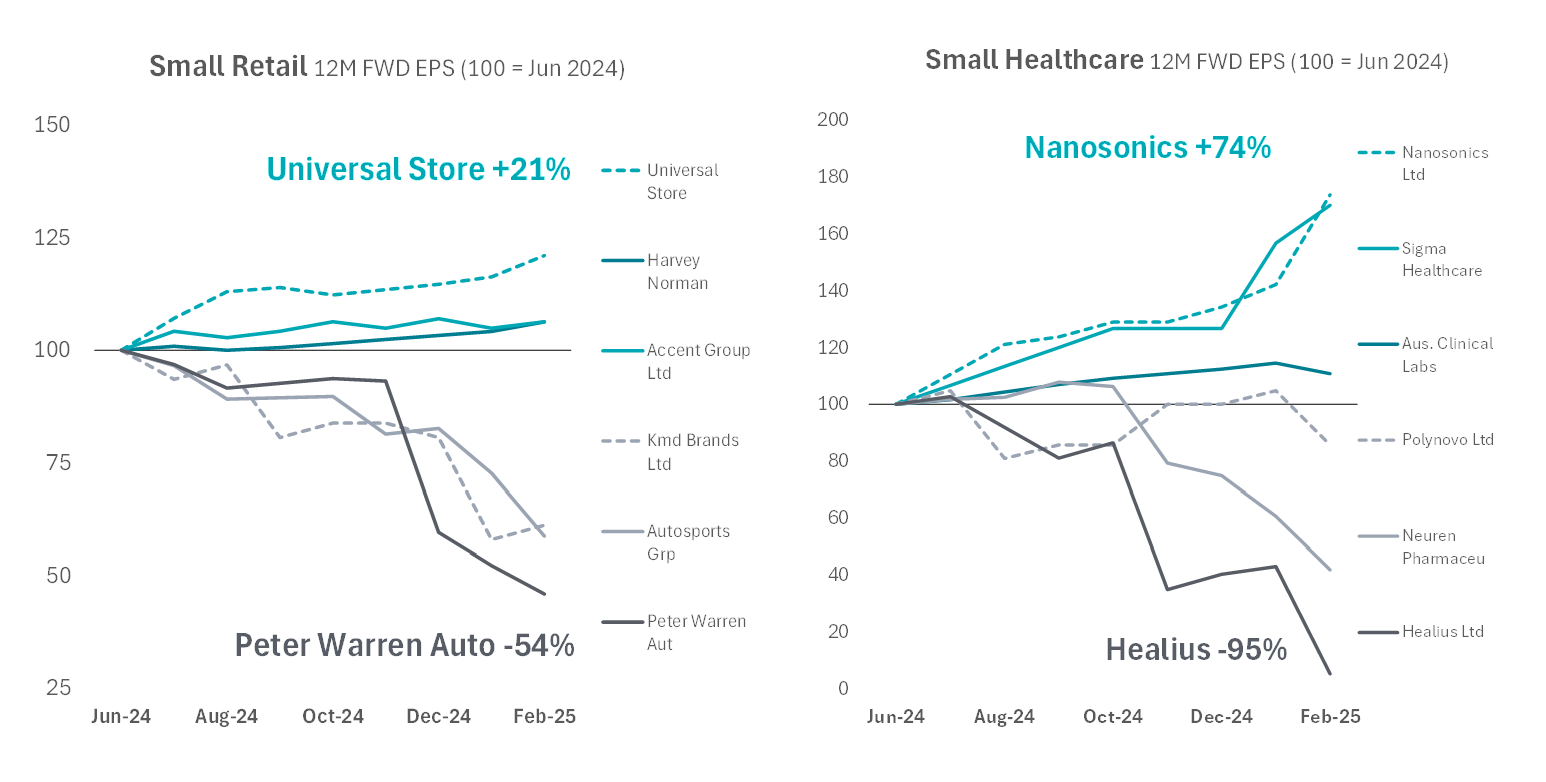

In small caps, the movements in earnings expectations are normally multiple times larger than seen in large caps, even within the same sector. Often the difference in execution by management can drive changes far larger than what is happening at the macro level.

In small caps, the movements in earnings expectations are normally multiple times larger than seen in large caps, even within the same sector. Often the difference in execution by management can drive changes far larger than what is happening at the macro level.

This is the volatility that active small cap investors convert into alpha. Trying to get more right than wrong, and over a long-term time horizon. Our view as active managers is we want volatility to take advantage of. Let it work for you rather than trying to hide from or launder it.

This is the volatility that active small cap investors convert into alpha. Trying to get more right than wrong, and over a long-term time horizon. Our view as active managers is we want volatility to take advantage of. Let it work for you rather than trying to hide from or launder it.

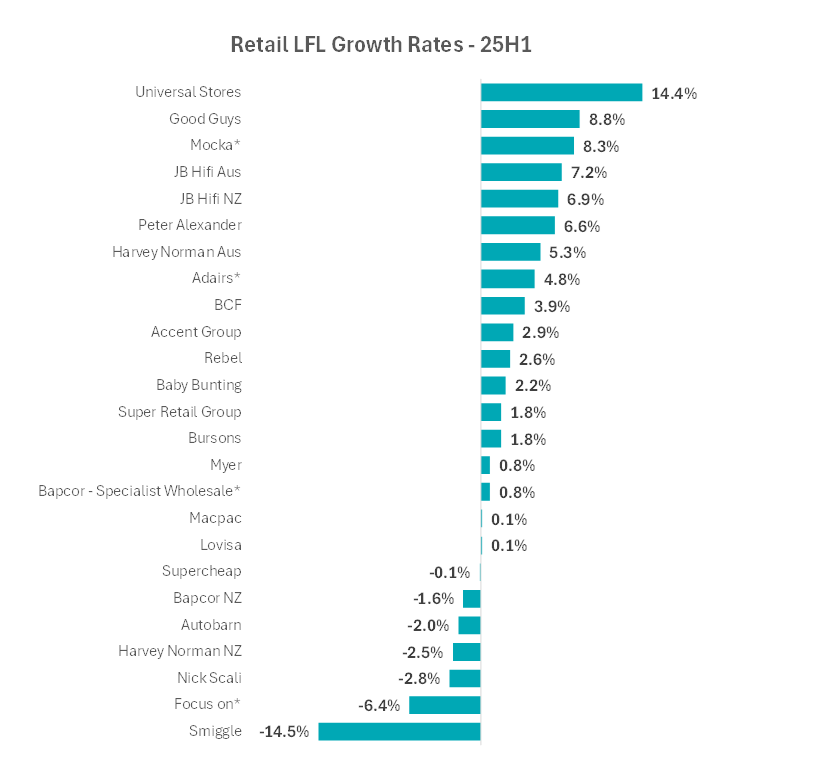

Volatility and the consumer

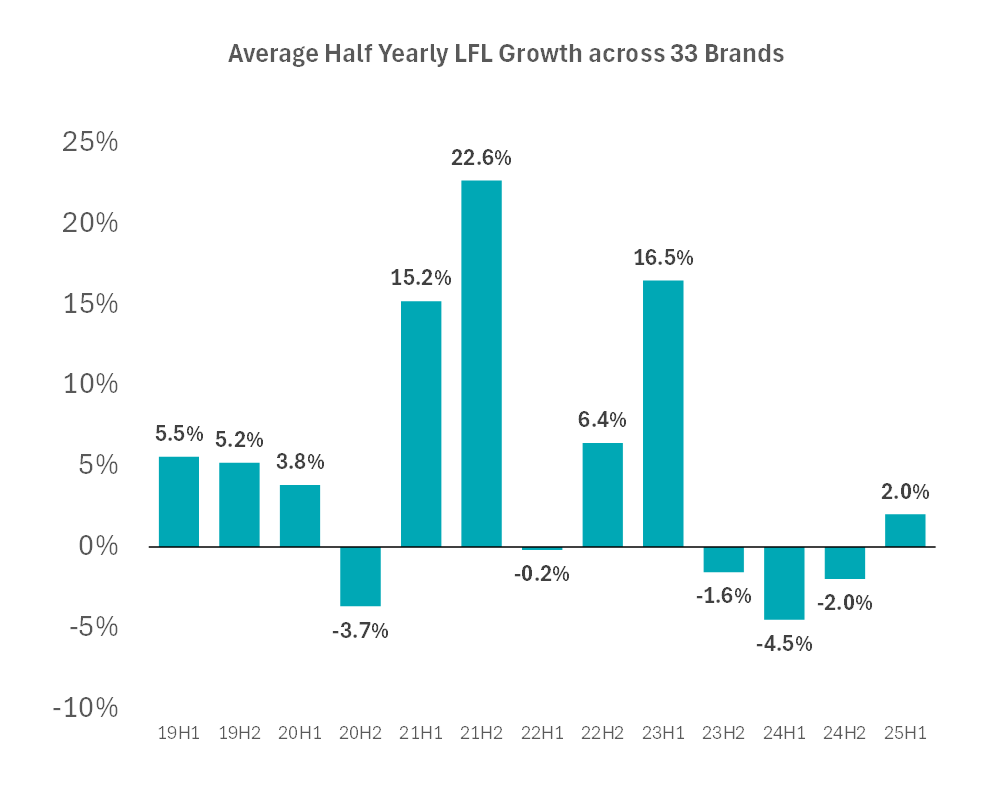

The Consumer Discretionary and Retail sector feels permanently volatile in two dimensions. The first is over periods of time. From year to year, the level of growth – most accurately captured by LFL sales growth – varies significantly. Having seen the depths of the cost-of-living crisis and impacts from inflation in 1HFY24, the sector overall has improved with a return to positive LFL growth in the reporting period just gone. The market will always obsess about where this number will go – will further interest rate cuts see an acceleration in spending? Will a recession finally appear? What will tariffs mean? We don’t know and in 25 years have never seen economist forecasts help us generate better returns in small cap retail stocks.

The second dimension of volatility is within the sector.

The second dimension of volatility is within the sector.

The range of outcomes between companies and brands – either because of category trends or more often due to management execution – which creates an even larger source of earnings dispersion within retail.

We have previously discussed retail names which we think are likely to be on the right side of this volatility, this time we will look at a retailer whose true value may be obscured behind the volatility.

We have previously discussed retail names which we think are likely to be on the right side of this volatility, this time we will look at a retailer whose true value may be obscured behind the volatility.

Harvey norman (HVN) – hiding in plain sight

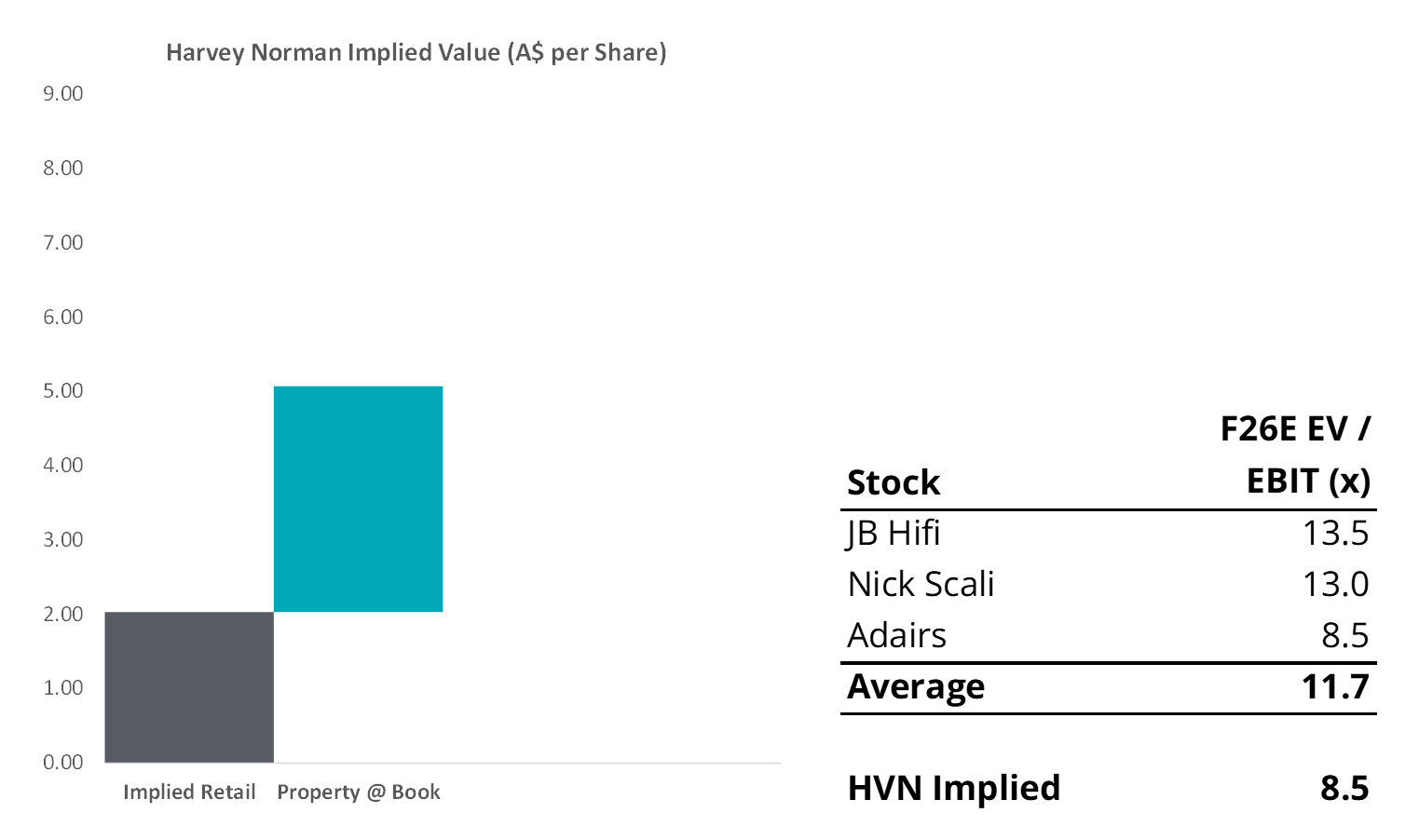

Harvey Norman is an unusual retail stock as they own their own property – in fact they own a portfolio of property even larger than just needed to house their own stores. To see how the market prices the HVN retail operations, we need to unbundle the property and retail businesses.

At ~A$5 share price, by subtracting the property at stated book value (around A$3 per share) we are left with a retail business at A$2 per share.

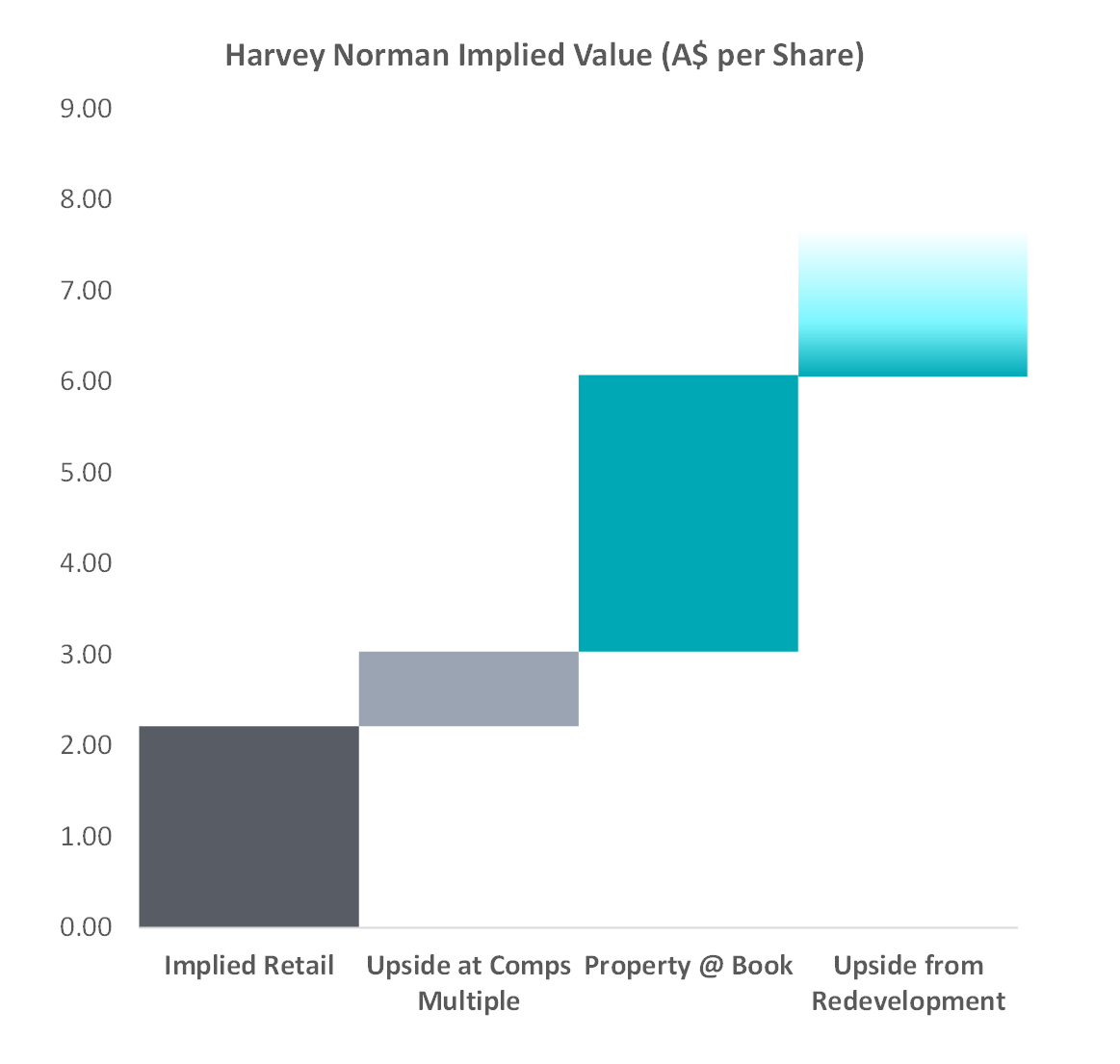

This implies an EV / EBIT multiple on HVN of 8.5x, well below similar, high-quality peers. But this is not the most interesting thing about HVN, and we are not the first to make this observation. We think the potential market value of the property portfolio is just as interesting.

How do we figure out what the true market value of the HVN property may be relative to the current in-use book value? Well, we can show one example of where this value uplift can come from using the Macquarie Park (Sydney) Harvey Norman site as an example.

How do we figure out what the true market value of the HVN property may be relative to the current in-use book value? Well, we can show one example of where this value uplift can come from using the Macquarie Park (Sydney) Harvey Norman site as an example.

Harvey Norman applied to Ryde council in 2013 for a mixed use (which means a combination of commercial and residential) redevelopment and was knocked back. Six years later in 2019, the Lachlans Village mixed use development completed – literally right next door, with the Ryde Metro station 600m away opening the same year.

It is slowly dawning on people, that if you want to solve the housing crisis, you need to build more homes. To build more homes where there is existing infrastructure, you need to change zoning laws. And so, the NSW state government, under the Transport Oriented Development Program (TOD), has now rezoned this area including the HVN site coming into effect on 27 November 2024. This rezoning and the potential for re-development changes the value of this site.

This is only one site in the HVN portfolio, and it is not even in the top 20 disclosed in their annual report valuations. We estimate it is carried on the books at around A$40m.

We conservatively estimate the site could be redeveloped into mixed use with the HVN brands underneath and around 750 apartments on top. This is using a FSR of 2.5:1 and six stories height limit. If this site was sold to a developer today, we estimate it would likely fetch closer to A$200m than the A$40m carrying value. This site was re-zoned with a FSR of 5:1 and a height of building limit of 190m (implying a higher valuation than we calculated). If HVN developed the site themselves, the value accretion would be much higher (as would be the risks). These are very approximate numbers for the purpose of illustration – but re-zoning based value uplift is very real.

This property represents around 1% of the carrying value of their total property portfolio. Not every property will have the same alternate use valuation uplift as Macquarie Park – but we think some of them will as they share the same characteristics – where a re-zoning to mixed use helps solve the housing shortage and unlocks value in the HVN land bank. HVN is not an instant gratification investment – the value unlock here could take many years to unfold and investors to understand.

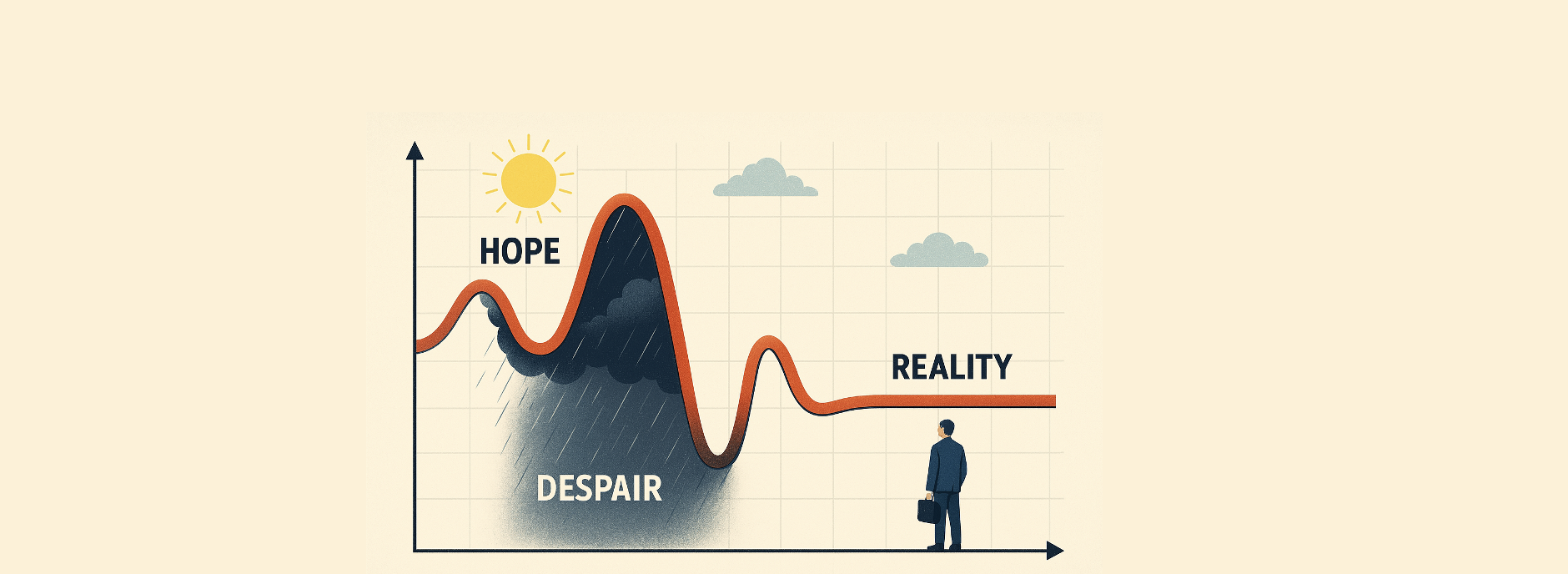

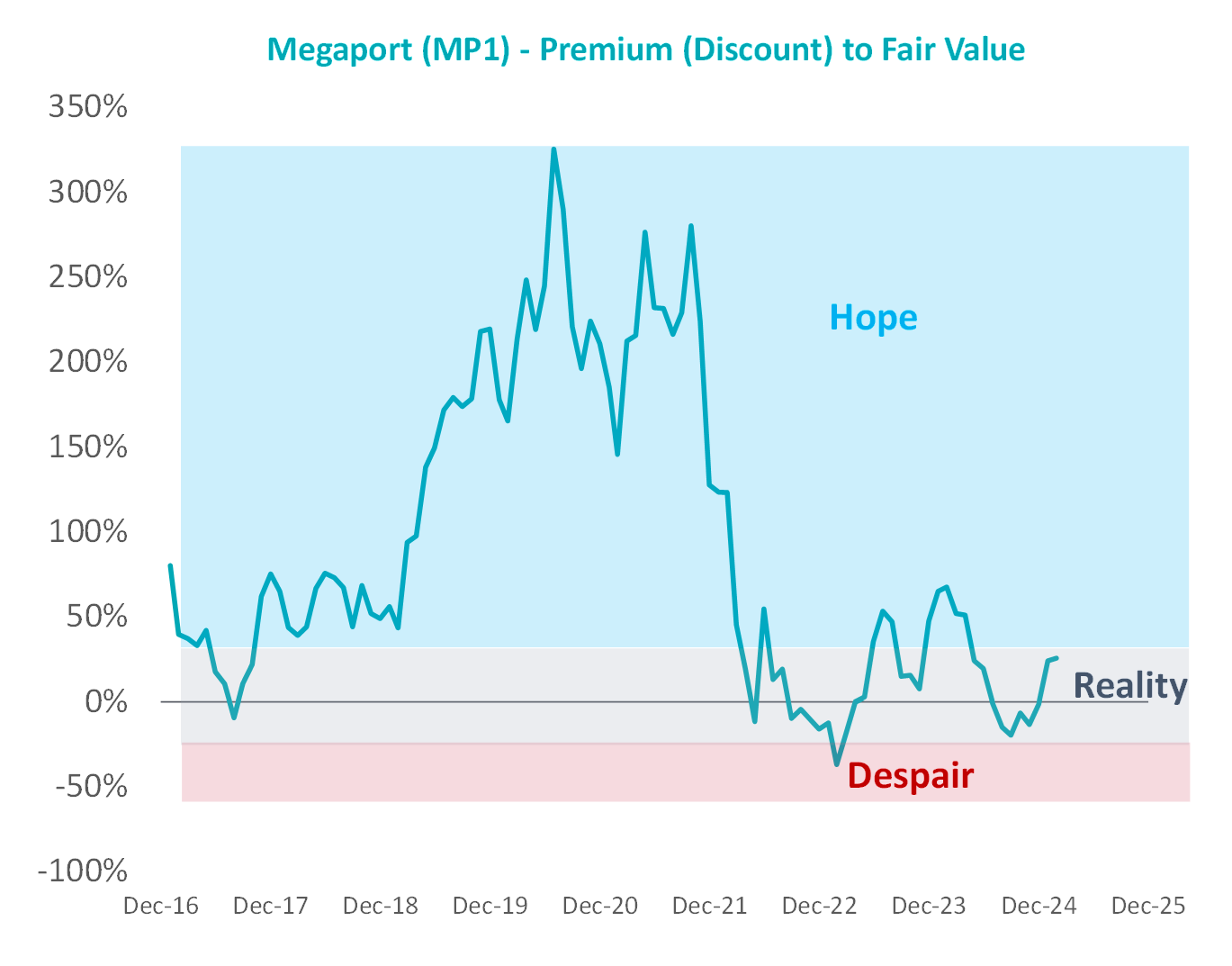

Megaport (MP1) – being patient rather than hopeful

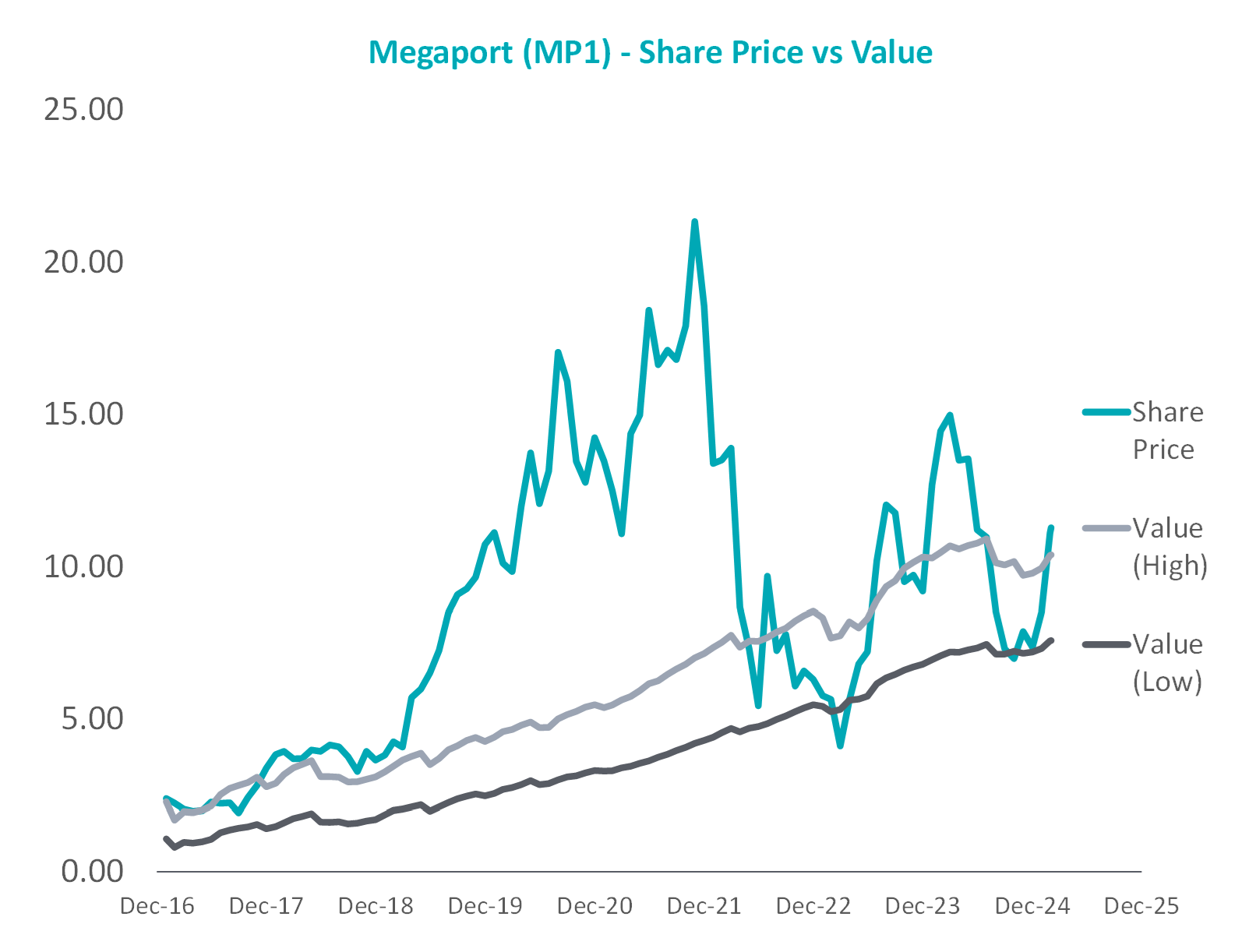

Another form of volatility is the way share prices move relative to value over time, and how being patient can allow volatility to work in an investors’ favour. The long-term volatility of the Megaport share price over the past decade has been wild.

If we look at the stock premium or discount to an estimate of fair value over time, we observe the stock has traded at huge premiums (Hope), large discounts (Despair) and closer to fair value (Reality). We are not hope based investors – but this doesn’t mean we don’t keep track of these types of companies for an opportunity when things change. Eventually hopeful investors gave up on Megaport and it fell into a more realistic zone of pricing vs fair value. We became shareholders in Megaport for the first time in late 2024, which begs the question, why didn’t we act sooner? Why didn’t we buy in late 2022 when prices and discounts to fair value were lower?

In late 2022, the business was still loss making, and we had concerns over management and governance. The Go To Market (GTM) strategy in the US was flawed and the product range was narrow. By late 2024, although the share price was higher and the valuation was not quite as cheap, the business was significantly de-risked. The business was now profitable. New management and new directors were in place. Reinvestment in US GTM was working and the product range was expanding.

In late 2022, the business was still loss making, and we had concerns over management and governance. The Go To Market (GTM) strategy in the US was flawed and the product range was narrow. By late 2024, although the share price was higher and the valuation was not quite as cheap, the business was significantly de-risked. The business was now profitable. New management and new directors were in place. Reinvestment in US GTM was working and the product range was expanding.

Long term volatility and patience give us the opportunity to invest when companies and stocks align with our view of appropriate risk and return.

Long term volatility and patience give us the opportunity to invest when companies and stocks align with our view of appropriate risk and return.

Disclaimer

This communication is prepared by Longwave Capital Partners (‘Longwave’) (ABN 17 629 034 902), a corporate authorised representative (No. 1269404) of Pinnacle Investment Management Limited (‘Pinnacle’) (ABN 66 109 659 109, AFSL 322140) as the investment manager of Longwave Australian Small Companies Fund (ARSN 630 979 449) (‘the Fund’). Pinnacle Fund Services Limited (‘PFSL’) (ABN 29 082 494 362, AFSL 238371) is the product issuer of the Fund. PFSL is not licensed to provide financial product advice. PFSL is a wholly-owned subsidiary of the Pinnacle Investment Management Group Limited (‘Pinnacle’) (ABN 22 100 325 184). The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: WHT9368AU

Link to the Target Market Determination: WHT9368AU

For historic TMD’s please contact Pinnacle client service Phone 1300 010 311 or Email service@pinnacleinvestment.com

This communication is for general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is for illustrative purposes only and is not indicative of future performance.

Whilst Longwave, PFSL and Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Longwave, PFSL and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

Any opinions and forecasts reflect the judgment and assumptions of Longwave and its representatives on the basis of information available as at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Longwave. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

This may contain the trade names or trademarks of various third parties, and if so, any such use is solely for illustrative purposes only. All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with, endorsement by, or association of any kind between them and Longwave.